M&A and integration have left many insurers with multiple inherited in-house systems that must be overhauled

‘Something new or different’: that’s the dictionary definition of innovation. Sounds pretty simple, doesn’t it? But it hasn’t been so, at least, not for the insurance industry. For general insurers and their business partners, innovation doesn’t just mean something new. It means something new that helps them to do business better, and respond effectively to changing customer needs and expectations.

For a conservative industry struggling with out-of-date systems, creaking architecture and sometimes archaic attitudes towards customer service, that’s a big ask.

Moreover, there are numerous areas where insurers need to innovate. It’s about the products they sell, the way they manufacture them and bring them to market, the way they work with business partners, and the way they respond to drastically changing customer needs and expectations.

To be ahead of the competition, insurers need to be easy to do business with. “Insurers that can provide prices in real time via partners or aggregators’ websites are going to be able to take business from those that are slower,” says SSP’s global head of value propositions, Sabine VanderLinden.

“The question for insurers is how they can embrace their business partners. Brokers are a good example: the more processes that insurers enable brokers to carry out, such as pricing or administering policies, the more they are going to use that channel. If insurers are not able to support brokers, they will go somewhere else.”

It’s a very real problem for insurers. A broker looking to develop a scheme, for example, could well choose their insurer partner based on that partner’s ability to offer the right systems to administer the scheme efficiently and bring it to market quickly. By providing in-house staff with more user-friendly tools, insurers can greatly improve their reaction times.

According to SSP, the product development cycle typically takes between 9-12 months, by which time today’s impatient consumers will be long gone. If those who are identifying, creating and launching new products have access to more intuitive tools that require less coding, time to market can be reduced to an average of 4-8 weeks for new products and 2-4 weeks for cloned products.

In recent years, insurers have had to overhaul their e-trading capabilities, developing user-friendly extranets and offering products on platforms such as PowerPlace to protect their marketshare.

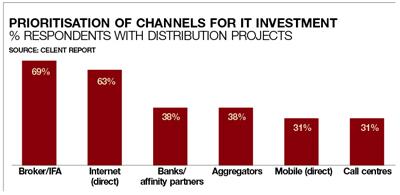

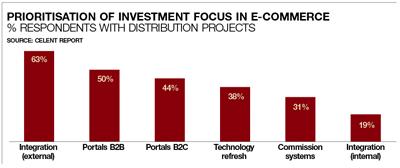

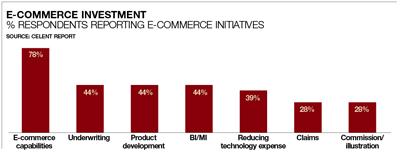

A recent report by consultancy Celent, based on interviews with 18 chief information officers at some of the UK’s leading insurers, found that 78% of respondents were investing in e-commerce initiatives. These included new or updated broker portals; more automation, including further integration with broker systems; new products designed specifically for channels such as aggregators; and expanded customer portals offering self service.

RSA is one insurer that has made great strides in the past two years, pouring significant resources into developing its e-trading capability from a slow start. RSA’s SME trading direct Dave Greaves says: “Our priority throughout the commercial business has been to make it easy to do business with us, and that has been our commitment to brokers. In terms of e-trading, RSA developed online offerings in conjunction with brokers. The main consideration in doing this was to make sure it would be as useful as possible to the very people who will be using it.

”Our online products are available on our internet site and on the major software houses.”

As well as developing new e-trading capabilities, insurers are updating their in-house systems. Almost half of the CIOs interviewed for Celent’s report, published in February, had investment planned or under way to replace core systems, such as product engines, rating and policy administration.

The report said: “One of the recurrent themes of the legacy applications architecture is how it severely limits the ability to get product changes to market in a reasonable time. Most insurers have been severely constrained by their technology in being able to respond to unpredictable business change.”

Tidy up legacy systems

One insurer that has responded to this challenge is Zurich. In a recent interview with Insurance Times, UK chief executive Stephen Lewis said: “Ultimately, if we’re going to deliver the right partnership capabilities, we’ve got to become easier to deal with. If you want to be easy to deal with, you’ve got to give your people the tools to do the job – that really requires us to tackle wholesale our legacy architecture in the UK.

“Like many of our peers in this market that have been formed through integration and mergers and acquisitions, we have a multitude of systems, and will embark on a road map to replace our legacy architecture in the UK.”

As Lewis points out, most insurers are formed through mergers and acquisitions, and thus have multiple systems to contend with. Overhauling them is not a simple process: Zurich’s programme could take three to five years, but the business benefits will be tangible.

“This is about finding best-of-breed components and starting to replenish and move to a standard suite,” Lewis added. “The world is moving, we all know that.”

