As it releases its interim report on home and motor insurance, the regulator proposes further remedies to stamp out the loyalty penalty, including restricting prices on automatic renewals and measures to better enable switching cover

The FCA has released its interim report of its market study into the pricing of home and motor insurance, which estimates around six million policyholders are not getting a good deal.

“This market is not working well for all consumers,” said FCA executive director of strategy and competition Christopher Woolard.

The regulator introduced measures two years ago to improve renewal transparency. Under the FCA rules, introduced in April 2017, insurers were compelled to “clearly, accurately and prominently” display their proposed renewal premium alongside the premium paid the year before.

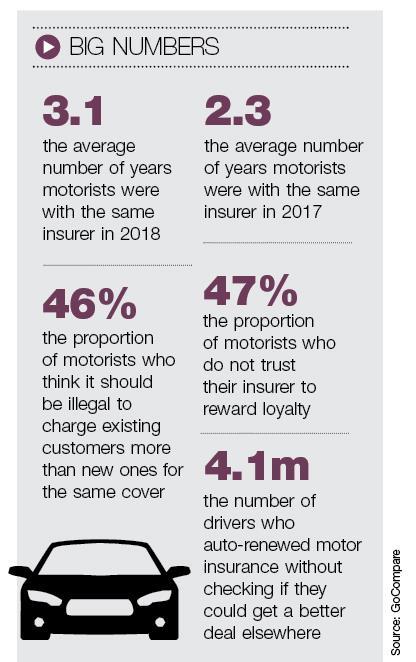

However, research by GoCompare suggests the measures have not gone far enough to tackle dual pricing. It found that 4.1 million drivers auto-renewed their car insurance this year without checking if they could get a better deal by shopping around. Nearly half (47%) of those surveyed said they did not trust their insurer to reward their loyalty.

“It’s no secret that insurers entice new customers with cheaper introductory offers at the expense of their existing policyholders,” said Lee Griffin, chief executive and founder of GoCompare Car Insurance. “When it comes to car insurance, loyalty can cost you hundreds of pounds.”

In 2018, Biba and the ABI agreed joint guiding principles and action points on pricing to reduce excessive premium differences between existing and new customers. The principles commit to introducing procedures to combat dual pricing when determining renewal premiums and to make clear to new customers that any special premium only applies for that year and that subsequent premiums may be higher.

“The industry takes this very seriously and the ethos and approach to better outcomes for long-standing customers will be given board or senior management level priority and be formally incorporated into firms’ procedures for determining the premium at renewal,” said Graeme Trudgill, Biba executive director. “We are mindful of the issues raised by the FCA in this issue and we are keen to ensure good outcomes for customers at renewal through these principles.”

The FCA has announced a consultation on a series of proposals designed to restrict price rises at renewal and increase switching rates. They include remedies to:

- Tackle high premiums for consumers: This could include banning or restricting practices like raising prices for consumers who renew year on year, or requiring firms to automatically move consumers to cheaper equivalent deals.

- Stop practices that could discourage switching: Including restricting the way that firms use automatic renewal.

- Make firms be transparent in their dealings with consumers: Including improvements to the way they communicate with their customers. The FCA is also considering whether firms should publish information about price differentials between their customers.

- Harness benefits of innovation in the longer-term: Ensuring general insurance markets benefit from new technology, including open finance.

No comments yet