![acquisition three jigsaw]](https://d17mj6xr9uykrr.cloudfront.net/Pictures/274x183/4/9/8/122498_acquisitionthreejigsaw_905211.jpg)

How regulation has impacted schemes since 2015: Delegation and distribution

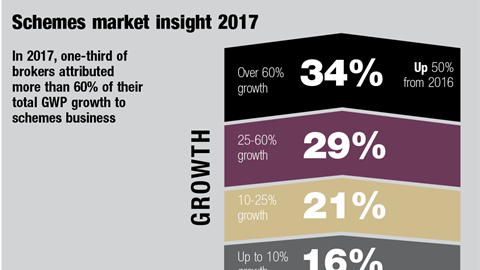

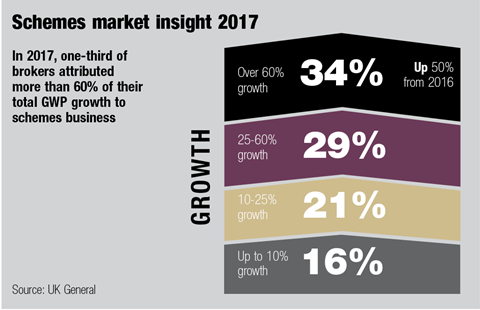

There appears to be a “technology disconnect” between what schemes brokers believe will happen with distribution and what they are currently doing about it, according to UK General’s scheme broker survey.

It found that while 69% of brokers thought social media, mobile distribution and personalisation of quotes are the trends most likely to have a profound impact on schemes distribution in the next three years, only 8% currently transact business using these methods.

Many continue to prefer traditional, manual methods, with nearly two-thirds preferring to transact business over the telephone.

Part of the resistance to an automated online form of distribution may be the desire to retain delegated authority status. “A lot of insurance carriers – particularly on the motor side – want to put customers through their own online system,” says SEIB managing director Barry Fehler.

“Which is very time consuming for us – we’re much better off with a binding authority.”

Following its thematic review in 2015, the FCA found “failings” within the delegated authority relationship and many of these are now on the way out.

Although not universal, within the review population the FCA found a series of control weaknesses, resulting in the potential for unfair outcomes at all stages of the outsourcing cycle.

Profound impact

This development among others is having a profound impact on schemes business.

“Delegation needs to be treated with respect by both parties and a good balance between conduct, good customer outcomes and being agile enough to move quickly in testing and launching new ideas should be sought,” says RSA head of schemes and deals development Katie Balme.

“When you’ve got an automated online method of distribution, it’s mainly the manual schemes that have delegated authority and they are very expense heavy,” adds Accelerate Underwriting managing director Scott Brown.

However, other schemes brokers are embracing change.

“There are brokers out there who are developing schemes that are very much driven by data – collating data and driving underwriting decisions and product design based on data – we do see that going on in the market,” says Brown.

“The best schemes are the ones that are built on data,” he says.

“Nowadays it’s easier for us to determine whether or not they’re going to work because we’ve got data that we didn’t have 15 or 20 years ago.”

Others think the Ogden rate change is more likely to impact schemes business in the near term, although it is still too early to tell how it will all play out.

“This has caused a fair amount of uncertainty in the market,” says Fehler. “We had a scheme lined up and ready to go and we’ve had to re-jig all the figures to take Ogden into account as they’re looking for lower combined operating ratios.”

In February 2017, the Ministry of Justice announced it would cut the discount rate to minus 0.75% from 2.5%, taking effect from 20 March.

The industry had widely expected the rate to be cut to between plus 1.0% and 1.5%.

“All the carriers are reviewing their rates as they come through,” adds James Hallam chief executive Paul Anscombe.

“It’s still not fully hit and the discount rate is forecast to change again in the future so a lot of the market is holding fire to see where we end up.

“Certainly people are reviewing their reserves on existing claims but the pricing piece on this is quite interesting.”

No comments yet