As business exposures increase, what is the outlook for corporate risks?

The business environment is becoming ever more complex and with that, demands for cover change.

Last year at Airmic cyber risk was being talked up as a specialist line but commentators now say it’s shaping up as another form of liability, a business-as-usual type risk.

New risks are in many cases driven by the huge swathe of business regulation being enacted, of which at least half is reported to be handed down from Brussels.

Zurich European middle market network leader Steve Green says: “It’s a fundamentally legal environment, driven by legislation and regulation, corporate governance, contract law and supply chain issues. The whole world is getting more sophisticated and people are getting more litigious. Employers’ liability and professional liability dominates.”

An example is a supplier no longer being able to trade with a major retailer like Marks & Spencer if they don’t meet certain criteria, such as having an energy performance certificate. Regulation like the Health and Safety Act also puts pressure on companies to get cover for offences like corporate manslaughter, which can carry a jail sentence. D&O cover is similarly being seen as more vital.

Zurich’s response to the new business environment is to team up with advisory partners like lawyers, and energy and health and safety specialists to work with brokers in evaluating clients’ risk.

Zurich head of corporate David Carey says: “We will provide an insurance product, but also support with value-added providers, and advice on how to avoid these situations in the first place. Also, we want to be sustainable rather than coming in and out of the market.”

What’s influencing the markets

Going up

Business interruption add-ons: The often unpredictable effects of extraordinary weather events, political unrest and economic upheaval mean that demand for business interruption add-ons is rising.

Enterprise risk management: More risk management roles are being created as larger companies look to understand what risks may be embedded within their business processes.

Supply chain advice: Activity is expected around evaluating risks specifically within increasingly complex supply chains, including anticipating the potential downsides of just-in-time manufacturing techniques.

Going down

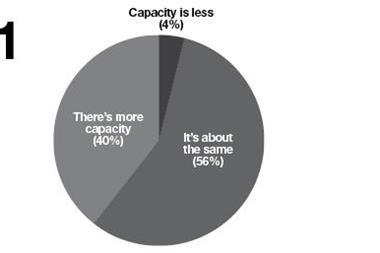

Rates: No sign of markets hardening across the board, although some pockets where claims have risen might come back, and certain insurers are pulling back.

Corporate activity: The Bank of England’s monetary policy committee has downgraded its growth forecast to 1.4% – a fall from 1.8% three months ago – warning that the UK isn’t immune from turmoil in world economic markets.

Retail: More retailers could exit altogether if consumer spending remains weak.

What insurance buyers think

There is a growing perception among companies with more unusual risk challenges that, following a year of high payouts, insurers are less willing to accommodate non-standard policies. This could be an opportunity for new business teams at intermediaries offering access to markets and advice on policies. The leading sectors with specialist policy requirements are professional/ business services, retail, and utilities.

No comments yet