What has the sector learnt from the Madoff scandal and the housing crash?

The Madoff effect

What happened

Madoff rip-off hits D&O and E&O insurers

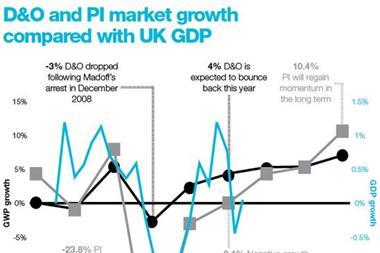

• The unravelling of New York financier Bernard Madoff’s fraudulent $65bn (£40bn) Ponzi scheme in December 2008 raised huge claims. By January 2009, Aon estimated $1.8bn of direct insured losses. Advisen estimated $1bn, suspecting many investment firms had inadequate cover.

Financial panic

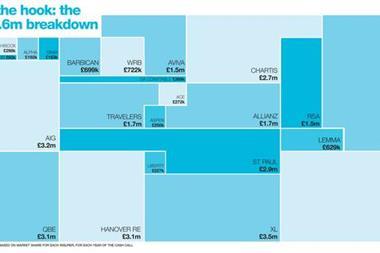

• In June 2009 insurers paid out $235m on D&O policies for claims against Madoff investor Banco Santander’s Optimal Investment Services. ACE, AIG, Brit, HCC International, Liberty International, Munich Re, Willis and Zurich were thought to have been hit.

What it meant

Litigation to escalate

• The ‘Madoff effect’ prompted fears in the industry that the financial crisis would result in a long tail of claims against D&O policies.

• The scale and sheer audacity of the fraud threatened to stoke the litigation culture to new heights and encourage aggressive, US-style litigation in the UK market.

• The drama and tragedy of the story heightened when Madoff’s son, Mark Madoff, unable to cope with the legal and media furore surrounding his father’s crimes, committed suicide in December 2010.

What might happen next

Court cases set to continue

• Madoff trustee Irving Picard is seeking $6.4bn from JP Morgan on the grounds that the bank was “wilfully blind to the fraud” and “complicit in it”. Picard is also seeking $9bn from HSBC and $2bn from UBS.

Claims may still materialise

• The predicted deluge of other financial industry claims has yet to materialise. Howden Broking Group broking director Andy Bragoli said: “The impact

hasn’t hit home. It’s not clear if everyone has provisions to cover potential claims. We haven’t seen them tested yet.”

Tail could be five to 12 years

• Shareholders may seek to recover losses by suing the board, taking several years. The board could then begin proceedings against accountants or advisers.

• There are predictions of a hardening in the D&O market this year, although with so much capacity insurers are not holding their breath.

The housing bubble bursts

What happened

Property slump hits valuers’ PI

• Property valuers found their work being more closely scrutinised after prices collapsed, leading to a rise in claims.

• Cases are emerging over alleged collusion between valuers and developers to hike up prices.

• “Professional indemnity claims often arise when people lose money, and a lot of them lost a lot on property,” Manchester Underwriting chief executive Charles Manchester says.

Valuer fees take a dive

• At the same time as premiums spiked, valuers’ fee income nose-dived compared with 2007/08, raising the cost of insurance for smaller firms to 20%-30% of fee income, compared with 2.5% during the boom years. Even for larger firms it has reached 10%-15% of fee income.

What it meant

High-octane claims climate takes hold

• Mortgage companies pumped out claims notifications with ferocity as commercial and personal borrowers found themselves unable to keep up with repayments.

• One lender sent a letter claiming that a property valued at £1m in 2006 had been overvalued, as its price later fell to £650,000. The surveyor was able to prove why the evaluation had been made at the level it had.

• In response, rather than exit the market, insurers have restricted the amount of business they write. In the past, 30%-40% of an insurer’s PI book may have been survey and valuation, but now it might be around 10%.

What might happen next

Uninsured firms forced to close

• Small firms are likely to continue to find it hard to get cover, with the cost of premiums forcing some to close. More claims and fraud are expected.

RICS considers policy changes

• The Royal Institute of Chartered Surveyors is reviewing policy wording, which can limit insurers’ ability to offer cover. “It’s a narrow choice: write it or don’t,” said Howden’s Bragoli.

Some new entrants are writing new business

• Although some insurers are exiting the market or capping their level of business, new entrants, for example Torus, are writing new business.

No comments yet