The number of M&A deals may be set to decrease, but insurers and investors will increasingly be looking to snap up higher-value insurance acquisitions

Insurers and investors have regained an appetitive for higher-value insurance mergers and acquisitions (M&A).

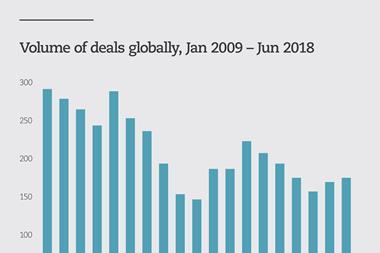

The value of deals increased while the number of deals fell, which Willis Towers Watson (WTW) suggests in its M&A Trends overview means that purchaser priorities are shifting.

Completed deal values were up 170% in H1 of 2017, compared to the same period in 2016. Meanwhile, deal volume fell by 17.7%.

Companies shirking capital intensive products

WTW’s report highlights that regulatory requirements, tepid premium growth and low-interest rates have forged a difficult environment to get reasonable returns. This is particularly the case in developed markets.

Over half of respondents had reduced exposure to capital-intensive products or increased exposure to less capital intensive products, with 65% intending to over the next three years.

Activity has been most pronounced in the annuities segment of the market. Large closed books are increasingly up for sale in the annuities market.

Solvency II has led regulators across Europe to force insurers to strengthen balance sheets, while “lower for longer” interest rates. The two factors have damaged the dividend potential of many companies and consequently, WTW suggests this will lead to more closed book deals mirroring the in the UK across Europe.

Low margin, high interest

Many companies will be actively seeking growth – including through M&A – over the next three years, according to the report. They are likely to scale back share buybacks and dividend support to invest in it.

Insurers and investors will look to buy into “quality over quantity”, with companies expected to complete fewer deals in the next three years than over the preceding period.

90% of respondents have made one or two acquisitions in the past three years, but just over three quarters (78%) of those surveyed intended to undertake one to two acquisitions over the next three years.

Respondents were expecting to spend more on a single acquisition than in previous years. Over the last three years, 8% had done a major deal (greater than $500m), while 17% were expecting to do a deal of this magnitude over the next three years.

Brand is the biggest concern

Insurers and investors were most motivated by building brand strength, which the report says is due to digitalisation and technology-based distribution and partly due to a perceived need to target “millennials”.

65% of respondents also saw revenue, cost and financial synergies as a “major driver”, which WTW suggests is due to regulatory burden and soft market pressures.

The third highest motivation for deals was innovation and technology.

No comments yet