The very rich expect a silver service from their insurance cover and will pay for the privilege. What's key is to recognise the importance of being tactful and discreet, knowing a van Eyck from a van Dyck, and being ready for that vital call, just in case one’s donkey has slipped into the pool again

Unobtrusive yet always on hand, tirelessly fulfilling every whim with scrupulous discretion: the perfect broker or insurer for the very rich sounds rather like the perfect butler. If you think you’ve got what it takes, the high net worth market is not a bad place to be. Sums insured are high and clients are prepared to pay an extra premium for the right level of service. They are also loyal – renewal rates above 90% are not uncommon.

While on paper their assets may have shrunk in the downturn, their houses, cars and million-pound collections of fine art or jewellery are still there and as vulnerable as ever, making it a relatively stable market too.

“High net worth clients can be very demanding,” says Paul Macbeth, managing director of broker Macbeth, which specialises in insurance for wealthy individuals. “They want everything done yesterday, but that comes with the territory. If you don’t want to react quickly or you can’t provide that service, you’re in the wrong area.”

It is rewarding too though, he says. “It’s interesting to learn about these people and how they became successful. The loyalty is incredible – very rarely do we lose someone.”

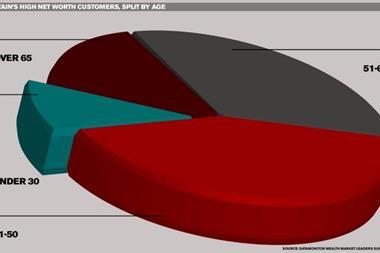

The phrase on the lips of every high net worth specialist is “cash-rich, time-poor”, and policies will offer wider cover, higher limits and a better service to accommodate that lifestyle. But offering the perfect high-net-worth insurance service involves much, much more ...

1. The best protection money can buy

“These clients have far more complex asset requirements than Joe Public and they want the peace of mind that they’ve got the best protection,” Chubb’s European personal lines manager Simon Mobey says. “They may have collections of fine art, jewellery, multiple homes and domestic staff, and they’re not just looking for the cheapest cover, they’re keen that policies have the best cover.” At specialist insurer Chubb, annual premiums for high net worth policies are between £2,500 and £10,000, but some of its richest clients in the ultra high net worth category pay as much as £300,000 a year. High net worth clients almost always go through brokers, and they appreciate the advice and the assistance that intermediaries provide.

2. An appreciation of the finer things in life

High net worth clients by definition have more expensive and exotic possessions than the average household, so you need to know what you’re looking at and how to repair or replace rare items if the worst should happen. Firms in this market employ teams of specialists who can visit clients at home to gauge the value of their collections and offer advice on protecting them.

“Clients are looking for an understanding of their lifestyle and they want experts in the field,” Hiscox head of art and private client business Austyn Tusler says. “They might have art or antiques, classic cars or a Grade I-listed building. We need to know about restoring fine art or how restoration could depreciate it. If someone isn’t qualified to restore a painting, they could cause further damage.”

The true value of a home or its contents might not be immediately apparent. “High net worth clients often have very expensive fixtures and fittings, such as marble floors; we see fitted kitchens worth £100,000 or £150,000,” Mobey says. “It doesn’t take long for that to mount up.” Chubb offers a complimentary appraisal service, which Mobey says pays for itself. “Eight out of 10 properties we see are undervalued.”

3. Discretion

Data security is of paramount importance. “As you’d expect, some clients are reluctant to release an inventory of their jewellery or fine art,” Chubb’s Mobey says.

“Some are happy to have it in a secure environment in our office, but others prefer to let us have a look but won’t allow it to leave their possession. We would go through that inventory, ensure it was from a reputable firm and then note in the file that details are on record with the client.”

4. Importance of tact

It helps if you can keep a straight face when confronted with outrageous sums or less conventional collections. At Allianz-owned broker Home & Legacy, underwriting and product manager Adrian Ewington says more mature and experienced staff tend to be employed. “We need people who can engage with these clients, who have a well-rounded knowledge and who won’t be overawed when they’re dealing with someone who has a £50,000 ring or a £100,000 painting. It's important to build a relationship, so you need to be able to engage a customer in conversation about these items and make them feel comfortable.”

