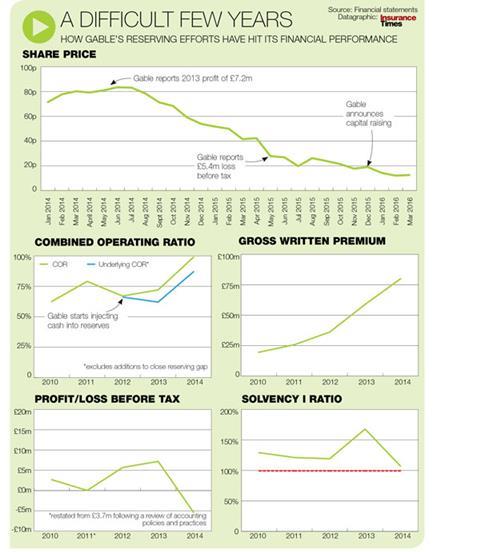

Unrated Liechtenstein-based insurer Gable has had a tough time recently. Its share price is down 88% from its 87.25p peak in 2014, and profitability has suffered as it has worked to close the gap between the reserves it holds and what actuaries think it should hold.

The company expects to make a pre-tax loss of between £7m and £8m for 2015.

In February the AIM-listed company suddenly exited two lines of business – tradesmen’s and high net worth household – on MGA Iprism.

And despite fund-raising efforts at the end of 2015, Gable did not meet the solvency capital requirement (SCR) under the new Solvency II capital rules that came into force on 1 January 2016.

The insurer has instead taken advantage of a two-year transition period allowing extra time to comply.

Business changes

Chief executive William Dewsall (pictured) also reveals that the new capital rules could mean changes to Gable’s UK business.

He says: “There will be amendments to the risk profiles we write in the UK. Solvency and capital are vital now to insurers, and under Solvency II you have to look at your profitable lines of business and where you are using your capital effectively.”

He added: “We are undertaking a strategic review of all our brokers and supporting intermediaries to see if they are meeting the standards we require.”

The question now is: how can Gable build confidence after a turbulent couple of years?

A string of high-profile failures has made brokers more wary than ever of unrated insurers. And some events in Gable’s history have, arguably, not inspired confidence.

In 2013, the company restated its 2011 results, cutting £3.7m profit to £37,000 after “a review of accounting policies and practices”.

‘Issue resolved’

Dewsall is reluctant to discuss this, other than to say: “That situation has been completely resolved and dealt with.”

And Gable’s UK underwriting agency Hogarth Underwriting Agencies, owned by Dewsall, has almost been struck off the companies register three times for filing accounts late.

Dewsall blamed his accountants and added: “It won’t happen again.”

Then there is the recent reserving and financial performance. Historically Gable has held reserves within actuaries’ range of estimates for where they should be, but below best estimate, with a £15.2m gap at end-2012.

In 2013, Gable moved to close the gap, injecting £18m by 2015. Largely as a result, Gable posted a £5.4m loss before tax in full-year 2014 and a £2.4m loss in the first half of 2015.

On top of this, the Iprism deal, Gable’s biggest in the UK, will not achieve the £100m gross written premium (GWP) over three years that it expected.

Dewsall says: “I don’t think they’ll get anywhere near it.”

Positives

But Gable has many positives. In business for 10 years, it has produced generally good underwriting results (see chart).

When reserve strengthening is excluded, Gable’s underlying profit has been strong. And with the reserving gap closed, it will no longer be a drag on profit.

While Gable missed its Solvency II SCR, Dewsall insists it will meet the SCR for the 31 December 2017 deadline.

He says: “We will make transitional arrangements. I can’t specify what they will be, but the business is well aware of its responsibilities to policyholders and shareholders.

“We are a solvent business, we are a strong business, and we will continue to be so. We will take the measures and make strategic changes to this business to accomplish what we need to do to be Solvency II compliant by that deadline.”

And Gable continues to attract business. The company wrote gross premium of £80m globally in 2014 and expects to write more than £100m in 2015.

Its five-year deal with Towergate continues, and it still writes five lines on Iprism.

Dewsall says Gable aims to pay claims quickly for its mostly SME client base, and has an 85% retention rate.

He adds: “We try to be a fair and honest company. Not the biggest, but certainly fairest.”

Gable’s challenges may not be over, but if it can tackle them it has a chance of putting its difficult past behind it.

Pass notes: Gable

What is Gable?

Gable is registered in the Cayman Islands and regulated in Liechtenstein. It was incorporated on 30 November 2004 and is listed on the London Stock Exchange’s Alternative Investment Market in January 2015. It was formed from Liechtenstein-based insurer Brown Duke, which it acquired in December 2005. Gable specialises in niche commercial lines business, and writes in seven European countries, including the UK. The company has been writing UK business since 2006.

Why has it not sought a rating?

Smaller insurers are often unrated because rating agencies’ capital requirements are onerous and obtaining a rating is an expense in its own right. But chief executive William Dewsall (above) gives a different reason. He says: “If I get an A or BBB rating the major brokers will say we tick their box and I’ll be inundated of hundreds of millions of pounds of premiums, which I can’t handle. We may change our philosophy on that but at the moment we keep ourselves unrated because we couldn’t handle the size of the business that would come our way.” However Dewsall does not rule out eventually seeking a rating.

Solvency II has been troublesome for Gable. What does Dewsall think of it?

Not much. He says: “It is possibly one of the worst pieces of legislation I have ever seen. It is certainly biased against smaller insurance companies. It could have been brilliant. It should have been written far better than it has been. I don’t think it is a consistent piece of legislation at this time.”

{kind=link}

No comments yet