Amanda Blanc faces a number of challenges as she takes over the helm at Aviva, but none are bigger than the problem of how to deal with the sclerotic UK business’s life and savings arm

“Aviva? It’s a melting ice cube,” one expert, who worked inside the company for years looking at its strategy, tells Insurance Times.

“I would put the whole UK life and savings business into run-off. Stop accepting new business.”

The fact such drastic action is even being discussed shows the challenge facing new chief executive Amanda Blanc.

So what exactly are Aviva’s problems, and how can Blanc fix it?

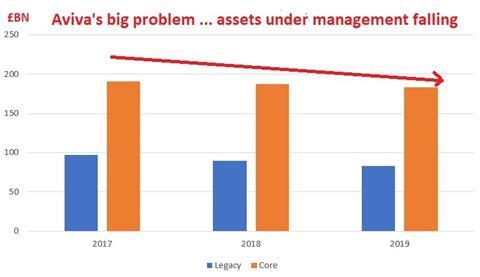

Aviva’s big problem

An investor who bought Aviva’s shares five years ago is down 40%, despite a massive bull run on the stock markets.

But the share price is the symptom, not the cause.

Ex-boss Mark Wilson argued Aviva gets a big capital diversifiction benefit and is better off together

After speaking off the record to a dozen analysts, shareholders and Aviva directors, they all point to the biggest problem: the UK protection and savings business is either going backwards or growing at a glacial pace, depending on how you look at it (see graph below. source: Aviva year-end presentations)

Importantly, it’s viewed as going nowhere by large investors, who have their own research teams running the numbers.

Investors simply have better choices than Aviva, and they are wary of its UK protection and savings arm, 60% of its £3.2bn profits, being so weak.

Combined with the covid fallout, Aviva’s over-leveraged balance sheet, and £600m less future profits as longevity releases dwindle, the perfect storm has hit Aviva’s share price.

It currently stands at 286p – nearly its lowest level in ten years.

And a significant proportion of Aviva’s shareholders and analysts want bold action.

Long-suffering shareholder and investor activist Philip Meadowcroft says: ”George Culmer and Amanda Blanc have no ties with Aviva’s tainted past or its employees.

”They are in pole position to conduct what could be a brutal hatchet on Aviva’s sclerotic structures and some less than spectacular operating units.

”There can be little doubt they have an unparalleled opportunity – maybe the last one – to pull Aviva up out if its decline.”

Breaking up is hard to do

Blanc has a range of options, with the most radical being a break up.

Aviva is basically made up of three parts.

The largest is UK protection and savings (including Aviva Investors); next up in size is European/Asia life and finally, the third and smallest part is general insurance.

All the businesses make up Aviva market capitalisation of £11bn.

By splitting up Aviva, analysts believe it could get £5bn for the general insurance and £15bn for the rest – nearly doubling its market capitalisation to £20bn.

But there are two problems.

Firstly, Aviva has £7.4bn debt that needs accounting for.

Secondly, and most importantly, Aviva also gets a ‘diversification benefit’ under Solvency 2 rules for having a mix of businesses.

As former boss Mark Wilson correctly argued, to stand these businesses alone would need billions in extra capital.

All three previous chief executives Wilson, Maurice Tulloch and Andrew Moss feared a clean break could actually leave Aviva worse off.

The easiset solution would be for a takeover of Aviva, but as Investec analyst Ben Cohen notes, nobody will buy the business because of UK savings and protection.

His analysis paints a picture of Aviva being caught in a strategic no man’s land.

Cohen, in an in-depth review of Aviva in 2018, which remains just as relevant today, wrote: ”While the strategic rationale for the group’s structure is perhaps no weaker than any other European composite insurer, the key rationale of its structure – diversification – is likely to provide an on-going barrier to unlocking value through the break-up of the company.

”While performing adequately, albeit with the prospect of declining capital generation, the lack of interest from international insurers in the UK Life market (indeed, most life markets), is the biggest barrier to a full take-over.”

Bit by bit break up

So what can be done to solve the problem?

One idea widely discussed by Aviva experts who have analysed the company carefully is to dispense of the problematic UK life and protection business bit by bit.

The first and most obvious action would be to seek a buyer for the legacy book, which has £84bn assets under management.

Run-off specialists such as Phoneix might show interest. Phoenix will soon complete a deal for rival ReAssure, with former Aviva life head Andy Briggs taking over as Phoenix boss - meaning a legacy book deal is perfectly set up.

Ex-Aviva UK boss Mark Hodges runs ReAssure but is stepping down soon

Aviva currently runs at four times price earnings.

If Blanc sells the back book for eight times profits, it could make a nice turn.

She would also have some capital to throw a big dividend bone to Aviva’s long-suffering shareholders.

However, there still remains the even bigger problem of what to do with the remaining bulk of the UK protection and savings arm.

Nobody is likely to take the business as a whole, but there might be a buyer for the ‘with profits’ part of the book.

That could get Aviva another one or two billion.

Anything else that does not find a buyer should be put into run-off, suggests the ex-Aviva insider.

He says: “Just run it off. You wouldn’t have so much of a problem on solvency if it was done gradually over time.

“Aviva could probably even operate with a lower solvency for a while.

”There would be good capital returns from the run off. Aviva is well-equipped to do it and wouldn’t need a specialist to help.

”There would also be a big cost saving. There are thousands of staff managing that piece of the business, based on accepting new business.

”Separating the IT life and protection from general insurance wouldn’t be that hard. A Tata or IBM could do it, probably for less than a few hundred million.”

Smaller but more beautiful

Unshackled and free at last from its sclerotic UK protection and savings arm, Aviva would be left with the general insurance arm, Aviva Investors and European & Asian Life.

All of those business would be up for sale.

If there are no buyers, they could be hived off into separate floated companies - one the solid performing general insurance business and the other European/Asian life & Aviva Investors - with a promise to investors of a high yield dividend and moderate capital gains on share price.

Amanda Blanc’s arrival as CEO has bounced the share price

Amanda Blanc’s arrival as CEO has bounced the share price

Blanc is hinting that radical action could be on the way, and the market likes what they hear so far. The share price is up 5% since Blanc’s appointment.

“For investors I will address the under performance of recent years and set a strategic path that is ambitious,” Blanc said upon appointment. “I am not a business as usual person and I haven’t come here to do a business as usual job.”

Shareholders have seen so many false dawns, they have their doubts.

Meadowcroft said: “I would definitely break it up.

“But I’m just not sure it’s in the genes of the people leading it to do so. We’ll see.”

No comments yet