Commercial lines brokers continue to consolidate, with the tie-up between Stackhouse Poland and Gallagher expected to be completed at the end of Q1. But as brokers seek ever-increasing scale, do we risk losing the value of independent advice?

Commercial lines brokers face numerous challenges in 2019, including the ongoing pressure to differentiate and grow in what is an increasingly challenging and uncertain operating environment.

Achieving organic growth has never been easy, but as 2019 gets underway it is also clear the challenge has never been greater. The impact of economic and political uncertainty is stifling UK business with an anticipated impact on commercial insurance spend.

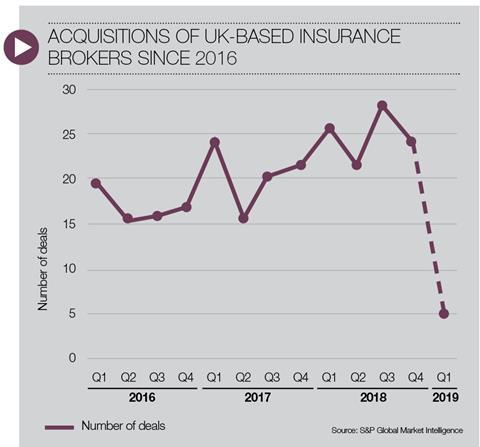

Consolidation continues to be the most direct route to gaining scale and market share. After a relatively quiet December, independent broker Stackhouse Poland became the latest large intermediary to be swallowed up.

It is understood that consolidator Arthur J Gallagher has offered close to £300m (at a value of 15 times Stackhouse’s earnings before interest, tax, depreciation and amortisation (EBITDA) of roughly £20m) for the company, setting the tone for mergers and acquisition (M&A) activity in 2019.

The UK insurance broking sector is worth £14.9 billion, growing at a steady rate of 2.8% a year since 2013.

Olly Laughton-Scott, partner at IMAS Corporate Finance, says: “On one level [the Gallagher/Stackhouse deal] will support continuing M&A activity because the perception will be that if you can build up a significant asset you can sell it on at a premium, so it will encourage other consolidators to move forward.

“But the other interpretation is that the reason Stackhouse sold is that it saw fewer opportunities, and if it had seen fantastic opportunities in terms of stuff to buy, it would still be an independent business.”

He continues: “There’s been such a high level of consolidation. It does mean that the pool of businesses that can be acquired is contracting. But there are still a significant number out there. And what is clear is that the large boys have not been successful at roll-ups, and they have used the medium-sized private equity-backed firms essentially to do it for them. And then they swoop in and buy the larger business.”

The growing compliance burden and changing fee structures makes size an ever-important factor within UK broking. Other benefits associated with a larger organisation include access to investment and a panel of larger insurers. But is this at the expense of independent advice and the spirit of innovation?

Freedom from pressure

“I have nothing against consolidation,” says Ashwin Mistry, executive chairman of Brokerbility and BHIB. “We have bought a number of businesses and brands over the years to grow our books of business and talent.

“But what I don’t have is a venture capitalist that demands that I make a coupon return of anywhere between 9% and 13% every quarter and grow by double digits.

“I’m still allowed the freedom to make decisions. If you feel the pressure to get certain renewals over the line, the nervousness will show in your behaviour and will be picked up by clients.”

He adds: “I think independence of mind is desperately important.”

Staying nimble

There is also the old argument that as brokers get bigger they lose their entrepreneurial spirit and ability to be nimble. Mistry thinks there is still plenty of innovation in the commercial lines space, and points to insurtech advances and products catering to new and emerging risks.

“It’s a great time to be a broker, but you have to be selective in terms of the client you want to be looking after,” he says. “It’s all about customer journey and how brokers can use things like predictive analytics to best serve their customers and interact with them. That’s not forgetting that empathy at the end of the phone remains important, particularly when it comes to handling claims.”

While the gap between the largest and smallest intermediaries is getting wider, Laughton-Scott thinks technology will prove to be a good leveller.

“Everybody uses the internet and so the benefits of being a large company are in many ways diminished,” he says. “I think the regulatory burden has been overstated because good technology will incorporate regulation into it and it becomes part of the process. Actually the regulators have correctly been more focused on the large companies.”

“Good quality small commercial brokers, certainly in general insurance, have looked after their clients because they have a long-term relationship with them,” he adds.

“With technology increasingly taking care of the transactional side of the business, you ought to still be able to add value through the advice element. But it requires cost to be taken out of the system, which you should do on the transactional side.”

No comments yet