Industry leaders talk about the problems – within the sector and outside – in beating fraud

Richard Davies, group fraud risk manager, AXA UK

We can spend forever defining fraud. What it requires is a definition that is good enough. Every project I have been involved in, we have a debate on how many angels can dance on the head of a pin. It’s a complete and utter waste of time – we just need to get on and do something.

I also think the industry is insular, we have organised ourselves in adversarial ranks and we have not been prepared to recognise that fraud is a problem that doesn’t just affect insurers, or the supply chain, and doesn’t need to be sub-contracted to loss adjusters and investigators. It needs to include the entire community involved in underwriting and claims.

We are also not engaging with enough of the stakeholder sectors – the broking arm, the aggregators, the legal profession, the investigators – in coming up with a solution.

Consumer education is absolutely key and I accept that not enough has been done by the industry about changing the current mindset that [insurance fraud] is somehow acceptable.

Scott Clayton, claims fraud and investigations manager, Zurich

We were pretty confident about getting a customer sentenced on a case, but this guy – who had 24 previous convictions – walked out of the court sneering at us. If we can’t get guys like these locked up, what chance have we got?

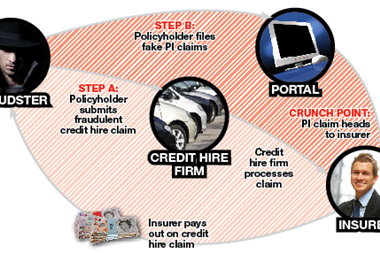

On the civil [justice] side, there’s nothing in the law to stop people exaggerating injuries; it’s a no-lose gamble. It goes into the question of how many personal injury claims are 100% genuine and how many are exaggerated.

We’re scared to run cases on low-speed impact clams because they’re not economic to run. You end up paying them and it’s a never-ending cycle.

Glen Marr, director of fraud, First Central Insurance Management

On consumer education, we’ve done nothing as an industry about what is acceptable and unacceptable behaviour. We don’t message very well about the ramifications - it’s tucked away in the small print.

We don’t understand the size of the problem; we don’t know the true extent of fraud.Ghost broking is biting the insurance sector, which should have seen it coming. It’s causing arguably some sophisticated problems for insurers, and the people who are committing it are not that sophisticated.

On problems of data sharing with the public sector, having talked turkey with the Department for Work and Pensions, it’s about bureaucracy.

They have legislation to share information, but they wanted legal advice to tell them what their own legislation meant – they tie themselves in knots. The ABI has a key role to play in engaging with the government.

Soundbites

Consumer education is key

“We should not lose sight of the great amount of work being done across the insurance industry. In terms of where the gaps are, a lot depends on how successful [the City of London fraud unit] is.

“Another key area is how the insurance industry manages its data: there is far too much focus on validation of claims at the claims stage and not enough checking at the quotation stage.

“Consumer education is absolutely key and I accept that not enough has been done by the industry about changing the current mindset that [fraud] is somehow acceptable.”

Mark Allen, assistant director of markets and regulation, ABI

Joined-up thinking

“My biggest concern is that we focus too much on competitive advantage: we don’t have a collaborative approach in terms of targeting the identifiable individual and penalising them.

“If we are declining business in one area it’s just going to another broker or insurer. You are just moving the fraudsters along a merry-

go-round and not getting to the root cause of the problem.

“There is anecdotal evidence of the social acceptability of fronting policies: parents think they are helping their children. If we can get to the heart of some of that, it will bring costs down for the industry.”

Stephen Gaywood, head of counter-fraud, AXA Personal Lines

No appetite outside of motor

“The Insurance Fraud Bureau’s strategy is all about the status quo. We have lost somewhere down the line the ability to track new trends.

“Two years ago, I started to talk about organised casualty fraud. I am waiting for a supplier to say we have experts in this, but there’s no appetite because that’s not where the revenue is – it’s all in the motor area.”

Mihir Pandaya, fraud manager, Allianz

No comments yet