LexisNexis Risk Solutions’ Director of Home Insurance Jay Borkakoti speaks to Insurance Times on how digitisation is affecting UK home insurers and how home insurers can leverage data to optimise the customer journey.

What was the purpose of the study?

LexisNexis Risk Solutions conducted the study in order to gain a comprehensive insight into the views of home insurers on their key challenges and priorities, as well as the top trends within the UK home insurance industry such as smart home technology and digitisation.

Where appropriate, we also compared home insurer views with those of 1,500 UK homeowners who were surveyed separately. Examining the similarities – and differences – between the perspectives of these two groups revealed opportunities where home insurers could leverage data to optimise the customer journey in turn driving customer recruitment, improve retention rates, price more effectively and make operational cost savings.

What were the stand out findings that surprised you personally?

Our findings go to the heart of some of the issues facing the home insurance market, underlined by the ABI’s latest research on the scale of the underinsurance problem in the UK.

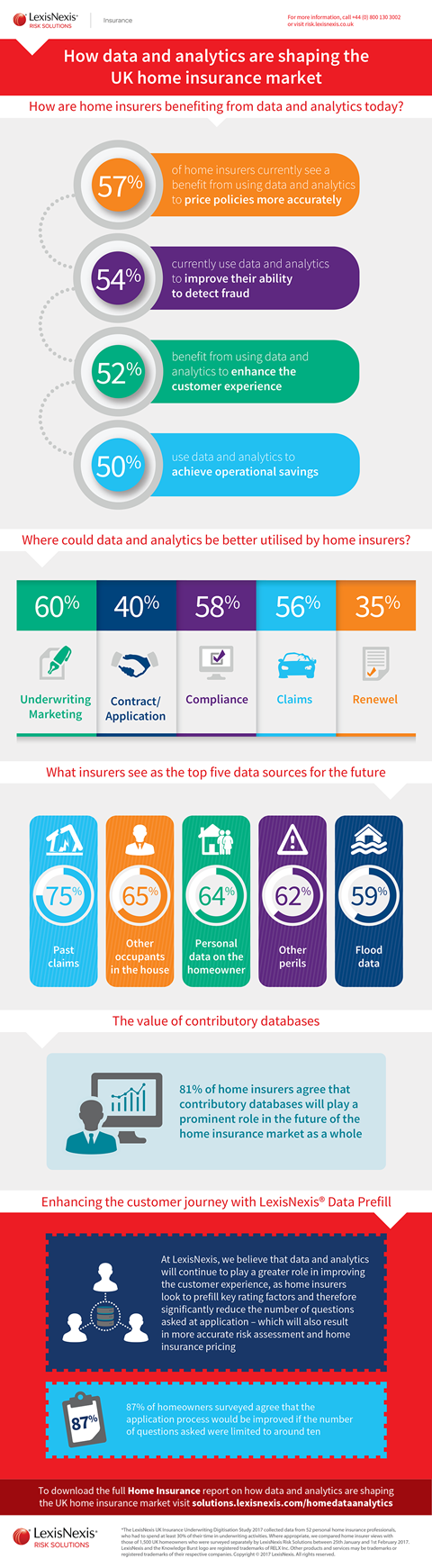

The main insight that stood out for me was the high percentage of consumers who think it is acceptable to leave out key pieces of information when applying for home insurance. 68% said they believe it is acceptable to omit or adjust information in their application to keep their premiums low. This to me aptly sums up the current status quo; the application process is so complex and laborious that customers effectively have to guess at certain questions at times which is hardly ideal. This can lead to challenges, such as under insurance for example, as consumers let default values do the work for them.

When you also consider the volume of questions customers are required to answer, it is perhaps not surprising that 87% said the application process would be improved if the number of questions asked were reduced. 10 was the ideal number based on the feedback we had, which I think is perfectly within the realms of possibility if data is leveraged within the application process.

85% of customers said they would support the idea of prefilling key property data during the application process, which highlights just how valuable this process would be to both the insurance provider and the individual.

What implications do these findings have on the future of data capture and sharing?

There is clearly a massive opportunity for home insurance providers to strengthen their validation process and improve the customer experience by leveraging data prefill at the application stage.

Using data on the property, the customer and information on past claims to prefill the application will help tackle the problem of mistakes, misrepresentation and fraud and help us move closer to “right first time” quotes.

