Inflation in motor and home premiums is slowing as we move into 2018

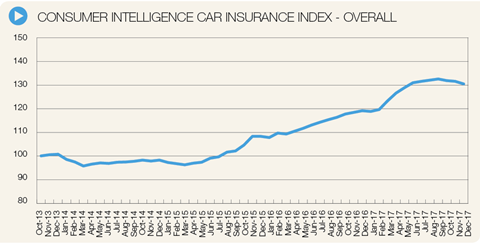

Motor insurance premiums rose to record highs in 2017, and stood at an average of £837 as of the end of the year, after peaking in September. That’s the headline finding of the latest Consumer Intelligence Motor Insurance Price Index for January 2018.

Consumer Intelligence pricing manager John Blevins, however, says price increases did begin to tail off towards the end of 2017.

“Although motor insurance premiums soared to new highs last year, shifts in government policy and the increasing uptake of telematics products saw overall premiums reduce by 1.7% in the last quarter of 2017,” he says. “Nevertheless, prices rose by 9.6% in 2017, more than three times inflation.”

These rate rises over the early part of the year were largely driven by the reduction to the Ogden rate in February 2017, as well as the government’s decision to increase Insurance Premium Tax (IPT).

More recently, however, the government has announced another Ogden review – potentially increasing the rate to a more reasonable level – as well as the IPT reprieve announced in the November Budget.

Blevins says that this has led to many insurers reducing premiums over the final quarter of 2017: “Insurers have been passing these savings back to their customers, although there remains a great deal of volatility in pricing strategy between brands.”

Meanwhile, the continued rise of telematics policies, particularly for younger drivers, has also helped keep the brakes on rate rises, with 59 of the top five cheapest premiums for drivers under the age of 25 being returned from a telematics provider. This figure falls to 11 and 4 for those aged 25-50 and 50-plus respectively.

Blevins says: “Overall, telematics brands now comprise 18 of the most competitive quotes – virtually doubling since our records began in 2013.”

Looking forward, Blevins says uncertainty is the order of the day, and a lot still depends on what changes are made to the Ogden rate.

“We could see larger decreases once we have confirmation of the Ogden rate changes”, he says. “Telematics will also continue to exert downward pressure on prices. However, the overall increase in the past year, with IPT and Ogden being sustained drivers, on top of a fluctuating pound and rising claims costs – due in part to an increase in the volume of theft-related claims – will mean an atmosphere of uncertainty could persist in 2018, and beyond.”

Home Insurance

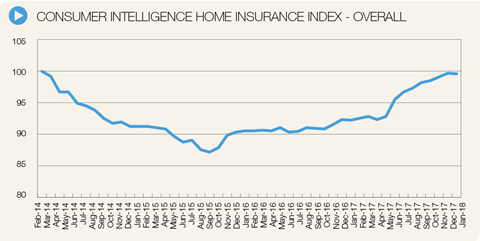

Similarly to motor insurance, the February 2018 Home Insurance Price Index from Consumer Intelligence reveals that increases in home insurance premiums have also begun to slow at the start of 2018.

“Premiums rose steadily in 2017 to a peak in December of 8.2 but came off the boil slightly in January 2018,” Blevins says. “The rises [we have seen] are not uniform, however; certain market segments go on attracting higher premiums. The worst affected policies tend to have one or more of the following traits: homeowners aged under 50, those living in London, older properties built before 1910 and homes fitted with ‘wet rooms’ and downstairs toilets.

“Overall, the average annual price of a buildings and contents policy now stands at approximately £132.”

Over the longer term, the average cost of home insurance has almost returned to February 2014 levels, when Consumer Intelligence first started collecting data on home insurance pricing, with premiums currently standing at 99.6 of the level of four years ago.

In the intervening period, premiums bottomed out in September 2015, and have risen fairly steadily since.

That is something Blevins attributes to the rising cost of claims, particularly those associated with escape of water claims. The ABI estimates that the average claims costs for water damage have risen by 31% to £2,638 in the last three years alone.

“Claim costs continue to be the main driver for premium increases, especially escape of water,” Blevins says. “The weak pound is also driving up imported material costs, which is exacerbating these increasing claims costs.

“Many ‘insurtech’ companies are trying to disrupt the home claims arena by working with insurers on connected devices designed to reduce claims costs by detecting risk before it escalates into a claim.

“Until these disruptors become more mainstream, however, we will not see the reductions in claims costs to drive prices down.”

No comments yet