With a broad SME market and new small businesses springing up all over the UK, how do brokers keep abreast of trends and make sure they are offering their customers the best possible value?

With new small to medium sized enterprise (SMEs) such as micro-breweries, boutique distilleries, horticultural nurseries and artisan bakers popping up every day, insurance needs to be able to cater to ever-evolving risks.

This is where schemes come in. With so many growth opportunities in untapped niche or specialist areas of business, schemes can be gold dust to brokers, giving them a unique selling point to address the market.

Ecclesiastical’ s schemes development underwriter Will Browne told Insurance Times: “The schemes market is tailor-made to serve the SME sector. Generic SME products are not designed for particular trade or customer groups and this is where schemes offerings can provide real differential.

“A scheme should provide unique covers that tailor the offering for the particular needs of a customer group, and this is the philosophy we adopt at Ecclesiastical.”

In its 2019 UK SME Insurance Survey, GlobalData said the penetration rate for SMEs in insurance for public liability (PL) and professional indemnity had decreased by 1.3% in 2019, falling from 70.8% to 69.5% (see p39).

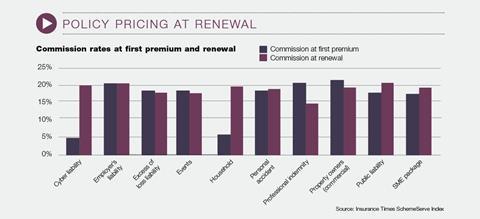

However, the inaugural Insurance Times SchemeServe Index – part of an ongoing study by SchemeServe in partnership with Insurance Times – revealed last year that public liability cover offers brokers the highest commission percentage at policy renewal – it offered a commission rate of 22.3%, up from a rate of 16.9% when a customer first takes out a policy. Meanwhile, excess of loss liability (EOLL) insurance is seeing commission growth of more than 240% at renewal. With certain lines worse than others, it also revealed that the least profitable lines for brokers were caravan and household.

SchemeServe chief operations officer and director John Price said: “Our Index, published last year for the first time, revealed that excess of loss liability, employers’ liability and PL are the most profitable schemes for brokers, showing some dramatic rises in premiums and commissions.”

But with so many new areas of business and changing customer needs, how can brokers and insurers keep up?

Know the customer

RSA delegated business partnerships director John Dawe told Insurance Times: “Differentiation for brokers is more important than ever. It means finding ways to meet customer needs that are not just focused on price. That’s why schemes are a fantastic solution for brokers – there’s essentially a three-way relationship between a customer, broker and insurer.”

Dawe said that brokers who understands their customer and their insurance needs are those who are going to gain a competitive edge.

He said: “It gives them the opportunity to provide solutions to these customers, and put their brands on the policy while also staying in control of service. It’s those brokers who win and that’s because they’ve got a stable proposition. There’s a clear segment of customers – they’re affinity groups or trade, and they have both got a common set of needs.”

But Dawe warned “schemes are not a quick win,” giving the example of having solo musicians as a target customer and covering performance cancellation.

“It’s really important for the broker to have a clear vision of the business that they want to write and full knowledge of their target customers and what makes them tick,” he said.

Bearing this in mind, he said it was important for brokers to keep on top of changing trends such as the gig economy, which in turn create a new insurance need and a solution. Brokers can do this by looking at the types of risks they have across their portfolios and identifying themes, Dawe added.

Price said that advances in technology, particularly from more affordable cloud based software sales and distribution services, have opened up the market to more brokers. About one-third of schemes business is done online.

Shape of the market

Meanwhile, Browne said that over the last five years Ecclesiastical has seen more brokers become interested in schemes.

He said: “Approximately a third of the enquiries we see are for speculative schemes, where a broker is coming to us with an idea they would like to develop. In terms of the existing schemes market, we are seeing a lot of movement of schemes around the market.”

Browne said this can be for various reasons – performance issues that are challenging to solve may indicate a scheme is under-priced, whereas others are being remarketed “where the broker feels the proposition is losing its edge and not getting the support from the existing carrier”.

But Browne said that specialist sectors and niche markets cannot be put into boxes and therefore the broker does not restrict itself to any one type of trade in the industry.

“Broadly, we look for markets that demonstrate they are different from the typical SME-type model that might fit into a traditional commercial combined policy,” he said. “We look for ways to stand out in the market and offer something that you can’t typically get in a standard commercial wording. It also needs to be relevant to the sector you’re working with to show how you’re adding specific value to that customer.”

He said that for a scheme to grow there needs to be a large enough customer base and understanding about how that group is served. When asked how it operates, Browne said: “It’s an open door for brokers to talk to us about any and all ideas – we like to grow long-term, sustainable relationships with our broking partners and the best way to do that is to collaborate with them and help them develop acorns into oak trees.”

Out of hours

Jodi Cartwright, managing director of MGA startup Coverly, says one obstacle to insurance purchases is that SME customers often do their business outside of traditional business hours. In other words, SME insurance purchasing habits do not suit the traditional 9-5 working hours of some brokers.

Coverly is providing a solution to this issue by using webchat and allowing customers to transact online. Cartwright said it is on track to become a “virtual insurer” that runs 24 hours and seven days a week.

She likened the issue to what happened in personal lines insurance, saying that, due to low premiums, the distribution cost needs to be cut out of the chain.

Lifeblood of the UK

Zurich’s SME Risk Index looks at changing risk. The insurer also identifies trends in the market. Paul Tombs, Zurich’s head of SMR said dentistry, security, and media were sectors where customer needs are distinct and therefore would ne classified as niche.

He told Insurance Times: “Certainly from the contracting market and the small IT contractors, those are the areas where we see growth. That creates a market that needs to have the right products offered to them.”

For 2020 post-Brexit, Tombs said there is potential for new opportunities: “SMEs are the lifeblood of the UK. There is still some uncertainty as to what the economic and political landscape will be, but its an opportunity to grow.

No comments yet