The regulator’s own figures reveal the extent of lost revenue facing UKGI

Briefing by content director Saxon East

Saxon East is content director at Insurance Times

It is enough to make the mind boggle.

Looking through the FCA’s pricing reform papers, some startling predictions are made by the regulator.

Here are three:

* Compliance costs to the industry are £1bn

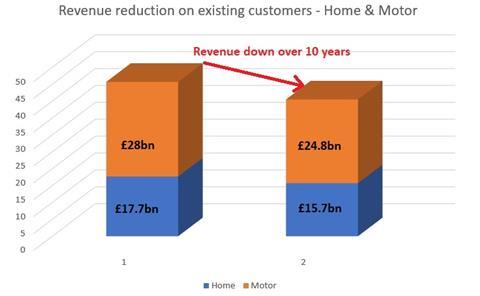

* The regulator estimates that its pricing reforms will lead to a reduction of revenue between £3.7bn and £11bn over the first ten years.

* Loss in revenue from existing customers likely between £5.3bn and £6.7bn

Let’s suppose for a minute that the final revenue reduction does reach £11bn. Now let’s put that relative to other major events to hit our industy.

* The £11bn is twice the size of the Ogden changes, which were estimated at between £5bn and £6bn

* The £11bn is almost four times the size of the £3bn costs from the 2007 great floods

* The £11bn is equal to the very worst case estimate, put forward by Willis Towers Watson, of what Covid could cost UK insurance firms

The point being made is that, as if we didn’t know already, the FCA’s pricing reforms are an immense event for the industry.

In fact, the reform could turn out to be the biggest event in the recent history of UK General Insurance.

What softens the blow considerably is that these estimates from the FCA are the aggregate amount over ten years.

Insurance has a long time to absorb the blow, unlike the floods or Covid where the claims impact is much more immediate.

In conclusion, it appears the FCA is looking very intently on value offered to customers.

It will make insurance firms bear the cost - however large - if it leads to better customer treatment.

Where it looks next is the question people are already asking themselves.

No comments yet