The tide is already shifting on this front as we have started to see some insurance providers take positive steps to reduce the volume of questions at application and use this as a key marketing message. In fact, 2017 saw a key step change on this front with the launch of multiple websites with a data driven customer journey at the forefront of their proposition and it is expected that this will accelerate further in 2018.

What sources of data do you think have huge potential but are underused by home insurers?

In our study, when home insurers were asked to rank in importance the data sources that would be most valuable in assessing risk at the application stage they put past claims at the top of the list. This was followed by data on other occupants in the home and then personal data on the homeowners themselves.

Given the appetite from consumers for prefill data, coupled with the usefulness these data sources would provide to insurers, there is definitely a strong opportunity for a market-wide contributory database on policy history and past claims to help assess risk at the point of quote. This approach already works with great effect in the motor insurance market where we have identified a direct correlation between policy history and claims losses and will have huge potential for home insurers.

With more innovative smart tech capturing real time behavioural data what do you think will be the next key metric that would fall into the category of ‘personal data on the homeowner’?

Given the growth in data coming from the IoT and the potential for risk mitigation from smart home devices, this could well be one of the next big data sources for the home insurance sector. The use of this data in underwriting and pricing will be driven by consumer demand for more personalised cover and services that protect their home and the stuff they care about, though challenges remain on being actually able to use this data for underwriting purposes.

If the industry is able to obtain all the appropriate consents, without doubt this opens an opportunity to look at developing a market-wide data set of connected home data, providing insurers with a much clearer view of customer risk at point of quote and potentially through the lifetime of the policy too.

81% of home insurers felt contributory databases would play a prominent role in the future, however such databases have been created around claims data. Which additional area of insurance do you think there is scope for contributory databases?

Policy history data is proving to be incredibly powerful. We know in the motor insurance market for example that people with a gap in cover in the past year had up to a 50% higher loss cost than those that didn’t and people with a policy cancelled prematurely had up to a 33% increase to loss cost. Also, people with two or more policy cancellations had up to a 70% increase to loss cost. This has created powerful new risk attributes for motor insurers. There’s no reason the same insights could not be gained for the home insurance market through the creation of a market-wide policy history database.

The insights into the risk of individuals that can be gained through contributory datasets take the personalisation of pricing and understanding of risk to a new level, which is why the home insurance market needs to take full advantage. Shared contributed data can not only support more accurate underwriting, it can also act as a driver for new business and lead-generation.

There is also an argument for the pressing need for a revised claims database on home insurance. The key determinants of claims with home insurance are more complex than on motor and insurers accessing this superior level of granularity, and hence accuracy, on past claims data would definitely be of immediate benefit.

43% of home insurers are not seeing the benefit from using data and analytics to price policies more accurately, why do you feel this proportion haven’t tapped into this potential yet?

Many of the home insurers we surveyed see the benefit of using data and analytics when it comes to detecting fraud (54%) and achieving operational savings (50%). I think it important to understand that in home there have not been the same drivers for change we have seen in motor, so the impetus to improve has been less urgent.

However, with a number of new, wholly digitised new entrants in this arena, increasing competition is forcing real change.

The use of data and analytics is transforming the industry as a whole, helping insurers price more accurately and quickly, reduce operating costs and develop new business models. Home insurers are starting to embrace change and capitalise on data and analytics, as well as other technological enhancements in the market.

With more and more data available to insurers, should home insurance customers be concerned?

It is consumers not insurers who are driving change in the insurance market. Consumers want premiums that reflect their individual risk, they want a smoother application process and they want insurance cover for the things they value and hold dear. The delivery of data at point of contact enables the sector to meet these demands. Ultimately, the more data available on an individual the more an insurance provider is going to be able to understand their needs and give them the correct cover at a price that reflects their risk.

What data solution in your opinion has or will enhance property data understanding?

A combination of market-wide claims contributory database for property and person claims and a prefill solution will enhance the process massively. Consumers are willing to share their data in exchange for more accurate premiums and an enhanced application experience will provide a clear competitive advantage for home insurers.

What tech trend are you most excited about this year?

The continued advancement of data-driven customer journeys will take hold further in 2018 and this continues to excite me the most because it is our biggest challenge as an industry which is finally being actioned.

But also watch out for advancements across the continuum involving Blockchain. These could be especially useful when looking at how to improve the claims process.

No comments yet