Gallagher’s acquisition of Bollington is in its ’sweet spot’ range, so what does it mean for the market?

Briefing by Saxon East

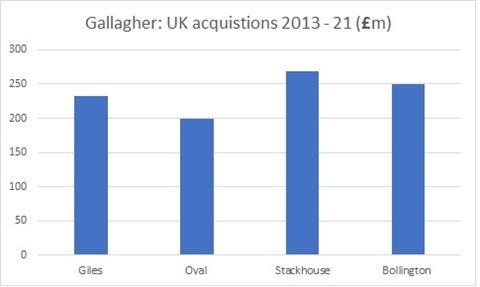

Another year starts, another deal for Gallagher. This time it is Manchester-headquartered Bollington, with a deal estimated in the £250m range.

This time two years ago it was Stackhouse Poland, going for £268m.

This deal range of £200m to £250m is the sweet spot for Gallagher, by looking at previous acquisitions (see below: Bollington estimated)

But Gallagher certainly has the firepower to go way beyond these purchase prices.

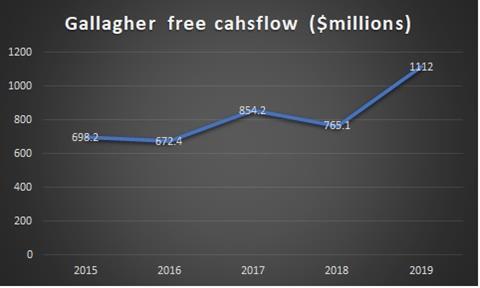

It mainly uses free cashflow in the UK to fund purchases - which is growing at a healthy rate (see below)

If you are a UK private equity-backed broker, that is good news. There is a potential purchaser with the potential to significantly increase the size of acquisitions.

The US broker is looking for qualities such as specialisms or good product fit, regional footprint expansion and the right cultural fit.

The biggest competition threat for those £200m to £300m is from Aon and Marsh. But Aon has spent considerable resources consuming Willis, and it is only two years since Marsh absorbed top five broker JLT.

That means Gallagher is in good shape to continue buying UK independent brokers for anywhere between £200m to £300m, and much higher if it desires.

Not a subscriber? Click here to join.

Bollington buy will ‘supercharge’ Gallagher regional footprint

No comments yet