Public liability insurance offers highest renewal commission. Meanwhile, cyber is up and coming as a product bringing good profits to brokers, but more needs to be done to improve understanding

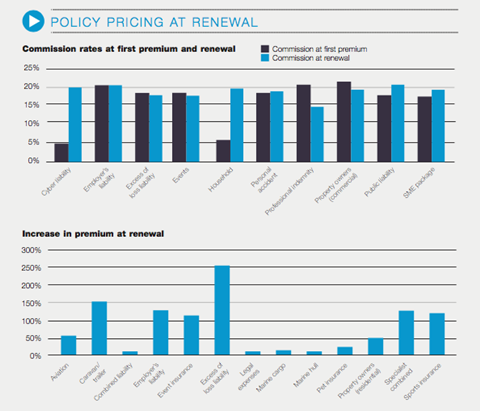

Public liability (PL) insurance offers brokers the highest commission percentage at policy renewal, according to the inaugural Insurance Times Schemes Index.

Meanwhile, Excess of Loss Liability (EOLL) insurance is seeing commission growth of more than 240% at renewal.

The Schemes Index, produced in association with SchemeServe, reveals the most profitable schemes businesses for brokers, as well as some dramatic rises in premiums and commissions across a number of key business lines.

The new index found that PL insurance offered a commission rate of 22.3%, up from a rate of 16.9% when a customer first takes out a policy.

Employer’s Liability (EL) insurance delivered the second highest commission percentage for brokers, with a commission rate of 21.7% at renewal and 21.8% at first premium, with the average amount of commission received more than doubling as a result of a 130% increase in premium from the first year of a policy’s life to the second.

EOLL insurance, which effectively acts as a top-up to the standard EL policy, also benefited from a large increase in both premiums and commission at renewal. SchemeServe chief operating officer John Price said both business lines are benefiting from the rapid growth experienced by many small businesses in their first year of trading.

“This increase in premiums at renewal could be driven by businesses growing and increasing the number of staff over the first year of trading,” he said.

“It’s well worth nurturing these businesses as brokers’ commissions for EOLL insurance also increased from an average of £15.52 at first placement to £52.69 at renewal, an increase of more than 240%.

“Those increases in staffing levels are reflected in EL product figures as well. Brokers earned a little over double the commission at renewals, with renewals averaging £963, up from the average first premium of £419.”

Cashing in on events

While the liability schemes may have been benefiting from the growth experienced by SMEs as they start out in the business world, the events insurance market has done well thanks to a summer of good weather.

“We clearly like events as a nation and with a large increase in, particularly outdoor, events this year, the amount of insurance taken out to cover contingencies has shown an increase,” Price said. “Last year the average first premium for an events insurance policy was £84. This increased to £302.41 for this year.

“The average commission earned from these extra policies has also increased to double that of the previous year, proving it to be a profitable line for brokers working in that sector.”

Cyber insurance is another product brokers may want to focus on. SchemeServe found it delivered an average commission rate of 20.1% at the renewal of a policy, up from 4.9% from the first premium.

Despite this large jump in the commission rate, Price said brokers are missing out, with many of them not understanding the product, and most cyber customers failing to renew their policy when it expires after the first year.

“The figures clearly show that cyber policies are suffering widely,” he said. “I suspect this is because no one really understands the implication of having the cover. Often there is an element of cyber cover in liability policies, and it may be that it is believed that enough cover is already in place.

“Some basic cyber policies only cover the cost to fix the attack, but not the wider repercussions of loss of trust by customers in businesses that suffer data breaches, for example. Of 170 policies sold a year ago, only two renewed, and both at a lower value.”

Price said that to capitalise on the opportunity presented by cyber insurance, brokers and the wider industry need to do more to educate customers and make them aware of the consequences of not having adequate cover in place.

“The profession needs to work much harder at explaining the high risk and balance the ‘it couldn’t happen to me’ thinking with the importance of having appropriate cyber cover in place,” he said.

“It needs to be very near the top of businesses’ lists of things they need, and not at the bottom as an afterthought.”

Data provided by SchemeServe, a leading technology solutions provider for the insurance market and a specialist in the creation and online management of delegated authority schemes.

No comments yet