New research from Consumer Intelligence reveals which motor add-ons are most valued by consumers, and which consumers are most likely to pay for them

The insurance add-ons market is a rich source of income for the UK motor insurance industry, but changing regulations and differing consumer behaviour makes it difficult for insurers to know the best approach to market with these add-on policies.

In its new report into motor insurance add-ons, reported on exclusively by Insurance Times, Consumer Intelligence has revealed the add-on buying habits of consumers, including which demographics are most likely to value and pay for particular add-ons.

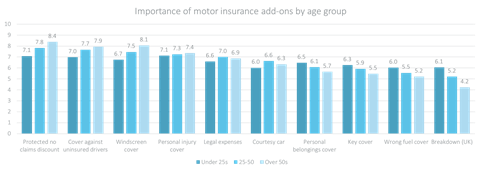

The research found that older drivers are much more likely to value add-ons over younger drivers, with policies such as protected no claims discount and windscreen cover seen as particularly valuable. These two policies were the only two add-ons to receive an importance rating of more than eight out of 10 (see below).

Consumer Intelligence chief executive Ian Hughes said it is all about the length of time these drivers have been behind the wheel, and the experience they have built up over that time.

“It is all about experience,” he said. “Younger drivers are unlikely to have many years of no claims bonus, and are therefore unlikely to want to protect it, or even understand what the concept of protected no claims bonus is.

“And windscreen cover is an odd one. Until you get a bit of experience driving and get a cracked windscreen, you don’t really realise just how dangerous that is. So the experience factor creeps in again, where people don’t realise that windscreens crack, and that those who have been driving know that, yes, they do crack, and not only that, when they do it can be really risky.”

In fact, almost two thirds (62%) of drivers over the age of 50 were willing to pay extra for protected no claims discount, compared to just 43% of drivers under the age of 25. For windscreen cover, these figures stood at 41% and 20%.

And Hughes said that insurers need to do more to educate their customers and potential customers as to the value of these add-ons in order to improve sales and maximise their revenue opportunities.

“It used to be the case that insurers would bundle in these add-ons or try and sneak it past the consumer, but now the IDD has changed that, and the downside risk is that people don’t buy a product that they should be buying” he said. “The upside opportunity, however, is that with good explanation of what the value is, without trying to sneak it past the customer but actually think about why someone would want to buy the add-on, people will buy these products.

“That is encouraging insurers to see the world through the eyes of the customer and explain the product the way the customer wants to buy it, rather than how they want to sell it.”

And this is of particular importance given how valuable these products are to insurers as a profitable revenue stream.

“For a lot of insurers, these add-ons are the only place where they make any money,” Hughes said. “So it is a crucial area, it is not the cherry on the cake – these add-ons are the cake. So it is really important that insurers understand this area, and understand how to maximise their opportunities.”

No comments yet