Aggregators are likely to take a revenue hit from FCA reforms. Here are five ways they could react and its impact on insurers and brokers.

Briefing by content director Saxon East

The figures are mind-boggling. The FCA estimates insurance firms will lose anywhere between £3.6bn and £11bn revenue over the next ten years from its pricing crackdown.

Right in the eye of the storm are the aggregators, which the regulator specifically points out to as the ones vulnerable to losing revenue as customers switch less amid renewal and new pricing being matched.

The price comparison sites have high profit margins - nearly 40% across home and motor - which they will want to maintain. If revenue goes down, so will some of their costs.

Even so, they will almost certainly look to offset the lower than expected revenues when the FCA reforms bite.

Following on from my last briefing on how the relationship between aggregators and insurance firms could change because of the FCA reforms, here are five options price comparisons could take, with potentially big impacts on insurers/brokers.

1) Demand a share of revenue from premium finance and add-ons

Currently, price comparisons do not take any share of the premium finance or add-ons. Brokers, for example, do not give away any of this income when they acquire a customer on a price comparison.

There is nothing to stop aggregators demanding a share of this income.

However, this highly-inflammatory move would further harm some of the larger brokers expecting to lose income on FCA-hit premium finance.

2) Push to maintain fees coming from brokers and insurers

Aggregators have various ways they make fees.

One method is the flat cost per sale approach.

There is also a tiered approach depending on sales volumes; type of cover; level of cover; and minimum conversion floor whereby insurance firms must convert a minimum number of clicks from the price comparison quote page to their own website.

Aggregators may adopt a nuanced tactical approach depending on the insurance firm - but the ultimate outcome will be to maintain as high as possible volume and level of fees from partners.

3) Expand more aggressively into SME

Brokers control 46% of SME premium and have around 82% retention, according to a BusinessWire analysis last year.

There is a big, largely untapped £7bn - £10bn market for price comparison sites.

Large volumes of commercial vehicle are already sold via aggregators.

Elsewhere, Direct Line for Business has had some relative success picking up tradesman.

Is it possible for aggregators to sell small shops and offices, and even more tradesman, in the same way as commercial vehicle?

So far, brokers have protected their business here. But with the extra pressure coming from the FCA reforms, price comparison sites may take a more active approach in extracting sales from this market.

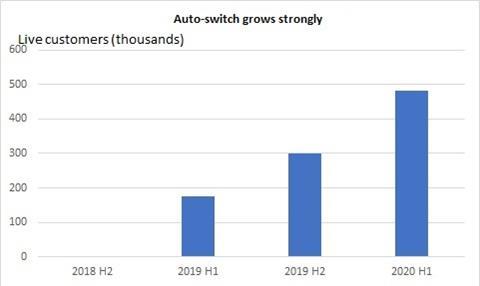

4) Rise of auto-switching

Even if new and renewal prices are aligned, there will still be cheaper deals on offer for customers who search around.

Price comparison could be more active in getting right in front of the customers faces - and one way to achieve that is via auto-switching.

GoCo’s rapid growth in auto-switch (see below) suggests there is market demand for the service. The big unknown is how much of the market can be converted.

Auto-switch (also called auto-save) could certainly be a valuable tool in increasing customer switching to offset the impacts of the FCA price reforms.

Currently, GoCo does not offer the service for general insurance. But could that change?

Even if it remains the province of energy bills, it could help offset lower revenues from general insurance.

5) Adopt the life model to charging partners

This is certainly one to look out for in the future.

If insurers start offering three-year lock-in policies (as opposed to a three-year price guarantee where the consumer could exit the policy mid-term), then aggregators could argue that they deserve a higher commission based on the duration of the policy.

In fact, this is the way the life market has worked in the past. As insurers such as Aviva know well, financial advisers were handed up front commissions in relation to the duration of the life insurance contract sold.

So is it possible for insurers, and broker partners, to offer three-year lock-in policies with price guarantees?

Insurers would face onerous capital requirements and difficult technological challenges in offering three-year lock-in contracts.

However, reinsurers, themselves facing competition from alternative income, are keen to diversify and would probably jump at the chance to help share some of the capital load.

Secondly, insurers are updating their systems with modern software providers, such as Guidewire, who have the capability to assist with these changes.

Saga, which is offering a three-year price guarantee, updated its core systems to Guidewire in 2018.

All it takes is one big player to make the leap, and the rest will follow.

No comments yet