Clients may collect anything from old banknotes to comic books. “A rare first edition of a Superman or Batman comic can sell for hundreds of thousands of dollars.” Hiscox’s Tusler, too, has expressed enthusiasm for some unusual collections: “People who have wealth are passionate about what they collect. We do all sorts, from porcelain, art and jewellery to toys or teddy bears or Barbie dolls.”

The extremely wealthy may also lead extreme lifestyles that can lead to some jawdropping claims. Ewington recalls the story of a donkey falling into a swimming pool: “It caused considerable damage to the pool, and distress to the donkey.”

5. Bespoke policies

High net worth clients may have complex needs but they don’t want a complex set of insurance policies. That’s why insurers must be able to offer a portfolio of cover. Zurich Private Clients head Matt Schofield says that it can offer different wordings for homes in the UK and abroad and their contents, as well as fleets of cars, yachts and international travel, but with a single renewal date. “Having it in one place makes it a lot easier for them. Insurers need the ability to understand different elements and put them together. All our underwriters are multiskilled so there’s one point of call and clients aren’t bouncing around different departments.” Insurers also need to be comfortable with much larger single items than you would find on a standard policy, such as pieces of jewellery, he adds.

6. Lifestyle cover

As well as a complimentary valuation service, high net worth policies may include other services to make clients’ lives easier. Hiscox, for example, offers legal expenses cover and helplines for legal and domestic issues, which might include boundary disputes or finding an emergency plumber.

Clients can also access a website with travel advice supplied by specialist risk consultancy Control Risks Group, and its 606 policy includes basic kidnap and ransom cover for clients travelling abroad. The world is a more perilous place for a high net worth client. The policy’s family protection section also covers stalking threats and road rage attacks against “you or your chauffeur”.

Rich clients lead international lifestyles and their insurer or broker must be able to accompany them, albeit virtually. “Wherever they are in the world, they should be able to access their insurer,” Hiscox’s Tusler says. Hiscox provides a 24-hour medical helpline and employs staff who can speak many languages to assist with claims where necessary.

7. Always on call

When high net worth clients pick up the phone, they should always be within a couple of rings of somebody who knows them and can immediately respond. Even at the weekend. “Our clients want somebody who reacts when asked to do something,” Macbeth says. “When they want to talk to you, they want to talk to you. All of our clients have our mobile numbers and everyone has an iPhone so that emails are monitored and dealt with outside of office hours.”

At no time is this more important than when there is a claim. For straightforward claims, insurers will post a cheque or make a BACS transfer within hours. For more complex cases of fire or water damage, they may send a loss adjuster the same day.

“We have a network of loss adjusters around the country, and the client will have the mobile number of the managing director of the local firm,” Oak Underwriting managing director Bob Trott says.

8. A very personal service

Wealthy clients may prefer a replacement item to cash, but they still get to choose exactly where it comes from. “What a high net worth insurer should never do is force the customer down the mass-market supply route,” Home & Legacy’s Ewington says. “Say you have a certain computer from a particular company. What we wouldn’t do is say we’re going to give you an equivalent model, and send you to collect it from the local Argos.”

Insurers must also be prepared to work with a client’s chosen firm: when the donkey fell into the swimming pool, Home & Legacy directly engaged the original pool contractor to carry out the repairs.

Oak, too, will work with whichever firm a client specifies. “We had a claim for a kitchen that had been installed seven or eight years ago by a well-known installer,” remembers Trott. “Rather than just delivering a new kitchen, we made sure we got that installer to replace it.”

Chubb’s Mobey has an anecdote that neatly sums up the difference between a standard policy and the Rolls-Royce treatment that high net worth customers receive.

Two business partners were involved in separate car crashes. The one insured with Chubb was provided with a replacement Bentley the same day, and received £120,000 within two weeks, along with an offer of help to source a replacement vehicle. The other guy had a standard policy. The insurer insisted he send his Aston Martin to a mechanic on its approved repairer network, who failed on four occasions to complete the job to the client’s satisfaction.

“First there was something wrong with the respraying, and then the door. He ended up driving to client meetings in a Nissan Micra for months. Our clients get to choose where they take their vehicles. The guy said: ‘I don’t care what it costs, get me that insurance’. ”

And that’s certainly not something you hear customers say every day. IT

No comments yet