Brokers must understand the ramifications of the new working order to support both insurers and end clients

By Jon Guy

As insurers warn of a looming underinsurance crisis, new research has found that almost half of UK business owners did not believe they would return to in-office working full time in 2022.

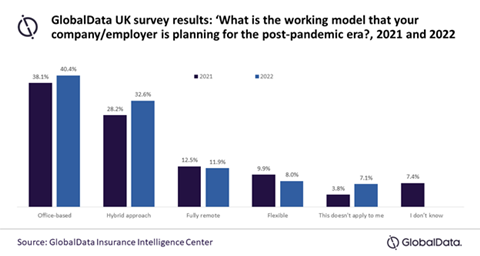

Research by data analytics and consulting company GlobalData’s Insurance Intelligence Centre, which was publicised in January 2023, found that only 40% of surveyed respondents anticipated a return to the office in 2022.

One of the Covid-19 pandemic’s most significant long-term repercussions was the transition to remote working in 2020, which saw the world of work subsequently adopt a hybrid and flexible working approach in 2021 and beyond.

GlobalData’s study warned that increasing consumer demand for flexible working models will present both challenges and opportunities for insurers moving forward.

Some industry commentators have highlighted a growing unease about the implications of hybrid working, while others - such as insurer RSA - have now adopted a hybrid system across its UK and Ireland operations.

Guillaume Anns, associate insurance analyst at GlobalData, explained: “Around a third of employers adopted a hybrid working model in 2022 - an increase from 2021.

“Staff are demanding flexibility, making working full-time in an office environment a less viable option.

“With the incoming recession likely to put further pressure on expenses, more businesses are likely to scale down and reduce their insurance cover in the process.”

Opportunities and challenges

Although insurance demand may be reduced by less office working, there are some upsides for the insurance sector.

For example, many insurers have - or are planning to - move offices to downsize, reflecting the fact that their entire staff are highly unlikely to be in the workplace at the same time on any given day.

Plus, there is also opportunity around new covers to insure a hybrid or flexible working approach.

Read: RSA implements hybrid working for over 5,000 UK staff

Read: Briefing - Is hybrid working diminishing London’s leadership as an insurance market?

Explore more news analysis here, or read up on insurers here.

What GlobalData’s research fails to address, however, is the new risks that come with a move to hybrid working.

Do firms have a responsibility to provide cover for staff when they are out of the workplace? Will the use of personal technology, such as laptops and phones, create new liabilities for businesses? Will it also create new risks around staff welfare?

The challenges businesses now face may well combine to create insurance opportunities, but these also come with a need for brokers to understand the ramifications of the new working order.

Insurers have said they are keen to educate brokers around the risks of underinsurance in order to avert a crisis. They will need to look at the changing risk dynamics for UK business alongside this.

No comments yet