The Lloyd’s market has had a tough few years with large catastrophe claims and dwindling reserve releases, but how have market conditions affected the main players, and what does the future hold?

With three successive years in the red and a fourth year of underwriting losses seemingly on the way, the Lloyd’s market has faced some testing times of late.

The combined operating ratio (COR) for the Lloyd’s market stood at a loss-making 102.1% in 2019, but this was still an improvement on the 104.5% reported for 2018 and the 114.0% for 2017.

Despite this improvement, Lloyd’s has paid out more than £11.5bn over the last four years, much higher than the £9.6bn paid out over the previous high catastrophe frequency period of 2010-2012 and even further above the £6.4bn incurred between 2004 and 2005.

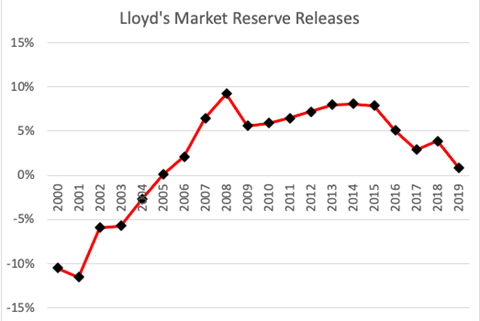

Jefferies’ research also found that the market had suffered from a period of “industry-wide reserve strengthening” between 2000 and 2004, but that reserve developments since this period had been “favourable”as the industry began to release funds from previous years.

Since 2014, however, the amount being released from reserves has been on the decline, and the market released just 0.9% from reserves in 2019, and Jefferies said in its research that the Lloyd’s Market had demonstrated “remarkable underwriting discipline” in response to these challenges

.“Reassuringly, the Lloyd’s market is demonstrating remarkable underwriting discipline, raising prices and cutting volume,” Jefferies said. “Moreover, the number of new syndicates being approved to write in Lloyd’s has fallen to near zero, preventing an influx of new capital from over-supplying the market.

“We expect all of these trends to accelerate in 2020, with rates rising ever faster, volumes falling and potentially some syndicates completely withdrawing.”

The investment bank added that capital strength would be key to taking advantage of these opportunities as we moved through the rest of 2020.

“Looking beyond the listed insurers, we believe that capital strength is critical to success,” Jefferies said. “With catastrophe losses high, reserve releases low and claims inflation rising fast, we expect that some syndicates will find themselves capital constrained and unable to take advantage of rising prices.

“During this time, we believe that the listed insurers will outperform, as they typically have strong balance sheets, or are backed by shareholders willing to support equity raises.”

But how have the individual underwriting agencies fared?

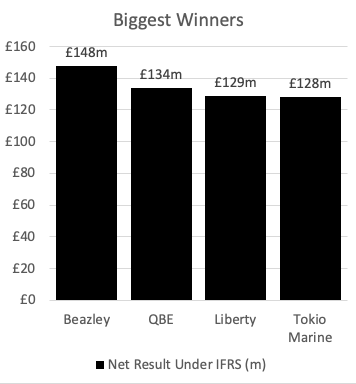

Last year’s top underwriter Hiscox has been replaced by Beazley, with the underwriter reporting net profits of £148m for 2019 off of gross written premium (GWP) of £2.5bn.

This means that Beazley accounted for 21.4% of the Lloyd’s market’s profits, despite writing just 6.6% of the market’s overall GWP.

Other top performing underwriters in the market include QBE with profits of £134m, Liberty (£129m) and Tokio Marine (£128m).

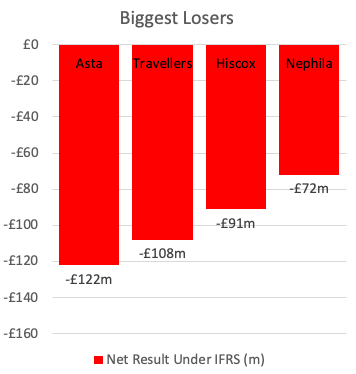

At the other end of the scale, Asta reported the biggest losses of 2019, reporting a net loss of £122m under IFRS reporting standards off of GWP totalling more than £1.2bn, closely followed by Travellers with losses of £108m off of GWP of £370m.

Meanwhile Hiscox, which brought in the Lloyd’s market’s biggest profits in 2018, reported a net loss of £91m for 2019 off of GWP of just under £2bn.

Jefferies said in its research that Hiscox’s downturn in performance was largely for similar reasons as its November-issued profit-warning, namely social inflation driven by US juries deciding on ever increasing payouts against companies liable for casualty claims.

The wider Hiscox brand has also taken a bit of a battering in recent months, especially in the wake of the business interruption scandal that has hit as a result of the Covid-19 crisis.

Despite these challenges, Jefferies said that given the actions taken by Hiscox in the fourth quarter of 2019 (which included strengthening its director and officer’s liability reserves, changing reserving methodology to hold casualty reserves longer, and recording new casualty claims at higher loss picks) as well as the insurer’s “long-term track record” , it expected “Hiscox’s London Market’s business to improve its position in 2020”.

No comments yet