Personal motor returns to profit as commercial lines worsen

RSA posted a UK combined ratio of 99.9% for the first half of 2012, a deterioration of 2.2 percentage points on the 97.7% it reported in last year’s first half.

The combined ratio generated an underwriting result of zero, compared with a £20m profit in the first half of 2011.

The poorer result comes against a background of UK flood claims, which cost the company £40m in the first half, and worsening performance in most of the commercial book.

In addition, RSA’s UK net written premiums were almost flat at £1.5bn as the company continued to reposition its portfolio.

The company is targeting growth in products where it feels it has a competitive advantage, such as household, pet and motor, and is focusing on fewer segments in motor.

Personal lines

RSA’s UK personal lines business posted a profitable combined ratio of 99.3% in the first half of 2012 despite the flood claims, although the result was 4.2 points worse than the 95.1% reported in the first half of 2011. The household, motor and pet books were all profitable, reporting combined ratios of 99%, 99.5% and 99.4% respectively.

RSA hailed the personal lines motor book’s return to profitability after four years.

Personal lines net written premiums dropped 2.5% to £661m (H1 2011: £678m) as an 18.5% drop in personal motor premiums to £224m offset increases in household and pet. Household net written premiums increased 7% to £324m (H1 2011: £303m) while pet premiums were up 13% to £113m (H1 2011: £100m).

RSA said the growth in household was driven by the acquisition of Oak Underwriting in 2011 and the deal it announced with OIM Underwriting in May. It added that the pet growth was due to “strong performance” with its affinity partners including Tesco and the Home Retail Group.

“We continue to build momentum in our affinity channel and recently signed an agreement to provide Pet and Household insurance to John Lewis and Waitrose customers in the UK,” the company said.

Pet insurance commenced in July 2012 and Household is scheduled to start in early 2013.

Commercial lines

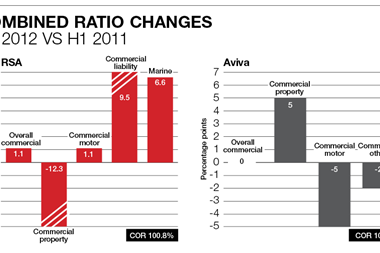

RSA posted a loss making 100.8% combined ratio in commercial lines in the first half of 2012, a 1.1 point deterioration on the 97.7% it reported in the first half of 2011.

Performance deteriorated in all lines except commercial property, where the combined ratio surged by 12.3 points to a profitable 93.4% from a loss-making 105.7%. However commercial liability performance deteriorated sharply, with the combined ratio jumping 9.5 points to 102% (H1 2011: 92.5%).

The commercial motor combined ratio increased to 108.3% (H1 2011: 107.2%) and marine to 98.3% (H1 2011: 91.7%).RSA said the motor result continues to be impacted by the loses from one significant contract.

Commercial net written premiums overall increased by 5% to £836m (H1 2011: £797m), mainly driven by property increases. Commercial motor premiums were flat at £272m.

Rate increases

While RSA’s commercial performance deteriorated, it was the source of the biggest rate increases for RSA.

Commercial motor rates were up 9% compared with June 2011, commercial liability rates were up 6% and commercial property rates up 3%.

Personal lines motor rates, meanwhile, were up 4%, while household prices rose 5%.

RSA H1 2012 division combined ratios in % (compared with H1 2011)

Total UK: 99.9 (99.7)

UK personal: 99.3 (95.1)

Personal household: 99.0 (89.3)

Personal motor: 99.5 (101.7)

Pet: 99.4 (96.0)

UK commercial 100.8 (99.7)

Commercial property: 93.4 (105.7)

Commercial liability: 102.0 (92.5)

Commercial motor: 108.3 (107.2)

Marine: 98.3 (91.7)

No comments yet