l Increasing competition is squeezing rates, and new customer discounts are raising accusations of dual pricing

Competition continues to increase in the UK’s Home insurance market driven by a prolonged period of stability, profitability and benign catastrophe claims.

However, this competition is beginning to squeeze premium rates, particularly on new business, while customer expectations are constantly changing and being raised. And insurers are also facing rising claims from escape of water as well as issues caused by Brexit and increased taxation.

“It is very competitive, a challenging market to grow competitively and profitably in, and the strategic issue is how to make money when everyone’s trying to grow at the same time,” says Mohammad Khan, UK general insurance leader at PwC. “There’s an interesting dynamic where, as motor rates come down, will it change some insurers’ appetites to grow their home book at a loss?”

Khan continues: “Home insurance has traditionally been profitable for insurance companies because people renewed a lot with their current insurer. However, virtually every single personal lines insurance company is trying to grow in home.

“Consequently, across the industry, for new business, when an insurer looks to take on that policy it will be unprofitable in the first year and they will make a loss on average.”

At present, home insurers are only able to make a profit on renewal policies while new business is unprofitable.

Khan adds: “That means the economics of home insurance can only work if you can get your customer to renew with you for at least two years and the FCA is clearly quite concerned about new versus renewal pricing.”

He continues: “For a long time in the home market people kept renewing with the insurer they were with, so there wasn’t a large volume of new policies for insurers to compete over. But, over the years the volume of potential new customers has been increasing as people look around more.

“There’s volume available for people to grow, the problem is insurers need to have a strategy for retaining those customers in the first year they are probably going to make a loss.”

In an age where many consumers can easily find a competitive quote via an aggregation website it is difficult for insurers to rely on a renewal strategy to generate an underwriting profit. And this is set to become more difficult still with the impact of insurtech on distribution channels on the increase.

Changing expectations

“Customer expectations are changing. They want a more responsive, simpler process that is ideally digital. Having a good user interface is not an advantage anymore, it is a basic requirement to stay in the game and compete,” says Tony Sault, UK General insurance leader at EY.

“Customer expectations are being set from outside the industry by their experiences of other industries. They are applying how they interact with their banks and online shops and that is informing what they expect from insurers.”

It is not only the carriers who are using these with new innovations for the changing market. Brokers are also responding well, using platforms like GuardHog, which has introduced new products into the sharing economy space.

Sault adds: “The brokers are also starting to see how they can use and explore this technology on the distribution side, so it is not just the preserve of insurers. They are using it around customer engagement, capturing data and data analytics around distribution because control of the customer is absolutely critical in this space.”

Despite increased competition from both aggregators and direct insurers, the combined broker market share for personal lines, including both motor and home has remained steady at 35%, according to Biba executive director Graeme Trudgill. This includes all types of home cover from High Net Worth to Students, from the typical family home through to social housing schemes.

Stable and profitable

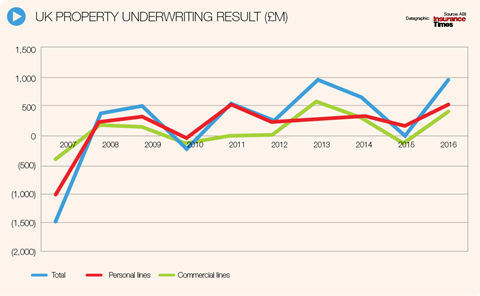

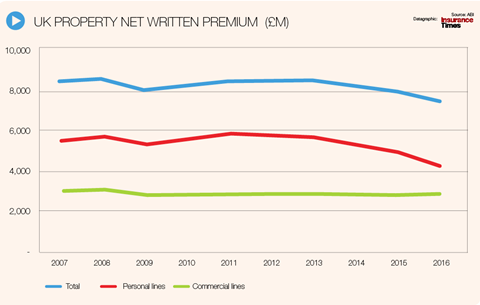

Overall, the property market was worth £12.6bn in 2016 and it has stayed broadly quite stable and profitable, according to Sault. But the market share of the top ten has increased to about 63%, up from £7.9bn in 2015 to £8.05bn in 2016.