Fortunately, there are systems that can be implemented on a modular basis to effectively wrap around existing legacy software, allowing firms to avoid or postpone the disruption of full-scale replacement. Back-office systems, such as policy administration, claims management and billing, can be linked to product development components, which means smoother integration, quicker time to market and better use of valuable back-office data.

It’s not just business processes that have changed beyond recognition. People now expect to be able to find information and perform transactions at any time, in any place, on a platform of their choosing. Information has been democratised, with knowledge no longer the preserve of the few. The man on the street now fully expects to be able to compare the premium he would pay to upwards of 20 insurers for the same risk. The implications of these changes are truly game-changing for the insurance industry.

The UK’s biggest insurer, Aviva, recently announced that it was returning to the aggregators, having made a strategic decision to withdraw in 2008. This U-turn powerfully demonstrates that aggregators are in the driving seat: insurers may not like them, but customers do. Those insurers that have been slow to embrace them have suffered the consequences.

Insurers have also been relatively slow to embrace mobile technology. According to Celent’s report, several insurers had or are developing apps for smartphones or mobile-friendly versions of their websites. Several had some presence on social network sites. That’s hardly an overwhelming presence, however, given the ubiquity of smartphones and social media in today’s world.

According to Celent’s Catherine Stagg-Macey, insurers have yet to find a killer app. She says: “It’s a low touch type business, so doesn’t lend itself to apps. Buying insurance on-line also isn’t quite inline with the fiddly interface of smartphones. Life insurers do better in this space, offering apps to high net worth and IFAs to check on value of investment.”

However, there are a number of ways insurers could use technology to make existing distribution channels more effective. Communication with aggregators needs to be greatly improved, to make it as simple as possible for customers to obtain quotes and complete a purchase.

Insurers could do this by allowing online shoppers to perform the entire purchasing process on aggregator websites, or by directing them automatically to the insurers’ online platform to perform the final step of the buying process. The latter would require an instantaneous transmission of customer and quote data from the aggregator website to the insurers’ own systems.

Affinity and bank channels offer value by dealing with more complicated products and engaging more closely with customers. Insurers need to improve their integration here too, to take full advantage.

They should also promote frictionless communications with brokers, who retain an important role for customers requiring specialist attention, products or services. The most effective way to do this would be for insurers to differentiate themselves by implementing portals with rich functionality, and to invest in integration with brokers’ management systems.

Of course, distribution continues to evolve. To respond to a fast-changing multichannel environment, insurers should implement a service-oriented architecture approach, which will integrate front and back-office systems and promote greater automation, and implement all applications on a scalable infrastructure.

Make the most of your data

One of the biggest missed opportunities is the enormous amount of information that insurers harvest about their customers. They are experts at using it to price products and maintain sustainable loss ratios, and are becoming more sophisticated at fraud detection. But they are still missing a trick when it comes to growing their business through new products and more targeted approaches.

“The hot topic at the moment in e-commerce is data,” says SSP chief executive Laurence Walker. “The fundamental challenge is for insurers to be able to monetise not only their own data but data services from external providers, and use those for profitable growth.”

Basic socio-demographic data is no longer sufficient to target consumers effectively, particularly as gender-based pricing has been outlawed. Insurers’ systems need to be able to access external data sources such as driving, fraud and claims records to complement their own information. This would not only give them a clearer picture of their customers but enable them to provide accurate quotes more quickly – a key advantage in capturing market share from slower rivals.

Using real-time quotation engines, whether internal, provided by a third party or cloud-based, would also improve underwriting by allowing insurers to implement rating updates across every channel as quickly as possible.

Many companies will have to overcome limitations of outdated back-office systems to achieve all this.

“There are a number of entrants to the market that can provide a combination of data packages to improve the customer experience, and allow insurers to target segments of the market based on a number of criteria, not just the information captured at the point of sale,” Walker says.

“For example, someone buying car insurance might provide their name, their car registration number and their postcode and address, and from that you can infer a whole load of information about them without having to ask. The challenge for insurers is to bring all that data into one place so they are able to use it on their own websites, and to work with aggregators and affinity providers in a multichannel environment. There is a lot of legacy IT out there: insurers were early adopters of infrastructure, which means they’ve now got large, complex systems that are quite slow. Insurers need to make sure the systems they are looking at in future can aggregate all of this data to provide a multichannel view of the market.

“We will see a continuum of change. Some of the big insurers already have a level of sophistication, and there will no doubt be niche players too. There will be the early adopters, and everyone else will have to keep up or they will be left with business that they don’t want to write. If existing players don’t get a handle on it, they will lose out to new entrants not constrained by their legacy IT.”

External lessons

So what can insurance learn from other sectors? Manufacturers may seem a world away from the business of insurance, but there is a surprising amount that insurers could learn from their rigorous approach to driving out costs and the efficiency gains they have made by automating complex processes. Insurers could overcome many of the constraints posed by legacy infrastructures by promoting standardisation, and choosing a tiered architecture and modular systems to offer greater flexibility.

