As the demand around automated services grows, the insurance industry must ensure that its workforces are equipped to work alongside automation

The Covid-19 pandemic saw technology take centre stage, as social distancing rules forced the removal of more manual processes. This subsequently influenced consumer habits and the appetite for automation.

Automation refers to technologies that are used to reduce the need for human intervention in processes. It aims to increase both speed and reliability versus manual, human-driven systems.

As the demand for automated services and processes continues to grow, insurers and brokers have to adapt to keep pace with consumer expectations, or they risk being left behind by new market players, such as Tesla founder and chief executive Elon Musk, who launched an embedded insurance proposition for Tesla’s EVs in the US in 2019.

A May 2022 report published by service comparison firm ISG Provider Lens confirmed that many insurers are now embracing different technologies to compete in a more digital savvy insurance sector.

In turn, this market movement has opened the door for more job roles around developing and implementing automation, especially as this type of technology is being applied across the entire insurance lifecycle.

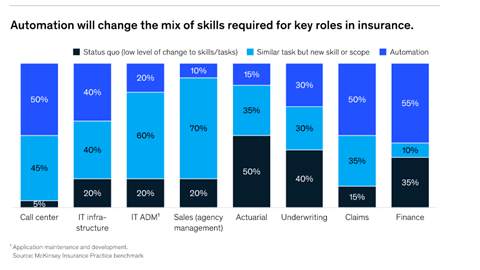

For example, a July 2020 report from global management consultancy McKinsey and Company, titled Transforming the talent model in the insurance industry, found that 10% to 55% of all roles in insurance - from underwriting, acturial, claims, finance and operations - could be automated over the next decade.

It additionally noted that a further 30% of positions could be automated over the next 10 years to reduce routine and low value tasks, in turn changing the skill sets required for various job roles.

This development could place greater emphasis on staff having creativity, agility, critical thinking and social intelligence, for example.

The report added that although the need for automation will increase by 55% by 2030, the need for basic cognitive skills, such as data input and processing, could decline by 15% over the same time frame.

However, because the automation sector is often perceived to be highly specialised, techy and male dominated, the insurance industry is facing a skills gap when it comes to fulfilling automation-centric roles.

Alastair Robertson, the UK head of continuous improvement, automation and predictive analytics at Zurich, who leads the insurer’s in-house automation team, addressed this particular topic in an April 2021 Ted Talk - he sought to bust myths around automation.

He told Insurance Times: “There is a lack of training providers and there’s not a huge bank of people you can choose from.”

To attempt to remedy this situation, Zurich has its own in-house training around automation, which includes six graduate schemes on subjects such as data science, as well as apprenticeships.

“We try to break the mould of where we hire. We shouldn’t limit ourselves - we just need the right people for the job,” he continued.

Robertson also wanted to squash the myth that automation steals people’s jobs. Instead, he believes that it can accomplish simpler tasks quicker, which means companies can deploy staff to work on more complex projects.

“In terms of the technology, it will continue to evolve. You have to be agile or nimble enough to change with it,” he explained.

Robertson is currently applying this thinking to his team of 42 staff - he is looking to create hubs around specific capabilities, such as robotics.

Read: Ki – the digital follow-only syndicate aiming to reduce the London Market’s expense ratio

Read: How bots and automation could offer greater efficiency for claims handlers

Underwriting automation

One offshoot of automation is embedded insurance, where a policy is sold in conjunction with a product purchase. This includes Musk’s motor policies for Tesla owners - but more brands could soon follow suit.

An Insurtech Insights webinar in March 2022, titled Can insurers keep pace with Elon Musk?, suggested that the underwriting capabilities that Tesla needed to insure its EVs were not currently in the market, which is why the firm designed an in-house insurance proposition.

Romain de Maud’huy, chief transformation officer for motor and home at Axa Partners, said: “Tesla wanted to have a whole ecosystem and a great customer journey. It is pushing the market into more precise underwriting. It is also pushing [insurance] to have a more integrated operation.”

Musk’s action has placed a further spotlight on the use of automation within underwriting, which is traditionally viewed as one of the sector’s most complex, expensive and time consuming facets.

However, by using automation in underwriting processes to analyse big data sets, insurers can have more control because they are able to set their own risk limits and pricing, as well as triage more complex risks. Robotic process automation (RPA) and artificial intelligence (AI) software can come into play too, underwriting risks for customers.

These tools can eliminate the risk of human error because tasks can be performed faster, more cheaply and with a higher degree of consistent accuracy.

Digital follow-only syndicate Ki is one example of this type of automation in action. Its algorithm can quote insurance automatically via its digital platform, which brokers can then access from anywhere via Google Cloud.

Adam Beckett, chief distribution officer at Ageas UK, said: “Automation allows insurers and brokers to simplify insurance for customers by delegating certain tasks to proven technology and instead focus their time, attention and insight where they add real value to customers.”

Meanwhile, Daniel Lloyd-John, founder, and chief executive at Broadway Insurance Brokers added: ”If embedded insurance is the way of the Tesla EV, I think they will need broking colleagues internally. It’s even harder turning yourself into an insurer and broker.”

Claims handling chatbots

Claims departments, meanwhile, have been quick to adopt automation in a bid to increase efficiency and reduce operational costs by cutting down on the need for human intervention for simple tasks. This aims to give claims handlers more time to work on more complex claims.

Zurich, for example, partnered with insurtech Sprout.ai in December 2020 to use its AI proposition to triage property claims. This followed the introduction of the insurer’s chatbot Zara in 2018, which was designed to handle non-emergency home and motor claims in three hours.

Axa has also invested in chatbots, introducing bots Bert and Lenny in January 2019 after it saw success with chatbot Harry, which launched in June 2018. The insurer estimated that the bots should save around 18,000 man-hours a year, freeing up claims handlers to turn to more complex tasks.

Google created its first chatbot in April 2020, called Google Meena, aiming to support the insurance industry.

However, Robin Challand, claims director at Ageas UK, believes that there is still a long way to go before very complex claims can be handled solely by technology.

He said: “Machine learning can certainly present our teams with useful information to help inform decisions, but because of the various parties involved in a claim and the level of negotiation required, it is unlikely to be able to replace a person’s ability to handle such complexity.”

PASS NOTES

What myths surround automation?

In his Ted Talk in April 2021, Alastair Robertson, Zurich’s UK head of continuous improvement, automation and predictive analytics, aimed to bust four myths around automation.

These included:

- Automation jobs being more targeted at men.

- That automation will steal people’s jobs.

- Large organisations are too big and set in their ways to use automation.

- That there is a lack of team expertise around automation.

What roles in insurance could be automated?

Related Companies

- Previous

- Next

No comments yet