The insurance industry is coming under increasing pressure over dual-pricing. Will it ever be able to eliminate it?

It has been described as the “crack cocaine” of the insurance industry by Consumer Intelligence chief executive Ian Hughes. Insurers, he says, are finding it almost impossible to wean themselves off the practice of dual pricing.

His comments came after the FCA announced it would be investigating the practice, which also coincided with a super-complaint by Citizens Advice to the Competition and Market Authority.

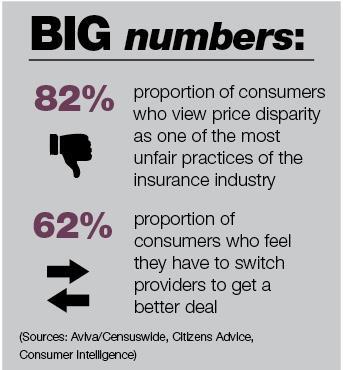

The industry practice of offering new customers lower premiums than renewal customers has received growing criticism in recent years. While it may have once worked as a way of attracting new customers in the era before aggregators when churn rates were lower, in today’s price-driven market it has resulted in loyal customers being unfairly penalised, according to Citizens Advice.

Loyalty penalty

It found that vulnerable groups – those on low incomes, older people and people with health problems and lower levels of education – were likely to struggle with shopping around for a better deal. Because they tend to have poorer digital skills, they are less likely to benefit from online tools and more likely to suffer a ‘loyalty penalty’, whereby they are charged more for staying with the same provider.

“If you look at other industries, such as the energy market, only 20% of consumers shop around and very few people switch. That is what insurance looked like 15 years ago,” says Hughes. “Price comparison has enabled people to shop around and switch easily, and there’s nothing wrong with that, from a customer’s perspective. But the introductory rates, lack of engagement through the life of the policy and price increase at renewal create the hamster wheel which all parties – insurers, brokers and customers – find it almost impossible to get off of.”

But personal lines insurance is not as price-driven as it first appears, Hughes believes. Brand and quality of cover still count, he says.

“Somewhere between 65% and 70% of the reason why consumers choose a particular insurer relates to price, but a substantial part of it is around trust and about brand,” he says. “If it was all about price, then whoever is the cheapest on a price comparison site would always win, and that simply doesn’t happen.”

“There’s also a time value of money element to shopping around. We’ve seen in our research that people only shop around when they see an increase of £30 or more, and switch if there is a difference of around £50 or more.

“So, if the renewal notice comes in and they see a £30 increase in the cost of their insurance or less then they will probably just accept it. Consumers are almost forced into switching when they see huge jumps in their premiums.”

Aviva’s stake in the ground

Following the introduction of rules by the FCA in April 2017, insurance carriers and brokers are now required to display the previous year’s premium on renewal notices. This push for transparency is bearing fruit, with data from Consumer Intelligence’s Insurance Behaviour Tracker showing a rise in the number of motorists (by 1% to 85.1%) and homeowners (by 3% to 77.6%) shopping around at renewal.

“Some brands are slightly ahead of the competition – in particular Aviva – and many brokers are doing a good job helping customers shop around to avoid getting stung by the cost of loyalty,” noted the data analytics firm.

The problem with the drive for renewal transparency is that the focus continues to be on price above service, says John Price, chief operating officer at SchemeServe. “Putting notices on a renewal statement saying ‘you might be able to buy this cheaper elsewhere’ makes it all about price and encourages customers to buy an inferior product,” he says. “It actually goes against treating customers fairly.”

In December 2018, Aviva took a bold step by launching AvivaPlus, a subscription-style service allowing customers to pay monthly and providing a guarantee that existing home and car insurance policyholders would not be charged more than new customers at renewal. The aim of the new product is to “help rebuild consumer trust and confidence” according to the insurer. At the time, Aviva UK chief executive Andy Briggs described AvivaPlus as a “reinvention of insurance”.

Implementing change

However, unlike Aviva, most insurance companies are not yet in a position where they can dispense with dual pricing as it is so ingrained in actuarial pricing models, says Hughes.

“It’s easy enough to say that customers are going to have fair pricing and won’t have big increases at renewal, but actually delivering that is horrifically complicated,” he says.

“A lot of insurers have a very basic issue that some of the systems they are operating on still have green blinking cursors that create the price, and the person who wrote the code retired 20 years ago. So, it’s one thing to say we’d like to do it, but it’s another to be able to actually implement it.”

Source

No comments yet