The Supreme Court ruling scrapping employment tribunal fees could mean a flood of new claims. But it is a double-edged sword for legal expenses insurers.

The Supreme Court’s ruling this July that the government was acting unlawfully when introducing employment tribunal fees in July 2013 represents something of a double edged sword for legal expenses insurers.

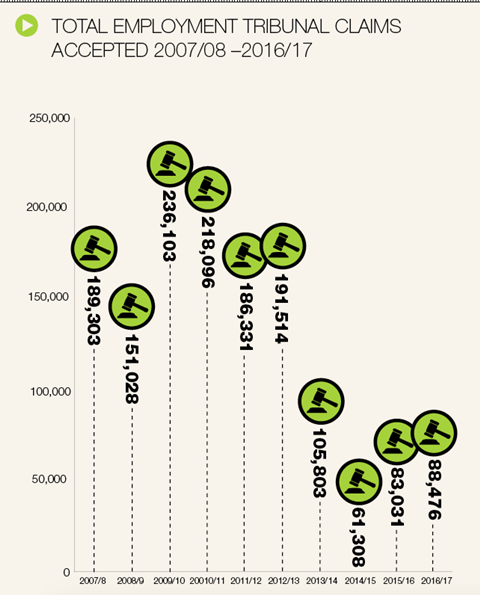

The immediate scrapping of the fees, which used to cost up to £1,200, will undoubtedly produce an increase in tribunal claims – which fell by some 70% when the fees were originally introduced.

This could create pressure for premium rises for certain types of legal expenses policies as a result of increased claims volumes.

The publicity surrounding the changes and the greater resulting policy usage should, on the other hand, boost demand for cover by creating greater awareness of the need for it.

Richard Brooks, sales director at Abbey Legal Protection, greeted the announcement with mixed feelings.

He says “It’s entirely appropriate that people have affordable access to justice but you tread a fine line as the system has the potential to be clogged up again with spurious claims.”

The impact on tribunal claims

One significant unknown factor concerns the possibility that the government could seek to introduce a lower level of tribunal fee.

David Haynes, head of underwriting and marketing at ARAG, says “The jury is still out on this but, if the government introduces no further fee, I see no reason why tribunal claims shouldn’t go back to pre-2013 levels.”

However, Helen Withers, managing director of Arc Legal Assistance, is only expecting a 20% to 30% increase in tribunal claims over the next 12 to 24 months, citing several important changes during recent years.

In 2012 the qualifying period for employees to claim unfair dismissal increased from one to two years, and since 2013 employees wishing to go to tribunal have first had to try the Early Conciliation service offered by ACAS (Advisory, Conciliation and Arbitration Service).

Withers says “The fact that tribunal claims facilities have been scaled down to reflect the decline in claims will also increase the emphasis on avoiding tribunal hearings. Part of this scaling down is the need to give more advanced notice of the dates of tribunal hearings, which provides more chance to use conciliation.”

Impact on legal expenses insurance

Whatever the increase in tribunal usage, it will impact on different types of legal expenses policies in different ways.

The price of individual cover, which is sold to consumers as add-ons to household and motor policies, is unlikely to rise.

This is because these add-ons had normally covered the cost of tribunal fees incurred by employees. So, as the fees are no longer payable, their claims costs should fall.

However, this decrease may not be sufficient to actually trigger premium reductions. Although insurers paid the tribunal fees up front they recovered them if they were successful.

But the implications are far greater for commercial legal expenses insurance, which is sold both on a standalone basis and as an add-on to – or as a core part of – a broader insurance package.

Because commercial policies protect the employer rather than the employee, their pricing is vulnerable to a future increase in tribunal claims and also to an issue relating to previous claims.

Matt Frost, group director of underwriting, claims and reinsurance at DAS, says “The Supreme Court has ordered in the region of £32m in fees paid since 2013 to be reimbursed. Some fees will have been paid by the employers as part of the compensation award whilst other cases will have been funded by legal expenses insurance.”

Commercial legal expenses insurers commonly maintain they are not expecting much in the way of immediate premium increases, largely because premiums didn’t actually reduce much during the era of tribunal fees.

This is because, despite the volume decreases, average claims costs increased as a result of those with the highest paid jobs finding it easiest to meet the cost of the fees.

However, whilst not predicting anything catastrophic, some insurers acknowledge that premiums on commercial policies may have to increase eventually.

Phil Ruse, head of legal protection sales and distribution at Allianz Legal Protection, says “I don’t see any increases in premiums at the moment because sales volume increases will offset costs. But I expect commercial policies to go up by 20% to 30% eventually.”

In perspective

Nevertheless, the impact of the scrapping of the tribunal fees is only one factor influencing the potential pricing of legal expenses insurance.

The state of the economy is arguably just as important because claims tend to increase when jobs are scarcer. Indeed, Phil Ruse says “I think the impact of a recession could be greater than that of the scrapping of the fees.”

Improved education to dispel the commonly held perception amongst brokers that legal expenses insurers decline too many claims could also more than offset any detrimental impact from the tribunal fees issue.

A particular bugbear with brokers is that many claims get declined as a result of employers not making sufficiently prompt contact with insurers.

Jon Newall, principal at Lockyers, says “For tribunal cover to be effective under a standard legal expenses policy you have to have consulted with the insurer during the redundancy or dismissal. But it’s very rare that clients’ actually do this, and they only contact us once they receive the ET1 form from the tribunal service.

“However, if a client purchases D&O cover there is no such onus on them. So as brokers we prefer to recommend that option to clients as it means less claims are turned down.”

But Robert Marshall, chief executive of Trident Insurance, feels progress could be made if legal expenses insurers used more comprehensible language to make their requirements clearer and encouraged employers to keep better records.

He says “Legal expenses only doesn’t pay out because employers are not managing in a fit and reasonable manner. Poor record keeping can result in claims being declined because If it’s not written down then to the court it effectively didn’t happen.

“Employers should be monitoring potential disputes rather than just running to the insurer when it all blows up.”

No comments yet