This is touted as the most important chief executive appointment in Aviva’s history. But why?

By content director Saxon East

There is a story doing the rounds in the City and it goes something like this.

Chairman Adrian Montague had two clear candidates in mind for the chief executive role: UK boss Andy Briggs and international chief Maurice Tulloch.

Both were dependable Aviva men who knew the company well and were capable of filling the void left by Mark Wilson’s departure.

But Montague soon got wind of what shareholders wanted: a wider search for a CEO, including an outsider who could shake things up.

The speculation is that Montague is taking so long to make an appointment because it has fully dawned on him that this is the most important chief executive appointment in Aviva’s history. Why?

The unhappy shareholders

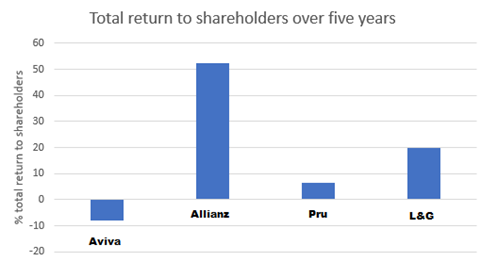

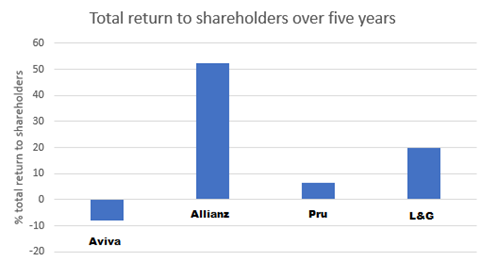

Perhaps the most obvious illustration of Aviva’s troubles can be found in the graph below. This is the total return to shareholders over the last five years, including gains from the share price and dividend.

The world has been on one of its longest stock market bull runs in history, yet Aviva has produced a -8% return to shareholders. Now compare that to Allianz, where investors have enjoyed more than 50% returns.

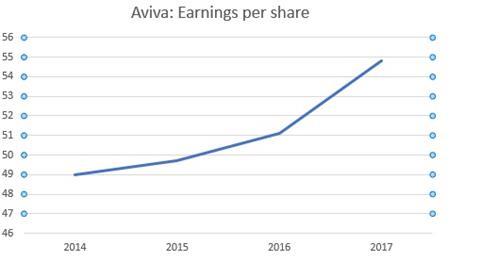

Former chief executive Mark Wilson always felt, arguably with some justification, that the market never rewarded his work. Certainly when you look at the growth in earnings per share, below, Aviva showed improvement under his management. This was matched by an increasing dividend payment.

One can speculate forever on why the share price remained in the doldrums: Friends LIfe being seen as a rights issue in disguise; Aviva being in the dowdy European market compared to competitors such as Pru that had roared in Asia; dormant shareholders who put Aviva in tracker funds or reinvested the dividend with little care to sell their stock and uneager buyers watching a stagnant share price; competitors having better income and capital gain returns; the shadow of Brexit.

Ultimately, what matters is that Wilson never moved the dial. Wilson even tried to juice shareholders with share buybacks. None of it worked.

Many investors and analysts now have a similar view: more of the same isn’t good enough.

The new chief executive appointment

This means the pressure will be on the new chief executive to do something more radical. One option that has wide consensus across the City is that Aviva should sell its life back book. It’s a legacy business, that is capital intensive, and is fighting an outflow of business on the non-platform.

However, the question of what to do with all the extra capital and long-term impact on the dividend would be difficult to work through.

Other more radical options involve splitting the business up completely, like Bruce Hemphill did at Old Mutual, so the better performing parts can unshackle themselves from the legacy businesses.

The non-life business is rock solid, not least in the UK where a succession of management teams have done an excellent job in producing underwriting profits in a very competitive market.

Will a Briggs or Tulloch have what it takes to make such changes? Or is an outsider needed? Or do we really need any change at all? These are the questions Montague will be tussling with. Uneasy lies the head that wears a crown.

Whoever lands the role, will face a great challenge in appeasing shareholders eager for more value. The pressure for change will be immense.

One thing’s for sure: there is plenty more drama to come.

No comments yet