![acquisition three jigsaw]](https://d17mj6xr9uykrr.cloudfront.net/Pictures/274x183/4/9/8/122498_acquisitionthreejigsaw_905211.jpg)

While insurers are becoming more innovative at covering reputational damage, the key problem remains defining reputational harm and just what customers need to be covered for

If it is possible to calculate what a reputation is worth, can a reputation therefore be insured?

Many of today’s emerging risks are challenging to indemnify because of their intangible nature. The insurance industry has responded with varying degrees of innovation when it comes to indemnifying reputational harm.

But defining reputation and brand is not always easy and companies themselves can be unsure how they want their insurance to respond.

As Airmic technical director Paul Hopkin says: “If you say ‘I want to insure my reputation’ it’s very difficult to identify the component of reputation you’re really talking about.

“If you’re a large plc it could be you want to protect your market capitalisation. In other cases what you want is your insurance to pay for, and even provide, crisis management.

“The insurance market has some way to go in developing reputation products, but also businesses themselves have to explain how they want insurance to respond.”

Managing a crisis

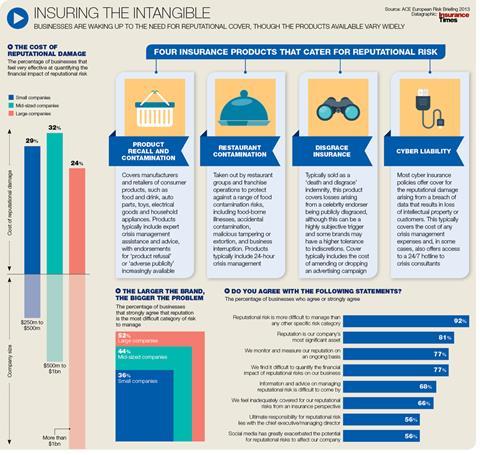

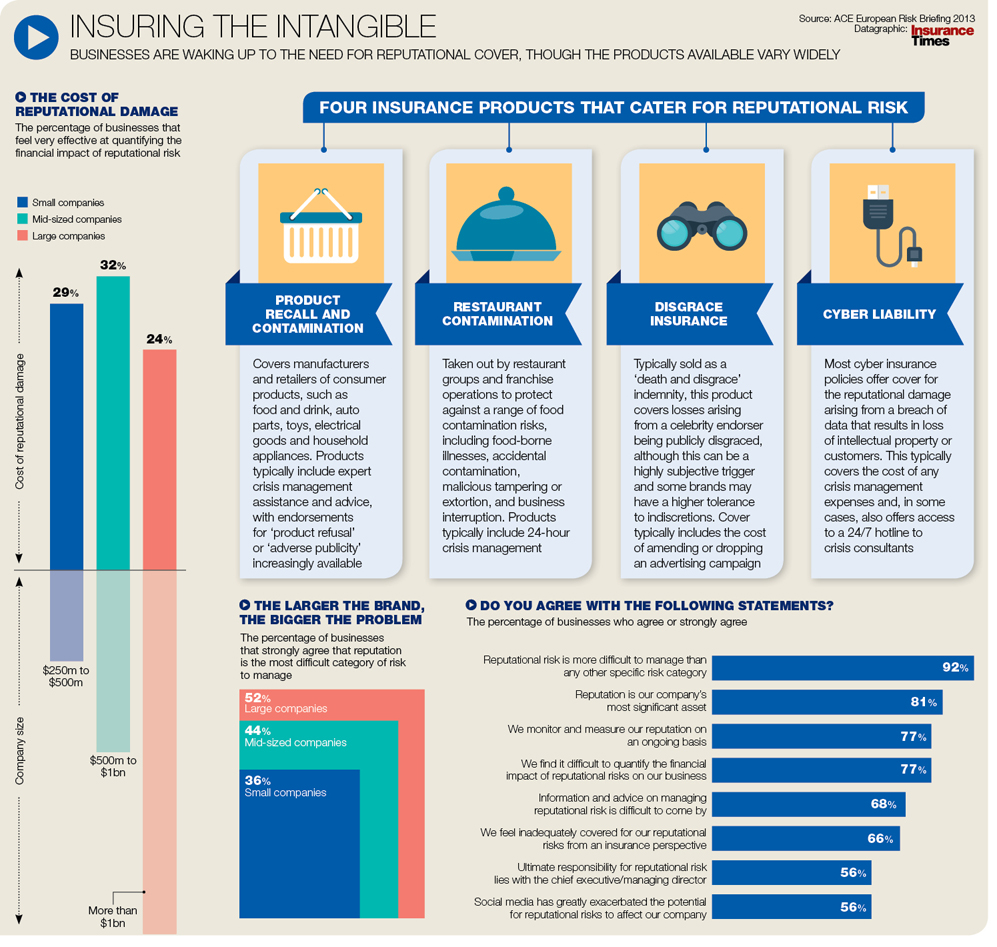

Many established insurance products cater for aspects of reputational risk. These include product recall and contamination and death, disability and disgrace cover.

Increasingly, products such as cyber liability and product recall contain reputational insurance add-ons, although these products are typically more about crisis management as a service and less about financial compensation.

Risk managers’ association Airmic once described such add-ons as “like buying a property policy that pays for fire fighters without offering a penny towards the cost of replacing a burnt-out building”.

But the product is evolving. Specialist insurers are designing standalone reputational insurance that is structured in a similar way to conventional business interruption cover. Demand is steadily growing as companies look to preserve the value of their brand.

“If I put a white t-shirt on a shelf and sell it to Joe Public I might get £5 for it, but if I put that t-shirt on a peg with a brand the public understands, I might get £30,” says Tokio Marine Kiln enterprise risk underwriter Thomas Hoad. “That [extra] £25, in simple terms, is brand equity.

“If your revenues and profits are derived from the margin you make above the cost of the generic, then damage to that brand can have ramifications that are far worse than a building burning down.”

What worries you?

Reputational covers are triggered by a list of agreed ‘perils’ ranging from product quality issues to celebrity endorsers falling from grace.

“Clients are interested in things like loss of custom from a reputational-type event and how it could affect the ability of the company to continue operating as it did before,” Hoad says.

“We talk to clients about the key things that keep them awake at night. Is it a disgruntled ex-employee, a data breach, being in contravention of some ethical issue, or a supplier who does something criminal? What worries you?

“You end up with a list, and it can be quite long and broad, and from that we write the wording. So if one of these things occurs, and it leads to a reduction in sales volume, we as an insurer will indemnify for the associated loss in profit.”

Join the debate in our new LinkedIn specialist discussion forums

Downloads

insuring the intangible

Image, Size 0.6 mb

{kind=link}

No comments yet