Ardonagh’s financial results for 2020 stated strong revenue growth and booming earnings, but, as is often the case with financial results, the full picture is more complex

Five years ago, Towergate suffered a near-death experience. Key insurers refused to trade with the broking giant as it ran out of cash. Only a capital injection from its new owners at the 11th hour saved the business.

Fast forward to today, and the headline figures appear to show the acquisition-hungry business, rebranded as Ardonagh, in much better shape.

There are booming earnings, fast-growing revenue and ample liquidity. But a closer inspection of Ardonagh’s accounts show a more complex picture.

Ardonagh’s financial situation can be broken down into two areas: financial performance and financial health.

On the former, the two key areas are revenues and earnings. Ardonagh announced last month that full-year 2019 revenues had grown 26.6% from 2018.

But, on a like-for-like basis, including the annualised impact of acquisitions and excluding corporate and foreign exchange items, the business is broadly flat. Ardonagh’s revenues grew from £663.6m to £668.5m – an increase of 0.7%.

The business showed good growth in advisory (+3.5% to £223.8m) and specialty (+8.1% to £142.5m), but this was pulled back by a decline in its largest unit, personal lines (-4.9% to £294.2m).

A main factor driving the decline in personal lines is the continued fall in income from Swinton. Ardonagh said this is a result of acquiring a business with downward income trajectory, with branches closing and not all customers seamlessly moving online.

Ardonagh is organising new products for Swinton and integrating it into Ardonagh’s wider personal lines business, which it believes has superior data and call centre abilities. Over the second half of 2019, Ardonagh managed to stabilise this decline in policy count and income at Swinton and said the business is performing better than projected.

Organic growth excluding Swinton is 3%, it said.

Cost savings have also been made to improve the earnings and margin. Ardonagh expects the business, acquired at just three times earnings, to stabilise further in 2020, improving overall group revenue.

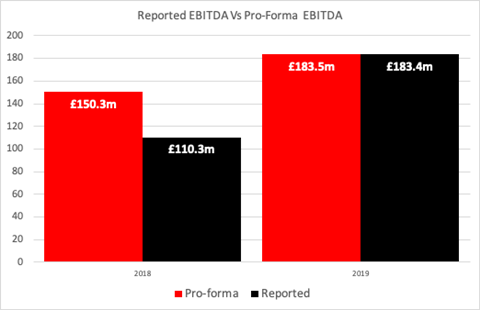

On earnings, Ardonagh reported its pro forma adjusted-run rate earnings before interest, tax, depreciation and amortisation (EBITDA) – which includes acquisitions and strips out certain costs – growing 22% from £150.3m to £183.5m.

Ardonagh said earnings margins improved 6.6 percentage points, but this is 4.8 percentage points on a like-for-like basis. Some of these improvements were due to a £12.9m accounting change.

The biggest driver in improving earnings quality has been the firm’s cost reduction programme, saving £21m last year.

In summary, despite the headline figures showing strong growth, revenues are flat on a like-for-like basis.

The anticipated stabilising of Swinton’s income will be key to improving overall group revenue performance.

Financial health

On financial health, Ardonagh has available liquidity of £181.7m, but the cash position has decreased from £125.6m to £61.7m.

With adjustments, the firm’s leverage position has £1.1bn debt, around six times reported EBITDA – with roughly half of this due to be paid back in 2023.

Moody’s said in a note at the end of last year that Ardonagh’s leverage was “very high”. The ratings agency said the leverage, with interest payments totalling around £90m each year, are among the group’s biggest challenges. It has flagged up the possibility of downgrades if debt to EBITDA ratios are not kept under control.

Ardonagh said that once its run rate savings – those expected to be realised over the course of 2020 – are included, it brings the ratio down to around 5.2 times EBITDA.

Moody’s said: “The group’s strong position in the broking market and coverage of the insurance value chain are key credit strengths.

“Ardonagh also offers niche insurance products to retail and small and medium-sized commercial clients, where it benefits from its extensive footprint, influence over carriers and attractive commission rates.

“Ardonagh is well diversified in terms of product line, with a focus on specialty products and niche segments that generally cannot be bought directly

from insurers.”

Moody’s continues to list Ardonagh’s financial ratings outlook as stable.

The broker’s diversification will stand it in good stead when it comes to handling the global economic uncertainty after the Covid-19 pandemic, with no more than 12% of Ardonagh’s gross written premium coming from any one class of business.

’We’re well-positioned’

Announcing Ardonagh’s full-year results for 2019, chief executive David Ross said: “As we look ahead to a period of domestic and global uncertainty, all the work that has taken place since the formation of the group to upgrade our systems, diversify our business and connect our people and clients leaves us well positioned to adapt and remain resilient.

We will continue to serve our clients however we best can.” Moody’s has also pointed to Ardonagh’s recent acquisitions as a further point for optimism.

“We view Swinton, acquired on 31 December 2018, as a good strategic fit that strengthens Ardonagh’s personal lines brokerage business,” it said.

“We expect Swinton’s cash generation to improve operating cash conversion for the division. Swinton also brings a larger scale and a strong brand that will benefit the whole franchise.

“Ardonagh estimates that the business, on a pro forma basis, contributed £32.4m adjusted EBITDA, excluding one-off costs, in 2018. Cost reduction and the integration of Swinton were nearly complete as of September 2019, with all branches closed as planned.”

What next for the consolidator?

Towergate nearly went bust five years ago, writes Insurance Times content director Saxon East. The consolidator’s high debt interest payments and decline in cashflow put its very existence in peril.

Fast forward to today, and the firm still has high leverage and interest payments. On the positive side, there is enough liquidity available – £181m – to ensure there is no repeat of 2015.

The main challenge to Ardonagh’s financial health is its £1.1bn debts, with repayments by 2023.

Ardonagh can’t pay that off from its own funds. The options are to roll over the debt or sell the business to new owners. Could the pandemic, a wrecking ball to the economy, change all that by making the corporate bond market a tougher place to find funding?

And if there are new buyers, who will they be in the pandemic’s aftermath? Aon, Willis and Gallagher are out of the picture, having done their own deals. The most likely option is another private equity owner.

In the meantime, getting the best out of its individual units, including the largest, which is UK personal lines, will be key. Ardonagh has bought heavily into this highly competitive area of insurance.

The benefits of Swinton have yet to fully transpire, with the acquisition dragging down overall like-for-like group revenue. Ardonagh is confident this will stabilise in 2020, and the earnings margin on Swinton has already increased substantially with cost savings.

On earnings, the improvement is being driven by reduced costs, with £71m saved since 2017.

Ardonagh has many moving parts – the integration of Swinton, the cost reduction programme and £1.1bn in debt that will need to be dealt with by 2023.

Although in better shape, it still remains a work in progress.

No comments yet