The insurer also saw underlying profits fall by a third as it announced its latest set of results and coronavirus continues to create uncertainty for the group

It has been a tough year for the Saga Group, with overall profits down by more than a third to £109.9m as market conditions hit hard.

The Saga Group reported a 39% reduction in overall profits to £109.9m for the year ended 31 January 2020, with the group’s broking and underwriting businesses likewise suffering.

The decline in the performance of the group’s insurance business has been driven by a number of factors, including the PRA’s (Prudential Regulation Authority) crackdown on renewal pricing, of which the insurer was a particularly hard hit business.

In response to the crackdown, Saga launched a new three year fixed-price product, and in its annual report the insurer revealed it had sold 320,000 such policies, with 65% of direct new business clients choosing the product.

Despite the relative popularity of this new product, the insurer’s profits from retail broking business fell 14.7% to £90.2m (2019: £105.8m). The group’s underwriting underlying profit before tax fared even worse, dropping by more than a half to £40.6m (2019: £86.7m).

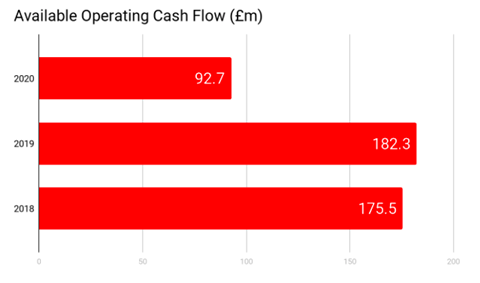

As a group, Saga’s financial position has also weakened, with available operating cash flow down by almost a half to £92.7m (2019: £182.3m).

But group chief executive Euan Sutherland said that it had made “good progress” in improving its position as it looked to improve its fortunes.

“In a year of change, Saga has made significant operational progress and strengthened the management team to ensure the business is positioned to deliver for our customers and members and for investors,” he said. “Our insurance and cruise businesses made good progress against the priorities we set out in April and we have moved to significantly strengthen our financial position, reducing debt and operating expenses and improving cash flow.

“Saga Insurance remains largely unaffected by Covid-19, however along with all other travel businesses, our travel business has been significantly impacted.”

Ratings Downgrade

Despite Sutherland’s optimism, the group received a ratings downgrade from Moody’s in March 2020, with the ratings agency saying the temporary suspension of Saga’s cruise operations, along with lower tour and cruise bookings and rising cancellations related to the coronavirus, will place pressure on the group’s profitability and liquidity”.

The group’s corporate family and backed senior unsecured debt ratings fell to Ba2 from Ba1, and the probability of default rating to Ba2-PD from Ba1-PD. Meanwhile, the outlook on Saga Plc was also changed to ratings under review from negative.

“The rating has been placed on review for further downgrade to reflect the risk of a more prolonged suspension and disruption of the group’s cruise and tour operations, which would put the group at risk of breaching covenants on its bank term loan and revolving credit facility,” Moody’s added.

The ratings agency’s report said that the worsening performance of the wider group would “impede the group’s ability to offset declining profitability on its insurance business or to reduce its debt to EBITDA leverage”.

Moody’s first changed its outlook for Saga to negative in April 2019 after it raised concerns about the risks associated with Saga’s strategy for growing its insurance broking and travel business to offset falling revenues, meaning that the group’s leverage positioned remained above Moody’s expectations.

The group’s debt position includes covenants on its term loan and revolving credit facilities that require it to maintain debt to EBITDA leverage below 3.5x, with its debt ratio currently standing at 2.4x EBITDA (2019: 1.7x).

While Moody’s says it does not expect the terms of these loans to be broken, the report stated that “significant uncertainty” remained as a result of the coronavirus pandemic, and the impact this could have on the group’s travel operations, as well as the impact ongoing government restrictions could have on the elderly population that makes up Saga’s customer base.

Sutherland recognised the group’s problems, and said that it had become “inefficient”, but that the business was now making the “necessary” changes to be more successful in the future.

“Saga is a strong brand, with loyal customers and where we offer really differentiated products, underpinned by excellent service, our businesses do well and have potential to do better,” he said. “Organisationally, the group had become inefficient, lost its tight focus on customers and had under invested in digital, data and brand. We have started the work to make the changes necessary for us to be able to deliver the truly differentiated products and services our customers expect from us.

“Against the backdrop of Covid-19, the outlook is uncertain, but we remain confident that the Saga brand, and our insurance and travel businesses have a successful future ahead.”

Read more…Profits exposed: Admiral, Direct Line Group and esure rely on reserve release for underwriting profit

Not subscribed? Become a subscriber and access our premium content

No comments yet