Insurance Times delves deeper into the FCA’s dual pricing report looking at what concerns it could cause the personal lines broker

Briefing by Saxon East

The barbarians are at the gate.

For Rome is was the unruly Germanic tribes in the 5th century, for the modern day insurance broker it is the compliance boffins at the FCA’s headquarters in Canary Wharf.

And none are more threatened than the personal lines broker.

The regulator’s very own data and research released last week, shows how brutally exposed and fragile their business models are to FCA action.

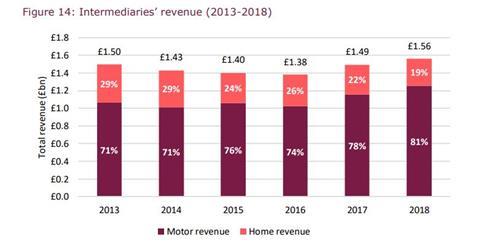

The interim pricing report released by the FCA shows that motor is the big earner for brokers compared to home.

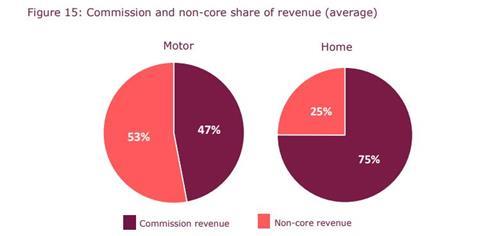

Around 53% of motor income is generated through sales of non-core products and services, the FCA data reveals (see below).

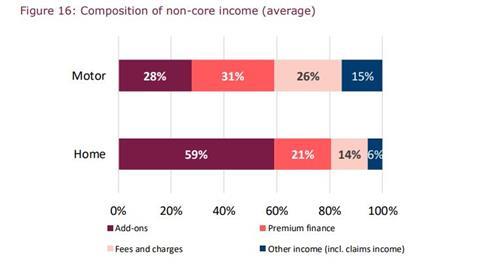

So what makes up the non-core revenue?

The FCA data reveals that the three big earners - premium finance, add-ons and fees/charges - make up 85% of brokers’ revenue in non-core.

It is clear that this part of the business model - non-core income - is crucial to the survival of many personal lines brokers.

The grave concern for brokers making a living in this area is that the FCA has already looked at, or is looking at, these vital sources of income.

In premium finance, an FCA probe into motor financing resulted in the regulator having major concerns over the way commissions are being earned.

One provider, Bexhill, believes the read across into insurance premium finance is inevitable.

The FCA has given no clarity around the issue for brokers, and the silence is worrying many.

Next up, you have add-on revenue. The regulator earlier this year stated its concerns that add-ons were not delivering value to customers.

What effect will this have on customers? Is this the start of an even bigger crackdown?

Finally, we come to fees and charges. In August, a report by GoCompare showed that these charges have risen much faster than the rate of inflation.

The FCA has already warned of charges and administration issues around tradesman. Personal lines will be worried they are next in the firing line.

In summary, the regulator is showing signs it is going to attack the non-core income which props up their business models.

Personal lines brokers are very much in the hands of the regulator, one which has shown an ever-increasing creep as each year goes by.

So much of the best innovation, customer care and staff well-being comes from personal lines brokers.

But make no mistake, they are under threat.

The regulator must act with care or it will destroy vast swathes of this part of the market.

No comments yet