There is urgency to review the FSCS by April 2012, when lender repayments may spill into insurance sector

The insurance industry's key new watchdog could require an extra £200m per annum to implement the government’s proposed new early intervention approach to financial services regulation.

Last month's draft white paper on financial regulation, which outlines the shape of the Treasury's post-FSA regulatory regime, says that the new Financial Conduct Authority (FCA) will be expected to step in when financial products are being developed.

Under the new, so called "twin peaks" model of regulation, the FSA is being replaced by two new regulators, the conduct watchdog FCA and the Prudential Regulation Authority. The government's early intervention approach is designed to nip in the bud issues like payment protection insurance, which the FSA has been accused of allowing to spiral out of control due to its pre-financial crisis 'light touch' style of regulation.

But FSA chief executive Hector Sants said in a recent speech that the proposed new approach would require the FCA to be equipped with more powers and up to £200m more in running costs.

He said: "A more interventionist and proactive regulator offers the prospects of greater success but comes with the certainty of extra cost."

With many firms only visited once every four years, he said “there are undoubtedly a number of failings which the regulator has no chance of detecting in advance.”

who is stepping away from involvement in conduct issues as he prepares to take on the chief executive's role at the PRA

Sants argued society needed to debate what he described as the "trade off" between greater regulatory effectiveness and cost.

Annual inspections of the 24,000 firms, currently not subject to such regular visits, could add "at least another £200m to the cost base of the FCA". But he said the trade off could be less mis-selling and hence lower contributions to the Financial Services Compensation Scheme. The total budget of the FSA, which is funded by fees from the companies that it regulates, exceeded £500m for the first time this year.

"We need to take that into account when we are considering the cost of the FSCS. The £200m compares with the FSCS claims levied on smaller firms, excluding the cost of bank failures, of some £300m per annum for the three years to March 2012."

Sants also acknowledged the ABI's criticism that a more interventionist style of regulation could curb innovation

Margaret Cole, who is leading the 'shadow' FCA within the FSA until its proposed chief executive Martin Wheatley takes over in the autumn, said the new regulator would appoint a new senior level team to analyse how financial markets work and interact with customers.

The goals of the campaign

Insurance Times's Fair Fees campaign calls on the FSA to:

? Ring-fence professional insurance brokers from the rest of the financial services sector when establishing the new Financial Services Compensation Scheme framework.

? Exclude the mis-selling of payment protection insurance (PPI) from the compensation scheme for professional brokers.

? Ensure that the fees and levies paid by brokers are proportional to the risks they generate.

? Protect professional brokers from having to pick up the tab for the failures of the banking sector.

? Go ahead with the review as soon as possible.

The campaign continues ...

It is now a year since Insurance Times launched its Fair Fees campaign, after a tidal wave of anger at hikes in broker fees and levies.

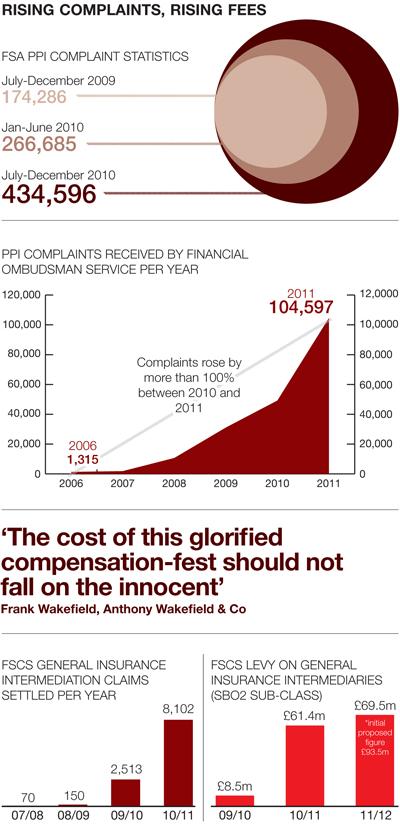

? The most galling aspect was the payment protection insurance scandal, which fuelled a massive hike in the Financial Services Compensation Scheme (FSCS): brokers now pay 10 times as much into the FSCS as they did two years ago.

? The campaign’s key demand is the restructure of the FSCS to separate general insurance brokers from those who mis-sold PPI. But progress has been frustratingly slow thanks to the FSA’s decision to suspend the review to allow for the publication of the EU’s Insurance Guarantee Directive.

? As this progress report on the campaign shows, time is running out, with FSCS liabilities from the financial crisis due to crystallise on its 2012 balance sheet. And Financial Conduct Authority plans could mean higher fees in years to come (see overleaf).

? As a result, Insurance Times has added a new objective to the campaign: an acceleration of the FSCS review – because brokers can’t wait for Brussels.

Why we support the Fair Fees campaign

Bearing the brunt

“By the FSA’s own admission, brokers are at the low-risk end of the financial services spectrum, yet we are bearing the brunt of other sectors’ mistakes. Bearing in mind that banks and retailers are the main players in this sector, the contribution should reflect this. Perversely, the FSA is not living by its own mantra of ‘treating customers fairly’ as it is clearly not treating brokers fairly.” Stuart Randall, chief executive, Ataraxia Broking

This is not our mess

“We and other straightforward insurance brokers bear no corporate responsibility for this mess, exacerbated as it is by the FSCS’s self-serving trawling for complainants. The cost of this glorified compensation-fest, mingled with the excessive spending of this bloated bureaucracy, should not fall on the innocent. It is inequitable.” Frank Wakefield, director, Anthony Wakefield & Co

FSA acted too late

“The first reason we support it is that the classification of intermediaries is far too wide – it includes organisations that are closer to banks and insurers. Second, much of the loss arising from recent failures would have been avoided if the FSA had taken action earlier on mis-selling.” Michael Ferraro, managing director, TH March & Co

Keep up the campaign

“We are a small general insurance broker. We do not affect any PPI policies, any mortgages, give financial advice or lend money to clients. So why on earth should we be penalised with exorbitant FSA fees when we do not operate in the sectors that have caused the FSA, and the government sections feeding off the FSA, to bring about these massive charges. I would be interested to receive a list of brokers that support your extremely worthwhile campaign. Well done, Insurance Times – keep up the good work.” Neil Jones-Barlow, chairman, Harbour Insurance Brokers

No comments yet