Upward trend in deals under £40m continues with fourth consecutive rise in volumes and values

At the end of the first quarter this year, we concluded that insurance sector mergers and acquisitions appeared to be recovering: 2009 had been the worst year for insurance M&A in a decade but, by all measures, the first quarter 2010 was at least 25% more active than the fourth quarter of 2009.

At the same time, however, deal activity had not reached anything like the dizzy heights of some recent years. So it was with a reserved sense of optimism that we awaited the second quarter to see if, indeed, the upward trend in activity would continue. Or would new factors, for example uncertainty caused by the general election, nip the M&A recovery in the bud?

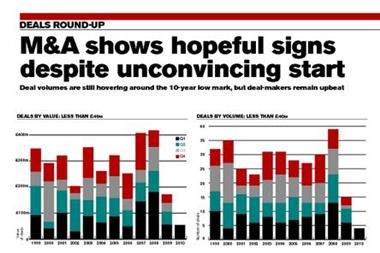

As usual, we answer this question by looking at the hard facts for deals. These are recorded in the charts here, using data compiled by Experian Corpfin, and divided into transactions with values above and below £40m. In each case, they only include deals completed in the period where the amount paid has been publicly disclosed and the buyer or seller operates in the UK insurance market.

Smaller transactions (under £40m) witnessed the fourth consecutive rise in both deal volumes and values: during the second quarter of 2010, there were six deals – a 50% increase on the first quarter. While this is only about half the number of deals per quarter seen in the heady days of 2008, it is a far cry from, for example, the solitary deal (disclosed as worth less than £40m) in Q3 2009. It is therefore perhaps cause for some optimism.

Aggregate deal values painted a similar picture – at £83m, Q2 2010 was 30% up on the first quarter and had the highest aggregate value since the collapse of Lehman Brothers.

The picture for larger deals (over £40m) in any quarter is always rather more ‘binary’ – a few big transactions either happen or they don’t – and this quarter was no exception. Rather than witnessing continuing growth, deal volume was down in Q2 2010 at just one deal compared to two in the preceding quarter, and the aggregate value reduced commensurately.

But the deal-making picture for a slightly longer period – looking at the first six months of 2010 and as measured across all deals – is rather more encouraging with values already ahead of the total for the whole of 2009.

Taking a wider view, statistics produced by private equity journal Unquote on investment in UK management buy-outs across all sectors in the second quarter of 2010 show that activity is holding up. As would be expected, deal-making has not returned to peaks seen in recent years – for buy-outs this was 2006-08 – but there has been enough activity to fuel optimism around the market.

As for insurance M&A, the wider UK buy-out market has seen almost the same aggregate value of deals in just two quarters of 2010 as in the whole of 2009. At the same time, banks are returning to the fray and funding deals again.

This appears, understandably, to be fuelling optimism, as demonstrated by Unquote’s recent survey of market sentiment. More than 80% of survey respondents felt that buy-out activity in smaller deals, defined in this case as below €150m (£124.5m), will increase; and a large majority that predicted activity in larger deals would either increase from what is already a reasonable level or stay the same.

In the insurance sector, this buoyancy is supported by Moody’s. As recently reported by Insurance Times, the rating agency expects a material upturn in insurance M&A during the remainder of 2010, driven by the twin factors of companies seeking growth in sluggish markets while trying to comply, through consolidation, with the new burdensome capital requirements of Solvency II.

Further activity should be created by the sale of the insurance arms of RBS and ING in order to adhere to EU competition regulations.

So, increasing M&A activity in insurance appears to be supported by activity across the board in the UK. This fuels optimism and is supported by a regulatory impetus. A virtuous circle? The coming quarters’ results will tell.

No comments yet