Standardisation is the basis of automation, but insurers must anticipate the constraints and benefits it will bring. The first step is to undertake a deep analysis of the business and IT processes currently in place, beginning with a detailed evaluation of the business case within just one geography or line of business, before rolling it out to other parts of the business.

There are opportunities for automation at every stage of the insurance value chain, not only to improve operational efficiency but also to increase value for customers. For example, modular product design offers the possibility of greater choice and customisation for customers, while automation in pricing and underwriting enables real-time quotation and payment transfer.

The cost and time consumed by processing policies could be drastically reduced by introducing straight-through processing, and interactions with brokers and consumers could be smoothed by web-based, self-service solutions. Even in the field of claims, manual intervention and handling time could be reduced, and potential fraud automatically identified.

But while automation is already widespread, it is usually applied without a clear consideration of what will improve the customer experience. Insurers could gain the greatest competitive advantage by ensuring responsiveness, transparency and choice.

They could copy the banking industry in reorganising their businesses around customers, rather than traditional business lines. They could also take advantage of new ways of managing their hardware and software, exploring options such as cloud computing and ‘software as a service’, which allow them to outsource the responsibility of owning and running IT infrastructure.

Adopting manufacturing techniques does offer opportunities to reduce cost, but their real objective is to achieve operational excellence. Insurers must question existing principles, habits and assumptions about their business – re-engineering processes as well as technology.

How do you prove it works?

If your insurance business was a smartphone app, how many downloads would it have? It sounds like a strange question, but consider it. As anyone who uses a smartphone knows, applications are highly addictive. They’re inexpensive, quick to download, and there’s little risk if a £2 app fails to deliver.

It’s the same for developers. They can go quickly to market with a product, market it via an online store, and gather income as they rack up the downloads. Even better, they can add new functionality over the air in the form of monthly or sometimes weekly updates with popular apps.

This cycle of product innovation is highly appealing to many businesses. Some insurers have now built apps for smartphones, but apart from a few claims trackers, they tend to be good for building the profile of the brand, but less so when it comes to core products and offers.

So how can insurers build this fast-to-market, low-risk model into the product lifecycle? After all, an industry where risk aversion goes with the territory is unlikely to leap at the chance to experiment with new products and offers.

However, there’s a growing argument for greater innovation, especially now that the industry is under more pressure than ever to demonstrate growth.

Proof of concepts

For many businesses, the journey begins by working with a solutions partner that helps them to build relatively inexpensive proof of concepts, which show the value of a new strategy, while minimising the risks associated with new IT projects.

Sagicor Underwriting is a good example of a business that has put this approach into action. It recently worked with insurance solutions provider SSP to stress-test several new applications that respond to the needs of the insurance marketplace.

Sagicor Underwriting general manager and head of SME Adrian Harris says: “IT projects have a history of burning lots of money without seeing anything. Proof of concepts are an ideal way of exercising control over new projects. They demonstrate to your colleagues and customers that you’ve made the correct strategic investment decision.”

Working with a team of business and technology consultants from SSP, Harris and his colleagues were able to examine the impact of a solution that manages multicurrency transactions across multiple tax zones. They also built a web layer over the top to make the system as usable as possible.

The power to change

Harris says: “The system has been built to develop the core to the underwriters. This takes the initial work away from them in terms of making some decisions.

“But at the same time, it offers them the power to change other ways of working and gives management ability to speed the process and make the overall business more efficient.”

In short, this approach would make it easier for underwriters to be more productive. But the proof of concept does more than simply prove the value of a new technology or process. It also means that Sagicor Underwriting can get buy-in and feedback from users, and loop this back to the live solution.

For Harris at Sagicor Underwriting, this more flexible and employee-friendly approach is one of the main reasons for working with SSP.

From telematics to telehealth

Is your car just another mobile device like your phone or your tablet computer? Now that all new European cars are being fitted with telematics as standard, many in the insurance industry are starting to think this way.

Like today’s smartphones, telematics devices transmit information in real time, including the vehicle’s location and the time it is being used. More recently, the technology has come to resemble the black box recorder on an aeroplane, recording speed and braking patterns. In the event of an accident, the device will also call the emergency services, helping doctors to treat victims more quickly in the critical moments following trauma.

But there’s more to this than fancy new technology. A recent ruling by the European Court of Justice means that it is no longer possible for insurers to differentiate between men and women when underwriting financial products. As a result, women drivers could face a hike in premiums of up to 25%. Telematics could be the answer, enabling insurers to offer ‘pay as you go’ premiums that are calculated retrospectively based on driver behaviour.

A costly commodity

Critics of telematics will argue that this has been available for some years with limited success. But this fails to take into account the financial pressures on consumers today. Like food and petrol, car insurance costs have increased at the same time that economic growth has barely stabilised following the global financial crisis.

