Complaints about terms in insurance policies have risen by three quarters over the past five years

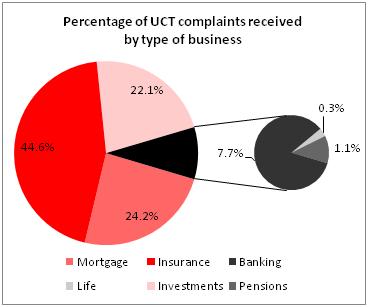

Nearly half of all complaints about unfair contract terms (UCTs) relate to insurance policies, according to data released from the Financial Conduct Authority (FCA) following a freedom of information request by law firm Pinsent Masons.

Since April 2008, the FCA and its predecessor the FSA have received 1,192 complaints about UCTs, with 45% of these citing problems with insurance contracts.

The next most complained about contracts were for mortgages (24%) and investments (22%), as illustrated in the graph below.

Pinsent Masons head of insurance and wealth management Alexis Roberts said: “The insurance industry needs to take these figures seriously. Financial services firms are legally obliged to provide clear and fair contracts, and cannot enforce unfair terms.

“The FCA may not be able to fine insurers for UCTs, but insurers risk adverse publicity and reputational damage if they don’t treat customers fairly. Further, there is also likely to be hidden cost where unfair terms cannot be properly enforced.”

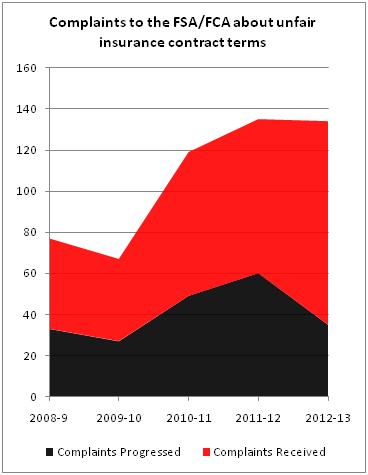

As well as an overall rise in the number of complaints received to 289 in 2012-13 from 198 in 2008-9, the number of complaints about insurance policies has also seen a marked increase.

Complaints about unfair insurance contracts have increased nearly 75% since 2008-9, with 134 received by the FCA in the last year (see graph below).

Roberts said the change in regulator and reputational damage as a result of very public mis-selling scandals had intensified the focus on the industry, and heightened consumer awareness about the ability to complain.

“The insurance industry has been under significant scrutiny since the FCA succeeded the FSA. The FCA has shifted its focus categorically towards consumer protection, and the insurance industry is increasingly under the spotlight,” said Roberts. “Following the PPI mis-selling scandal, consumers arguably have a heightened awareness of unfair treatment and are much more likely to complain and question terms and conditions.”

“It wouldn’t surprise me if this was behind the big increase in referrals seen since 2010,” he added.

Pinsent Masons also warned insurers that the rise of social media could mean UCTs cause more reputational damage if an insurer is found to be at fault.

Roberts said: “Social media is becoming an increasingly powerful tool for consumers and a bad experience with UCTs can quickly spiral into a major reputational issue for the insurer involved, and damage a well-respected brand.”

No comments yet