The FCA’s research into business models has thrown up some intriguing questions

Briefing by Saxon East

There are some interesting and intriguing parts in the FCA’s ‘tough, tough’ pricing interim report, most notably on which business models in home and motor make the highest profit margins.

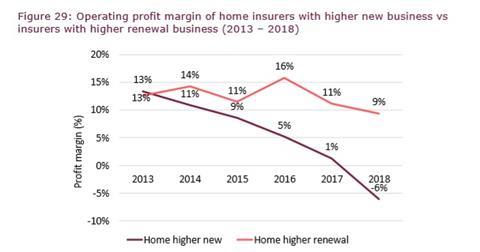

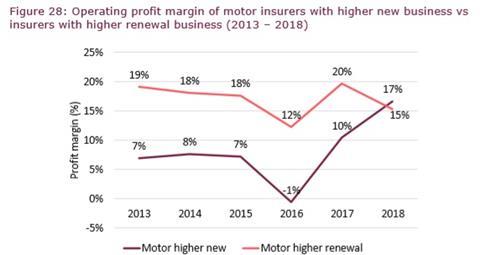

The FCA’s research into the market shows that motor and home insurers with the highest profits margins have two features.

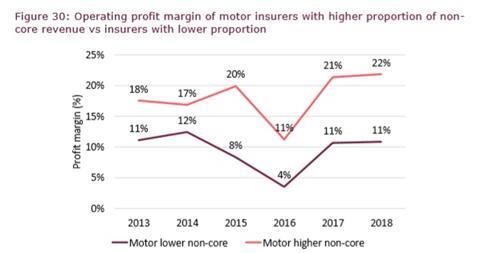

Firstly, they have a higher percentage of their book in renewals. Secondly, they derive a greater source of revenue from non-core income.

The effect on financial performance is quite striking (see below), with those players making twice the profit margins, over many years, against their peers.

It is the direct insurers who have the advantage here.

Why? The FCA suggests the insurers who uses brokers could have lower profit margins because of the greater churn, leading into lower margin new business.

Furthermore, the FCA says direct insurers have control of the ancillary income – especially the lucrative premium financing.

Intermediated insurers lose control of premium financing, plus legal expenses, breakdown cover and key cover to the brokers.

So who is the most exposed? If the FCA opts for the most punitive remedies, such as caps on renewal prices, then the most exposed here could be the Direct Line brand, which has a loyal following of renewals.

Also, those with books of loyal older customers such as AA could be exposed.

However, Direct Line would argue they have done a lot of work on ‘price walking’ already, launching initiatives that have dampened the dual pricing issue.

They may also argue that the likely rise in new prices will offset the renewal pricing hits.

If the FCA goes for a less aggressive approach, such as encouraging greater switching via ending automatic renewals, then those who play strongest on price comparison sites, like Admiral and Hastings, could benefit.

Ultimately, the situation will be clear once the final remedies land.

One thing is for sure though, if the FCA were to crack down on non-core income - legal expenses, breakdown, key cover and especially premium financing - it would have a definite negative effect on direct insures.

Look below at the graph showing the profit margin of insurers with a higher proportion of non-core revenue.

There have already been some concerns that regulatory intervention is brewing on premium finance.

This is the real cash cow for direct insurers and motor brokers.

Expect fierce lobbying from both the ABI and also Biba.

In conclusion, regulatory action on pricing is manageable.

A crackdown on non-core revenue - especially premium financing - would have a harsh outcome on certain business models.

Pray the FCA does not go there.

No comments yet