What if you could persuade drivers that their vehicle was a device for saving money? Imagine a marketing campaign that offered a significant rebate based on safer driving, appealing to households where balancing budgets is now a priority. In this respect, insurers face exactly the same challenge as any industry where customers weigh up the balance between data privacy and the benefits of sharing personal information with a business. Retail customers, for example, have used club cards to gather loyalty bonuses and other benefits for more than a decade in return for sharing data on purchases.

It’s also reasonable to speculate that the Facebook generation is increasingly confident about sharing information for personal gain.

In other words, many of the barriers to widespread consumer acceptance of telematics are starting to disappear. Recent European legislation requires telematics devices to be fitted in all new cars, meaning that the majority of vehicles will have the technology fitted as standard as drivers replace vehicles over the coming years.

The result? Insurers should start thinking about strategies that help them to compete and sustain growth by taking advantage of the technological and demographic changes that are shaping the industry.

A model for growth

But telematics isn’t the only area where consumers are using simple devices to gather data about personal behaviour. Take healthcare, for example. The growing number of monitoring devices and exercise apps for mobile phones offer a glimpse of what could be possible for insurers. Imagine the flexibility of premiums tied to healthy behaviour. Or consider the risks that would be avoided if an irregular heartbeat triggered a call to a hospital from a portable monitor.

Although not all of these predictions may come true, there’s no question that we are entering an age where small, connected devices will commonly feature in many sectors affecting insurers. As the cost of this technology continues to fall and becomes a commodity in the car industry, healthcare and others, insurers must take steps to deploy technology infrastructures that are flexible enough to help them compete.

Preparing for a future dominated by telematics won’t just protect market share in the car insurance market place, it will open the door to growth across the board.

Catherine Stagg-Macey is senior vice-president of Celent

Blue-sky thinking with cloud computing

What is cloud computing and how can insurers use it?

One way to look at it is having your data and processes hosted at a different location. You might have your music stored online so you can access it from any location. Or if you wanted to access your documents and you happen to be in an internet cafe, you can go onto the web and get them.

For companies, it’s similar to concepts like managed service provision, ‘software as a service’ or outsourcing. The issue for insurers is security. If you’re holding sensitive data about individuals’ insurance policies, you need to be sure that you know where it is and who is accessing it.

The answer for insurers could be something called a private cloud. That means that even if the data is not in their office, they know exactly where it is, who’s got it, how it’s held and what kind of security there is around it. It can be stored to their own standards.

Why would insurers use a private cloud?

If companies don’t want the bother of having to look after their infrastructure and worrying about how many computers they have or how much disk space is available, a private cloud could be an attractive option. Smaller companies probably don’t have either the expertise in-house or the money to make sure that data is stored in a state-of-the-art data centre. It could also be attractive to larger companies – the amount of power and space available is effectively unlimited, and the advantage is that they only pay for what they use.

What would a cloud-based IT set-up look like?

In terms of infrastructure, it would be very, very light. The insurer of the future based entirely in the cloud would still have some infrastructure in terms of printers and scanners. And they would still probably have their own experts on how systems work – it’s unlikely that there is going to be one insurance system that fits everyone.

Insurers are probably not going to be early adopters, but they could use cloud computing to make parts of their IT more scalable – if you run a television ad and you suddenly get 100,000 people responding, you have to make sure your systems can cope. Insurers are probably already using aspects of the cloud, such as their webpages being hosted on scalable solutions, or they might use data services hosted on someone else’s private cloud.

How would insurers switch to the cloud?

That’s one of the challenges. Large insurance companies have quite a lot of software and hardware legacy. You could move it out to the cloud, but what are you going to do with that specialist application that you’ve used for 20 years and only you can maintain, or all that specialist equipment you only bought five years ago?

There are ways of doing it that don’t require replacing the programmes you use to run your business – if you’ve got systems running on old mainframes down in the basement, you can take that system and find ways to run it on someone else’s mainframe somewhere else. Most companies with systems of any size would shift incrementally rather than taking a big bang approach.

You have to have a very focused business strategy. The first question to ask is ‘what does the right IT system look like?’, and the second is ‘do I want to look after it myself or put it on the cloud?’ They’re two separate things.

Can moving to the cloud save money?

Usually, if you strike a deal where you only pay for what you use. Private cloud providers will be able to take advantage of economies of scale that individual companies won’t. It’s not only that you won’t have to buy the kit in the first place, you have to take into account all the costs of managing it too. If it costs £800 to buy a desktop or laptop and £100 a month to rent it, you could say it doesn’t make sense to rent it after eight months, but that doesn’t include all the other costs. I’d be pretty surprised if using the private cloud or a managed service was more costly.

Duncan MacMillan is director of group operations at SSP

No comments yet