Climate change affects insurance more than any other industry, says Sandy Scott. That means we need to take a leading role in the fight against it

Insurance is arguably the business sector most directly affected by climate change.

The industry already faces significant challenges – one just has to look at the 2007 floods or the Australian wildfires. The impact of global warming on future insured losses is predicted to be profound. There is a real chance that current systems will not cope or substantial markets will become uninsurable – or both.

As people who understand and manage risk, insurers are well placed to lead the way in analysing and reducing the risk of climate change. So it is crucial for insurers to make climate change a priority, especially given the economic situation.

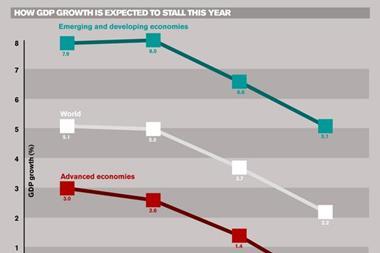

The recession puts us at a critical juncture. It seems we must choose between avoiding more strain on already stressed budgets in the short term, or investing in new practices and policies to manage what is potentially a much greater financial risk in the long term. But it is worth remembering the notion set out in Lord Nicholas Stern’s 2006 report on climate change: a risk postponed is a risk multiplied.

In reality, climate change is here now, and it is as much an opportunity as a risk for those who are wise enough to adapt early on. Action on climate change can be part of the way that the world digs itself out of the financial crisis – a “green stimulus” for growth. We can already see that this is happening:

• President Barack Obama has taken significant steps to tackle climate change in the USA. The White House is now ready to commit to real action and this will pave the way for a global coalition to emerge. As world economic players, China and India, too, will have to play their part.

• In the UK, Stern last month laid out the economic case for fighting global warming. He is calling for a “green stimulus” of spending – on green technologies, to fund low-carbon research, and to provide work for unemployed builders – to pull the world out of recession.

• These initiatives come as a new international climate change deal is under discussion. It will be agreed in Copenhagen later this year. Insurance businesses will be looking to Copenhagen for a framework that takes into account both mitigation of the worst dangers and adaptation to allow the industry to play its full role in the fight against climate change.

So, what can the insurance industry do? Climate change may seem like uncharted territory for insurers. Yet, throughout its history, the industry has fostered wide-ranging actions

to address other risks.

Insurance played a role in the 17th century in developing the first building codes with the advent of the fire marks system in London (which later spread around Europe). To mitigate claims by fire damage, insurers also established the first organised fire services in the form of the London Fire Engine Establishment (which evolved into today’s London Fire Brigade). The insurance industry has also asserted its leadership to minimise risks from earthquakes.

Today, insurers have a huge opportunity not only to identify and quantify the risks but also to develop creative solutions and products that will reduce climate change-related losses for consumers, government, and insurers – and ultimately benefit the public good.

The crucial test will be moving beyond simply managing the response to climate change in a technical sense, to taking a leading role as an agitator for change. Insurance is on the front line and now is the time to act.

The Chartered Insurance Institute’s third climate change report, Coping with Climate Change: Risks and Opportunities for Insurers, edited by Dr Andrew Dlugolecki, was published on 23 February. For more information, see www.cii.co.uk/research.

Postscript

Sandy Scott is director-general of the Chartered Insurance Institute

No comments yet