Insurance Times explores how the regulator’s proposed measures to mitigate price walking could have an adverse effect on the use of price comparison websites

Following the FCA’s final report on pricing practices within the motor and home insurance markets, industry voices conclude that price comparison websites (PCWs) “could be the real loser” here, as the FCA’s proposed “new rules will be bad news for comparison sites”.

On 22 September 2020, the FCA published its General Insurance pricing practices market study report. The two-year project explored thousands of policies and consulted with industry stakeholders in order to get to grips with the practice of price walking – where new customers pay cheaper premiums than renewing policyholders.

In light of its findings, the FCA has proposed a series of measures to mitigate price walking. This includes insurers providing data to demonstrate they are pricing policies fairly and increasing the transparency and methods by which customers can cancel auto-renewals.

Firms will have until 25 January 2021 to offer feedback on these proposals.

Despite the positive intentions behind the FCA’s actions, the suggested measures may have a detrimental effect on PCWs and lead to less consumers switching their cover or shopping around.

James Daley, managing director of research foundation Fairer Finance, explained: “The FCA’s new rules will be bad news for comparison sites. The FCA’s own research shows that switching levels will fall and, although their modelling only shows small decreases, I think we have to be prepared for the reality to be much worse.

“We know that price is customers’ biggest concern when it comes to car and home insurance. So, once existing customers know they are being offered the same price as new customers every year, it’s likely that many people will stop switching altogether. When the renewal pack arrives, there will be even less reason to open it, as customers can rest easy knowing that their price is in line with the wider market.”

Mark Andrews, director of insurance at financial services consultancy Altus, agreed. He added: “If the new regulation delivers the behaviours intended, price comparison websites could be the real loser as customers aren’t churned so much. Arguably though, price will become even more important in the short-term as customers on inflated premiums become more aware of ‘cheaper’ products.”

Furthermore, the potential drop in switching insurance providers contrasts the FCA’s own ambitions, continued Sanjiva Perera, managing principal at Capco, a global business and technology consultancy.

“One potential negative is disruption to the business models of price comparison sites. Existing customers often use price comparison sites to obtain a cheaper ‘new customer’ quote at a different insurer. In the future, if rates for existing and new customers are on a par, then an existing customer may have less need to seek a cheaper quote through a comparison site. We may even see less switching between insurers, the opposite of what the FCA is trying to achieve.”

Other unintended consequences of the FCA’s proposals, according to Perera, include an escalation of rates as “insurers increase rates for new customers, so they are on par across both new and existing customers”.

More claims could also be declined. “Insurers [that are] forced to reduce rates may start to reject claims if, for example, important information was not declared, which will drive consumer dissatisfaction with the industry,” Perera explained.

Change in focus

Moving forward, Daley believes that price comparison websites may have to steer away from providing purely price-centric results.

He said: “With less flexibility in their pricing, it’s likely insurers will look to further hollow out their products - increasing excesses and reducing cover levels - to try and bolster their margins.

“As a result, it’s going to be more important than ever that comparison sites do a much better job of helping customers make decisions based on quality. With consumers switching and engaging with their insurers less, it will be vital that they pick suitable cover on the way in - something which often doesn’t happen today.

“Comparison sites will need to start demonstrating that they can do more for customers than simply serving them up prices.”

Andrews, on the other hand, feels that PCWs should be included in the FCA’s consideration of the dual pricing debate.

He added: “The FCAs dual pricing proposals should not just be targeted at insurers. Additional changes regarding PCWs having to clearly state the value of products before purchasing also needs to be introduced. For example, what coverage you may be missing out on by purchasing from a top three [insurer] on the PCW versus selecting number 10 at an additional premium of £50?

“We will likely see further price wars and, consequently, poorer products hitting PCWs in the next 18 to 24 months as insurers battle for new business. Customers will still tend to pick the cheapest product rather than the one most suited to their needs and this may not play out well.”

Shopping around

However, PCWs GoCompare and MoneySuperMarket agree that customers use PCWs for many reasons aside from avoiding price walking.

GoCompare chief executive and founder Lee Griffin, for example, said: “People switch insurance policies for many reasons, not just because their existing insurer has increased their price at renewal. We know that people switch when they change cars, when they receive bad service from their insurer and when their old provider can’t meet their changing needs. It’s unrealistic to say that one insurer will continue to offer the best deal for your specific needs, year after year.

“Moreover, against a harsher economic backdrop, consumers are likely to be more inclined rather than less inclined to shop around in order to save money.”

This is supported by William Clutterbuck, vice chairman of Maitland, speaking on behalf of MoneySuperMarket. He said customers typically use PCWs because their risk profile has changed, for example if they’ve bought a new car, have had to make a claim or have moved house.

He added that although the FCA’s proposals will act as a leveller for premium prices, there may still be a difference in cost – it’ll just be smaller.

“It’s a big market, [insurers] will find a way of competing and, of course, if they’re competing hard, then that very much gives us a lot of value we can deliver to people who come to our site,” he said.

Auto-renewal risks

William Clutterbuck, vice chairman of Maitland, speaking on behalf of MoneySuperMarket, admitted that the PCW is not a fan of auto-renewals. “You can have auto-renewal, but you need to select auto-renewal,” he said.

Lee Griffin, chief executive and founder of GoCompare, agreed: “A fifth of motorists currently don’t switch their policies at the point of renewal because they think it will be too much hassle. [Around] 6.7 million drivers are collectively wasting an estimated £1.9bn a year by allowing their car insurance to automatically renew without checking they are getting a good deal. The only way for people to be sure they are getting a good deal at renewal, or when they first buy insurance, is to shop around – the easiest way to do that is by using a price comparison website.”

Increased traffic

Data and analytics firm GlobalData, on the other hand, predicts that PCWs will see a short-term boom in traffic as Brits hunt for deals to mitigate the effects of this year’s coronavirus-influenced economic recession.

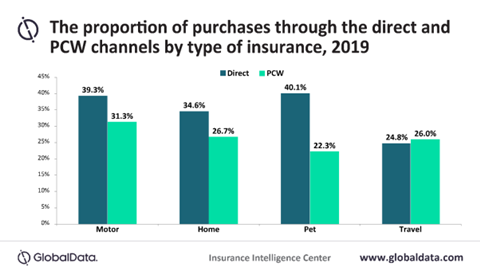

Yasha Kuruvilla, insurance analyst at GlobalData, said: “Travel insurance may be one line where the opposite occurs, with price comparison sites seeing less traffic as consumers value extensive cover to protect themselves against coronavirus-related events more than the price of a policy.

“While economists predict a return to growth in 2021 as the UK adjusts to a new normal, PCWs will likely enjoy a period of increased traffic from consumers in the near future.”

No comments yet