However, Trudgill notes that the pressure on premiums has continued due to a range of factors including insurance premium tax (IPT).

“The costs of delivery are increasing due to the Flood Re levy, index-linking and IPT, without any insurer rate increase,” he says.

The Biba-Acturis insurance price index for Q3 2017 shows around a 3% reduction on the same period last year (before IPT), he says, adding: “IPT has increased again and customers are looking to reduce cost where possible, so some optional areas of cover have been cut by customers.

‘Kick in the teeth’

“We’ve seen IPT go up as well, which I don’t get. There’s no VAT on essential food items, only VAT on luxury food items. So IPT on home insurance for a customer who is simply trying to protect their property is a real kick in the teeth,” says Simon Warsop, chief underwriting officer for Aviva’s personal lines business. “God forbid they try to increase IPT going forward; that would be a step too far in my eyes.”

While the repeated raising of IPT has been unwelcome, another government initiative has proved a boon to the industry, with insurers utilising Flood Re to provide affordable cover to people in high-risk areas: although the facility has not yet been tested by a major flood loss.

Warsop says: “Flood Re has been quite a useful intervention. Most of the customers that should be in Flood Re now are probably in it, or at least getting reasonably priced flood insurance from elsewhere. The worst affected people, in the lower end of housing like social housing, faced incredibly unaffordable premiums and had effectively taken themselves out of the insurance market: a lot of those people can now afford to come back in.”

He continues: “One of the big challenges of Flood Re is making sure those people who are disengaged from insurance are actually aware that insurance is available and they can come back in.

“Then we’ve had those people who have been struggling to pay but have been manfully making sure they can pay their insurance, who have seen very significant falls in premiums; so that has been excellent news. That has been a very good result of Flood Re.”

Biba estimates that Flood Re has helped over 150,000 homes access flood cover, which is great news for so many families. However, Trudgill says greater roll out to the broking sector is still needed.

He adds: “The issue most brokers comment about in regard to household is that Flood Re is still not widely available via broker software houses. Biba is working closely with Flood Re and we are pleased there is progress coming in the pipeline.”

Although Flood Re is helping provide a solution to one problem faced by insurers, another water damage issue – escape of water – has driven claims inflation over the past 12 to 18 months.

Khan says: “Some insurers are seeing inflation rates of between 15% and 20%. The issue is not more pipes bursting, but more damage when they do burst.”

The problem is most prevalent on newer houses and extensions where the plumbing being fitted is often of inferior quality.

This is a recent phenomenon, according to Khan. He explains that water companies have been working hard over the past few years to tackle leaks and wastage from their water mains, with the result that the water pressure reaching homes has increased. Many new homes use modern push-fit pipework, “Which can’t cope with the higher water pressure.”

This is an area where new technology can help both insurers and householders alike.

“Technology in the home space means that events that used to be pretty catastrophic are a lot less so. It used to be that if you had a small leak from the shower you didn’t find out about it until the lounge ceiling fell in,” says Warsop.

He adds: “Nowadays that’s a lot simpler to detect and there are devices like LeakBot, which help alert householders to little leaks before they become something big.

“That sort of proposition coming into the market is really going to help keep the cost of home insurance down and more importantly stop people’s lives being disrupted by ceilings falling in.”

Cyber risk

The new connected homes technology could bring discounts for householders, but at the same time it can increase the risk of cyber crime on the home, with hackers gaining access to home systems through connected devices. And although solutions such as these are helpful to the industry, which has also benefitted from a lack of catastrophe claims in recent years, there are still plenty of challenges for the carriers of UK home insurance.

Sault concludes: “Brexit is having an affect of insurers being able to confidently invest in certain things as well. However, we are certainly seeing continued investment in claims and pricing, the core skills of an insurer.

“The market has remained profitable but those escape of water claims are making life more difficult. Expense ratios have started to crawl up as well. There’s a squeeze on premiums because it is a relatively soft market, but expenses and claims are starting to creep up. There’s going to be a pressure this year on home insurers.”

No comments yet