New research from Consumer Intelligence, published exclusively by Insurance Times, reveals how vulnerable customers are being affected by the pandemic, as well as why this represents an opportunity for brokers and insurers to boost their brand’s reputation and their underlying business performance by offering better credit options for paying by instalments

The coronavirus pandemic has hit many people hard, and this is leading to a rise in vulnerable customers across the UK as well as an increase in demand for credit when taking out motor insurance.

New research from Consumer Intelligence, published exclusively by Insurance Times, has found that around 16% of UK consumers identify as vulnerable, although the research notes the true figure is likely to be much higher.

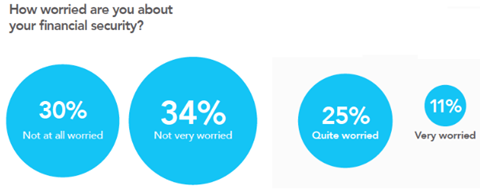

In its research report The True Cost of Credit in the Motor Market, Consumer Intelligence found that twelve weeks after lockdown began, some 25% of people said they were quite worried about their finances, and 11% were very worried.

Here, the Covid-19 pandemic is undoubtedly having an impact, especially because of how lockdown restrictions and social distancing measures have affected businesses and their working practices.

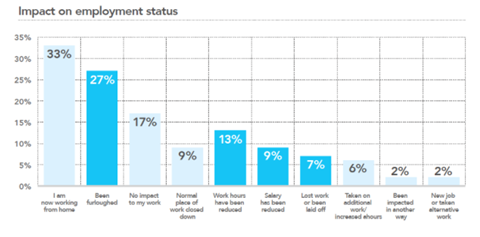

Results from Consumer Intelligence’s Covid-19 tracker showed that at the end of May some 27% of people were on furlough, 13% had had their hours cut, and 7% had lost their jobs.

Younger people were the most likely to have been put on furlough, with more than 30% of 18 to 34 year olds on the scheme.

And Consumer Intelligence chief executive Ian Hughes says this is going to be an ongoing issue for the UK motor insurance market to grapple with for some time.

“Credit is going to become a big issue for motor insurers in 2020, and beyond,” he says.“In a volatile market and against a backdrop of recession, more people are going to need to spread out the cost of large insurance premiums.

“That means all insurers and brokers need to be asking themselves some hard credit questions.”

And those questions, Hughes says, need to explore which consumers are looking for credit, how insurers and brokers are offering credit to them, and how much is being charged to pay for a policy in monthly instalments.

Another big question for the market, Hughes says, is around vulnerability, and how offering credit affects those vulnerable customers insurers and brokers are trying to help.

“This is your chance to make sure your credit strategy is credible for the next stage of the living-with-Covid world,” he says. “It’s also your chance to make sure it does your business credit, too.

“The first step is to understand your credit proposition, how it fits into your pricing strategy, and where you sit in the market.”

To help the market understand these issues, Consumer Intelligence is hosting a webinar on instalment income on Friday 11 September, and Insurance Times readers can register for a free log-in to the session here.

Incredible Opportunity

While rising customer vulnerability presents a number of challenges for the insurance market, it also presents opportunities for brokers and insurers alike.

Premium finance and instalment income is a big market.

Hastings’ annual report revealed £105.6m of income from premium finance interest in 2019, while in the same period it wrote premiums totalling £961.6m and recorded a £109.7m operating profit.

Meanwhile, Admiral’s instalment income from motor insurance was £83.9m in 2019, up from £81.4m in 2018 and £56.1m in 2017.

And Direct Line Group revealed £83.8m in instalment income in its latest results. In the same period it wrote £1.6bn of GWP, and recorded a £302m operating profit.

The latest research from Consumer Intelligence has also shone a light on just how important instalment income is for the UK motor market, with premium finance income accounting for 16% of motor brokers’ total income according to an October 2019 report from the FCA.

The research also found that almost a third (32%) of drivers currently pay their insurance premium in instalments, but that figure could soon be on the rise as the impact of the Covid-19 pandemic continues to be felt.

This means that those brokers and insurers that truly understand their credit proposition, and offer the right options to their customers at the right time, could set themselves up not only for financial success by way of a boost in revenue, but also for a boost in reputation and loyalty by helping those vulnerable customers on their books to better access motor insurance provisions.

“The credit picture has always been complicated, and it’s clearly now more complicated than ever,” Hughes says. “There are real advantages for the organisations that can vary credit. The organisations that can begin to vary credit won’t just be able to demonstrate that they have treated customers individually and fairly, they will also be able to more effectively target the customers and risks they want to attract.

“One of the things brands can win with a sophisticated cost of credit will be the right to market to the customers it really wants. And for those brands that can get close to their customers and understand their needs and pressure points, there’s a further opportunity to develop new insurance and credit products to fulfil predicted demand.”

The insurance landscape is evolving. Click here to have your say and you could win £250 John Lewis vouchers. Brokers how well have your insurance partners supported you over the last 12 months?

Read more…Online fraud and cyber scams soar during the pandemic lockdown but insurance for it ’fairly new’

Not subscribed? Become a subscriber and access our premium content

No comments yet