The legal minefield of solicitors’ PI

Solicitors’ professional indemnity is the soap opera of the insurance world. The dramas and plot turns of the market belie its relatively small size; rarely a month goes by without one player levelling accusations at another.

It has also become a deceptively tricky market for insurers to work in. With the 1 October deadline for renewals, insurers know exactly when they will get a stack of premium from law firms – historically a powerful incentive to play in the market.

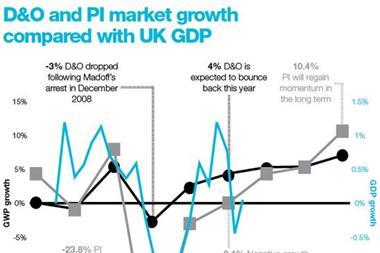

But as the storm clouds of financial crisis broke in 2008, claims against solicitors soared, fuelled by the collapsing housing market, emerging cases of fraud and the deepening recession.

ARP: the bitter pill

One particularly troublesome feature of the market is the Assigned Risks Pool (ARP). The ARP provides cover for law firms unable to get PI insurance on the open market, with qualifying insurers footing the bill for any claims.

The amount of cash insurers must contribute to the ARP is determined by their market share for the year in question.

Economic upheaval, topped by the bitter pill of the ARP, made the market so unappealing that in 2009 Hiscox and Catlin cut their losses and pulled out. Quinn, the fourth-largest insurer in the market, with an almost 10% market share, collapsed in the same year.

This left the rest of the qualifying insurers facing the prospect of soaring costs if a proportion of Quinn’s 3,000 law firms, unable to find cover, entered the ARP.

Because ARP costs are divided up between insurers according to market share, some insurers have been accused of using ‘minimisation techniques’ to artificially reduce the amount of premium they declare to the Solicitors Regulation Authority (SRA), thereby cutting their contribution to any cash claim.

This in turn would pass costs on to the more scrupulous qualifying insurers, resulting in them paying more than their fair share. Complaints have been made to the SRA.

And while there is no hard evidence of such practices in the public domain, the SRA has employed Capita to carry out an audit of insurers to weed out any dodgers. Insurers are also calling on the SRA to urgently reform the ARP.

The SRA appointed Charles River Associates (CRA) in November 2010 to conduct a root and branch review of the market, and asked for industry responses on proposed changes. The Law Society even drew up plans for an alternative ARP, called the extended renewal period (ERP).

Outrage followed the SRA’s announcement in April 2011 that although it would eventually scrap the ARP, this action had been delayed until 2013.

ABI director of general insurance and health Nick Starling said he was disappointed by the SRA’s timidity, and that it had failed to take on board CRA’s recommendations for immediate change.

Insurers were then hit with a sudden £38.6m cash call from Capita. The call related to shortfalls in ARP funding as far back as 2005, with 2008/09 accounting for £17.5m of the total.

Adding to insurers’ anger at backdated claims was the news that insurers will be liable to pay for any 2013 ARP shortfall as far into the future as 2018.

Ethnic issues

Another group making its voice heard is the Black Solicitors’ Network (BSN). Black and minority ethnic law firms can find it tough to buy PI cover, so they are over-represented in the ARP. BSN chair Nwabueze Nwokolo has said many minority ethnic firms will be forced to close if the ARP is scrapped.

Solicitors who qualify abroad and then practice in the UK are also sometimes treated with suspicion because they are seen as a higher risk as they can lack skills and local knowledge.

These issues add further complexity to this fraught market sector. And while many hope for improvements with the long-awaited SRA reforms, they are unlikely to please everyone.

To view our infographic on the breakdown of the £38.6m cash call, click on the image, right.

No comments yet