Hyperion spending millions to buy back equity from ageing staff and ensure more shareholder employees of the future

When JLT completes its sale to Marsh this year, Hyperion will become the world’s largest non-US owned insurance intermediary.

As the group celebrates this feat in its milestone 25th year, founder and group chief executive David Howden has his sights set on securing Hyperion’s next 25.

Howden has already given his commitment to the Hyperion board that he will lead until at least 2028.

And the group is pouring all of its profits into buying equity from existing aging employee shareholders, in order to ensure the next generation of workers can claim their stake and help the company thrive.

Hyperion spent £63m last year on buying back equity. Currently 650 employees own a 44% share of the group, but Howden wants 1,000 of the group’s 4,500 staff to be shareholders within the next 3-5 years.

“We didn’t pay a single penny in dividends last year, nothing,” Howden tells Insurance Times. “All our money was either invested in acquisitions and future growth, or in buying back stock.”

Independent

By redistributing equity to the next generation, Howden says it will enable to the group to keep regenerating and remain independent.

Howden said: “We are absolutely committed to employees owning part of the business.

“To do that you’ve got to look at succession planning. Why do businesses end up flogging? Because all the equity is held by the people who retire.

“So we’ve got a commitment that we are going to buy back our stocks in order to allow the up and coming generation to invest in the company.”

Hyperion has two private equity minority investors in CDPQ and General Atlantic, each with a 26% share, which Howden says is likely to remain static as the company maintains its acquisitive appetite.

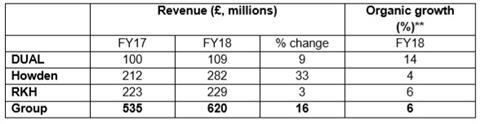

The release of the group’s full year results up to September 2018 revealed the group spent £145m on investments and acquisitions, in a period when the debt to EBITDA ratio increased to 4.3 from 3.8.

Model

But Howden insists this is within the ratio of between four and five that the group aims for.

He says this suits the Hyperion model, and claims it differentiates the group from industry consolidators.

“Our M&A strategy has always been selective,” he says. “We are not a consolidator, which is why we have very low debt. If you want to be a consolidator you need to be leveraged at six or seven times.

“That’s not our model, we’re not a leverage business. Four times is not high leverage.”

On multiple occasions Howden uses the phrase “it’s about long-term value, not short term gain,” and unlike consolidator PE houses, Howden says CDPQ and General Atlantic are committed for at least 5-10 years.

“We’ve got a business model that is very much about employees,” Howden says, maintaining that this is a strategy that will ensure the business can remain independent.

Investing

The agreement to reinvest profits into buying back equity and investing in the next generation is testament to the group’s commitment to prioritising long-term value.

And with the launch of a fourth business in the group – data and analytics company Hyperion X – the signs are that this attitude permeates throughout the business.

Adding to the MGA DUAL, retail and wholesale broker Howden and London market specialty and reinsurance broker RKH, Hyperion X will service all three companies.

The group has already invested £50m in Hyperion X since announcing the new business in October 2018, and is likely to invest more.

Howden says the business will “probably” make a profit in its first year, but says he “doesn’t care” if it makes a loss, insisting the venture is about embracing an increasingly digitalised industry.

He said: “Whether it makes a profit or loss will largely depend on how much we choose to invest.

“It will require investment, but we’re not really interested in next year, like we’re not interested in three years’ time either. What I’m interested in is five, ten, 15 years’ time. Hyperion X will transform our business over that time, and that’s why I’m doing it.”

Insurtech

Hyperion X is also intended to manage Hyperion’s third-party insurtech investments, as well as incubate its own start-up ventures.

Howden said such a business was necessary for successful integration of new technology within a business, and that acquiring insurtech start-ups is not sufficient.

He said: “Everyone knows the technology is out there but what’s difficult is integrating it into the business.

“To do that you’ve got to have insurance people deliberately brought into it. That’s why we asked (former RKH chief executive) Barnaby Rugge-Price to lead it.

“If you expect to simply just buy an insurtech business and expect it to seamlessly integrate into your existing business, that’s a road to nowhere.”

With the latest results revealing organic growth at 6% overall for the group, revenues increasing 16% on the previous year to £620m, and EBITDA increasing by 19% to £181m, Howden says he is delighted with the current state of the group.

Unconcerned by the group’s B2 rating from S&P and Moody’s, Howden is confident that taking a long-term strategy for the group can continue to deliver strong results.

He said: “The real secret behind our success is our differentiated business model. This is something that is going to be not just popular in insurance, but also beyond that.

“We don’t think short term gain is right, and having a long-term view doesn’t deliver worse results, it delivers better results.”

No comments yet