Market’s combined operating ratio in 2018 hits a high point

The UK motor insurance market has reported its best underwriting performance for more than 30 years.

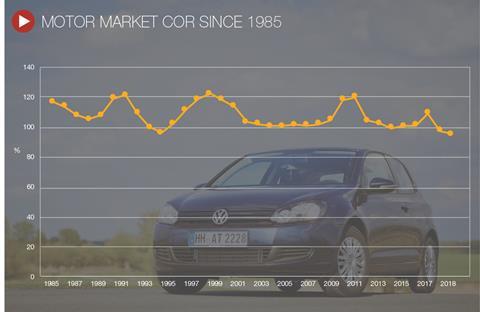

Research from EY, which studied insurers’ Solvency and Financial Condition Reports for 2018, calculated a reported market combined operating ratio (COR) of 94.8% for 2018, the best result for 33 years and a two percentage point improvement on the previous 12 months.

In fact, 2018 is only the fifth year since EY records began in 1985 that the UK motor market has reported an underwriting profit, and only the third time the industry has had a COR below 100% for two years running.

EY said the strong result reflects the benefits from premium strengthening in 2017, as well as pre-emptive reserve releases ahead of the change to the Ogden discount rate in 2019.

Excluding the benefit of these reserve releases, EY estimated the COR for the year would have been 98%, slightly worse than the 97% reported for 2017.

Hindsight, however, is always 20:20 and many insurers have since been forced to strengthen reserves following the Ogden rate being raised to just -0.25% instead of the anticipated 0% to 0.25% rate that many insurers were preparing for.

The consensus at the time of the announcement was that the rate change did not go far enough, with AXA’s David Williams saying that a negative rate “simply does not reflect the economic reality of the investment opportunities for those receiving lump sum payments”.

Meanwhile, LV= claims director Martin Milliner said the change would only lead to further uncertainty, and Zurich’s David Nichols predicted there would be increased costs as a result.

The ABI reacted the most strongly, with director general Huw Evans writing a scathing letter to the justice minister David Gauke, in which he accused the Ministry of Justice of being “misleading and wholly disingenuous”.

Revised financial statements

And with the new rate being announced in July, just weeks before insurers were due to publish their half year results, many had to revise their financial statements and make sizeable adjustments to reserves.

Admiral posted a huge blow from Ogden to the tune of £33.3m, more than the insurer had predicted (£22m).

Worst hit was QBE, which predicted the rate would be set at 0.25%, and had been working on this assumption since February 2018. This prompted warnings from financial analysts Berenberg Bank suggesting the insurer could face “significant risks” if it stuck with its strategy.

QBE did not listen, and as a result, suffered a huge £51m blow from the rate change. This led to the group reporting an overall underwriting loss of £13.2m.

LV= was hit with reserve strengthening of £13m, which took underwriting profit lower in H1 2019 (£19m) than it was in H1 2018 (£26m). The company had expected to report a profit of £32m before the lower than anticipated rate change.

Elsewhere, Direct Line took a £15.9m hit, while Hastings took a £9m body-blow, leading to an immediate 8% tumble in its share price.

While it did not issue a monetary figure on the hit, specialist motor insurer ERS said Ogden was to blame for its unprofitable COR for H1 2019, which worsened to 102.8% from 96.6% a year earlier.

This repositioning by insurers, combined with continuing high claims inflation, means that EY is predicting a tough couple of years ahead for motor insurers – the consultancy firm forecasts a market COR of 104.7% for 2019 and 107.6% in 2020.

Difficult market ahead

Tony Sault, UK general insurance market lead at EY, said motor insurers should prepare for difficult market conditions as they enter the next decade.

“The outlook looks altogether gloomier over the next couple of years, with results expected to slip firmly into the red,” he said. “The market is softening rapidly as it prices in the impact of whiplash reforms, at the same time as contending with continued high inflation on damage claims.

“The FCA market study will be another key focus for the industry, potentially resulting in fundamental changes as insurers seek to demonstrate fairness and transparency in their pricing models.”

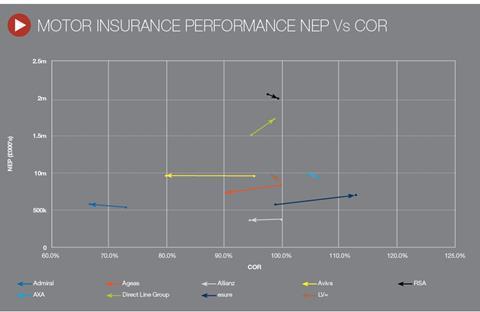

Insurance Times’s analysis of the latest set of Solvency and Financial Condition Reports from nine of the leading motor insurers in the UK has revealed that Admiral is top of the pack when it comes to motor underwriting, reporting a market-leading COR of 67.3% for 2018.

Of the nine insurers analysed, Admiral was one of seven to report an improved COR compared with 2017, knocking off 5.8 percentage points.

It was also one of just three insurers to report profitable growth during 2018 after also growing its motor net earned premium (NEP) by 6.8% to £594.3m.

Admiral’s improved underwriting performance was driven by a 6.1 percentage point improvement in its group motor loss ratio, buoyed by the pre-emptive reserve releases ahead of the Ogden discount rate change, which more than offset a 0.3 percentage point increase in its expense ratio.

Despite this improved performance, the insurer was forced to raise motor premiums in the second half of the year in the face of rising claims inflation. UK insurance chief executive Cristina Nestares said in the company’s annual report that the insurer maintained a “disciplined approach to underwriting” but that rate increases “meant that our growth rate slowed as the year progressed”.

The most improved underwriter, however, was Aviva, knocking 15.3 percentage points off its motor COR for a 2018 ratio of 79.9% (2017: 95.2%) and growing its motor book by 17.4% to report a NEP of £955.6m.

The insurer’s pre-emptive action in anticipation of the increase to the Ogden discount rate helped Aviva slash 13.2 percentage points from its loss ratio, while the insurer was also able to improve its expense ratio by 2.1 percentage points over the course of 2018.

Welcome news

This will be welcome news for new chief executive Maurice Tulloch, who has set about cutting costs and improving efficiencies across the group. Tulloch has already set the target of £300m of annual costs savings across the group by 2022, something he described as an “essential” step if the insurer was to “remain competitive”.

Tulloch is looking to achieve this by cutting 1,800 jobs from the insurer’s global workforce of 30,000. Other savings will be achieved through lower central costs, savings in contractor and consultant spend, reduction in project expenditure and other efficiencies, the company said.

Aviva expects to spend £300m between 2019 and 2021 to achieve these savings.

In the UK, Tulloch cited having a global head office and a UK head office as an example of duplication in the company. He gave another example of where Aviva has 50 different versions of a property product.

“Simplifying the business is not only a good thing for our customers in getting clarity about the products and how we service our customers, it also gives us opportunities to create efficiencies,” he said.

“For a well-run insurance company, that’s got to be one of the things that you focus on.”

At the other end of the table, Esure also suffered from increasing claims inflation as its COR rose by almost 14 percentage points as it broke through the 100% barrier to report a loss-making 112.8%.

This worsening of Esure’s COR was largely driven by a 15.4 percentage point increase to its loss ratio, while expenses fell by 1.7 percentage points.

Esure blamed accidental damage inflation, deteriorating performance on prior years accounts and big weather hits in the first half of the year as the main reason for its poor underwriting performance, with chairman Sir Peter Wood describing the year as a “disappointing result”.

No comments yet