Global catastrophes blamed for high first-half combined operating ratios

Beazley’s first-half results are a good indication of what to expect from other Lloyd’s insurers this reporting cycle, both in terms of profitability and preparation for a potential hard market.

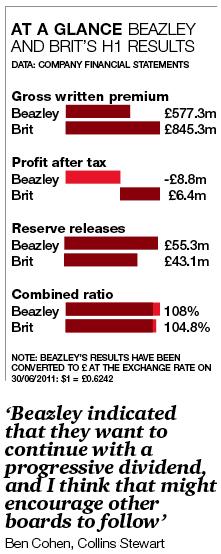

Beazley was the first listed Lloyd’s player to report. It made a loss after tax of $14.1m (£8.8m) in the first half this year, compared with a profit of $97.9m in the same period last year. Lower revenues, higher claims and higher operating expenses all conspired to push the company into a loss.

Of particular significance for the result was $154m of losses emanating from catastrophes in Australia, New Zealand and Japan, with the US tornadoes adding an estimated $29m. Beazley’s combined ratio came in at a loss-making 108% in the first half of 2011, compared with a profitable 90% in the same period of 2010.

Fellow Lloyd’s insurer Brit, which was made private in April this year following its acquisition by private equity consortium Achilles, made a profit of £6.4m. However, this was 90.5% down on the £67.4m it made in the same period of 2010, and the company made an underwriting loss for the first half, posting a combined ratio of 104.8%, compared with 96.5% in the first half of 2010.

In addition, Brit’s small profit position is expected to be the exception rather than the rule.

“I would be surprised if any of the quoted companies I follow, apart from Lancashire, would report a profit in the first half, just because of the catastrophes,” Collins Stewart analyst Ben Cohen said, before adding that he was surprised that Beazley’s loss was as small as it was.

Another revealing aspect of Beazley’s first-half results was its decision to boost its dividend payment despite the losses. Beazley paid out an interim dividend of 2.5p a share in the first half, up 4.2% on the 2.4p it paid for the same period last year.

Cohen believes that others could follow suit. “I had expected after Japan that all the dividends would be held flat as a cautionary measure, but Beazley were indicating that they want to continue with a progressive dividend and I think that might encourage other boards to follow them,” he said.

“One of the key reasons investors hold these stocks is for the dividend, so that could be taken well.”

While Beazley’s outlook on the pricing environment is generally downbeat – it expects rises in catastrophe-hit areas, but is planning for flat rates overall – it is nonetheless also preparing for a hardening in rates if more catastrophes hit. The company boosted its as-yet unused bank letter of credit facility to $225m from $150m on 21 July.

Beazley chief financial officer Martin Bride explained that this was to ensure the company would quickly be able to access funds if the right opportunities to expand presented themselves.

Other companies in Beazley’s peer group have announced contingent funding to write more business. For example, Lancashire Holdings launched a $250m special-purpose reinsurance vehicle, known as a sidecar, in May. This will effectively allow the company to access capital to write more business where opportunities arise.

Similar preparatory announcements could be made in second-quarter results. “Companies want to give the market the confidence that they are ready, so that even if there is a big loss, rather than just selling the shares investors will think: ‘These companies will be able to take advantage without raising new equity’,” Cohen said. “I think they will use the H1 results for that positioning.”

Beazley announced with its first -half results that if there are no further catastrophes in the remainder of 2011, it will post a full-year combined ratio in the mid-90s. While further large losses would prevent this, the company said they would also push up rates across the industry.

No comments yet