Price cuts by some insurers means the motor rate rise has slowed ahead of the revision of the Ogden rate

Overall motor premiums continue to rise, but some insurers have already been cutting their premiums ahead of a promised revision to the Ogden discount rate.

Last week the government announced proposed new legislation that will increase the Ogden rate, and introduce three-yearly revisions based on a new investment benchmark.

Back in February, the government cut the rate, at which insurance compensation payouts for long-term bodily injuries are calculated, from plus 2.5% to minus 0.75%. Many insurers raised motor premiums as a result. Last week, the government said the new rate will be between 0% and 1%.

But even before last week’s announcement, some insurers had begun reversing their earlier rate increases.

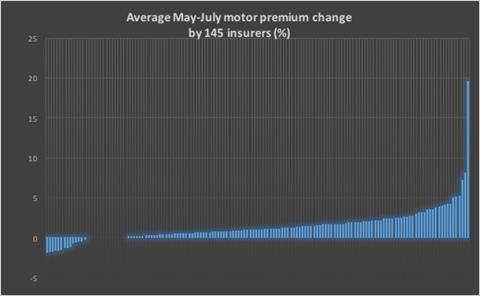

Data from Consumer Intelligence shows that 14 insurers cut their premiums over the three months to the end of July.

The latest data from Consumer Intelligence, published exclusively by Insurance Times, reveals that average motor premiums rose by 1.35% in July. But the data show that price cuts by a cohort of insurers have slowed the acceleration in prices from the month-on-month rate of 3.5% seen in the two months immediately after February’s change in the discount rate, when only three insurers reduced their rates.

Consumer Intelligence product manager John Blevins says the path of the market has not been straightforward.

| Price Index | Overall | Direct | Price comparison websites |

|---|---|---|---|

| July 2016 | 100.00% | 100.00% | 100.00% |

| Aug 2016 | 101.50% | 101.40% | 101.60% |

| Sept 2016 | 103.00% | 104.10% | 102.70% |

| Oct 2016 | 104.70% | 106.80% | 104.10% |

| Nov 2016 | 105.70% | 108.90% | 104.80% |

| Dec 2016 | 106.30% | 108.90% | 105.60% |

| Jan 2017 | 106.00% | 108.70% | 105.40% |

| Feb 2017 | 107.20% | 112.80% | 105.80% |

| Mar 2017 | 110.80% | 116.50% | 109.40% |

| Apr 2017 | 113.50% | 118.90% | 112.10% |

| May 2017 | 114.70% | 119.70% | 113.40% |

| Jun 2017 | 116.60% | 122.00% | 115.30% |

| Jul 2017 | 117.10% | 122.50% | 115.80% |

“The difference in the premium changes we are seeing is down to who has had what already set-up in their claims reserves,” he says. “If you were a provider with some excess reserves, you probably weren’t worried about making a knee jerk reaction, but a smaller insurer with claims performing as expected would need to have made more of a reaction to anticipate the effects of the discount rate change.”

There has been polarisation in the market in terms of rate movements, with the latest data revealing price changes of between a cut of 1.86% and an increase of 19.49%. This has been driven partly by the different market niches targeted by different motor insurers, with young driver policies, for example, not being impacted as much by the rate change.

“Younger driver market premiums are already sky high, so if you are already paying a lot and then you add 20% on top [to allow for the discount rate change], then you are just making it too expensive and you won’t be able to remain competitive,” Blevins says.

“Some of the smaller brands have also been a bit more opportunistic, either holding or reducing rates to get a bit more business through the door and hoping they don’t have a large bodily injury claim,” he adds.

And with the latest in the ongoing Ogden saga revealing government plans for a positive and regularly reviewed discount rate, insurers will be watching closely to see how their pricing models will be affected going forward.

But the government has said that any change in the law, which is still in the proposal stages, will not apply retrospectively.

Blevins says we could see further cuts to motor premiums in the future if the proposed changes come into force.

“We have already started to see people taking some of their increases back out,” he says, “but an increase in the discount rate could result in a whole batch of insurers who are not as competitive on price as they have been, but without increased claims, and that could result in them reducing premiums again [to help win back lost market share].”

EY UK general insurance leader Tony Sault said such changes could even result in large reserve releases as a result of the reduction in claims costs for bodily injury claims.

“A revision to 0% could reduce these costs by one-third, meaning reserve releases of £1.2bn, while a change to 1% could reduce this by two thirds, meaning up to £2.5bn could be saved by insurers and reinsurers compared to their current booked position,” he said.

No comments yet