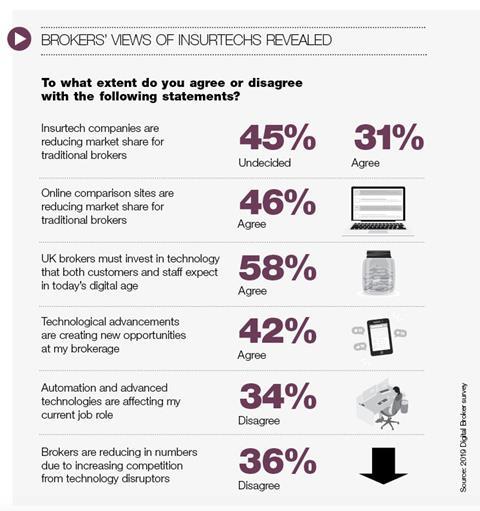

Online comparison sites are seen as a bigger threat to UK general insurance brokers than insurtech companies, according to the results of the 2019 Digital Broker survey

One-third of respondents to an Insurance Times survey said they thought insurtech companies were reducing market share for traditional brokers. A larger proportion (45%) were undecided over the potential insurtech threat to their business. This is versus 60% who cited aggregators/price comparison websites as a threat, up 11% on 2018.

Looking at the risk of disintermediation by online comparison sites, there has been a decline in broker confidence year on year. In 2018, 60% of brokers said they were ‘somewhat’ or ‘very confident’ of their ability to compete against the aggregators, but this had fallen to 38% in 2019.

Kristin Hackney, executive vice-president of customer experience at Applied Systems, said: “There were a lot of fears about insurtech initially and we think that is subsiding a little bit as brokers understand how insurtechs can help them do business better.

“With online comparison sites there’s significant adoption there from a personal lines perspective, particularly around motor,” she continued. “It’s understandable that brokers would see that as a threat to the broker channel.

“The more brokers can do to provide similar convenient services to consumers along with great customer service, that’s a great way for brokers to differentiate themselves,” she added.

Tech–broker tie-ups set to continue

The buyout of Ed and Besso by financial services tech firm BGC Group heralds a new era for wholesale broker disruption

The tie-up between BGC Partners and Ed Broking Group, completed in February, is the latest sign of disruption in the intermediary channel.

BGC has indicated it intends to buy “many more” insurance brokers, after the acquisitions of Ed and Besso, and to grow its revenue, as it has done in commercial real estate.

“I’ve got a team who spend their time at Canary Wharf understanding the models that BGC have created to disrupt other sectors,” Steve Hearn, BGC Insurance Group chief executive told Insurance Times. “This increasingly isn’t if, it’s when.

“Our sector continues to interest people outside of it, especially those immediately adjacent to it?” he said. “I would describe the BGC Group as being immediately adjacent to it and there have to be others. There are some large private equity-owned brokers out there, and by definition at some point, they’re for sale.”

The purchase of specialist broker BMS by the British Columbia Investment Management Corp (BCI) and Preservation Capital Partners (PCP) is another merger that has an emphasis on long-term innovation. PCP also owns cyber and specialty managing general agents (MGAs) Ascent and Cove.

Mergers and acquisitions (M&A) activity is going in both directions from an insurance and technology perspective. Examples of major incumbents taking stakes in insurtech startups include Willis Towers Watson’s purchase of TRANZACT, Munich Re’s acquisition of Internet of Things provider relayr and Aviva’s buyout of smart home insurance startup Neos.

As the role of technology in insurance expands, the ability to acquire new capabilities and counter the threat of new entrants is becoming more important, according to Clyde & Co.

“Technology has become a key driver of M&A,” said Ivor Edwards, partner at Clyde & Co. “On the operational side of the business, although there is a risk involved in integrating legacy systems, the potential synergies a transaction delivers can be amplified by the application of technological innovation to streamline processes, resulting in significant cost savings and financial benefits.

“Technology is also the skeleton key that unlocks multiple doors to new customers,” he added. “Companies with the deepest customer insights will become increasingly dominant and M&A immediately delivers the acquirer a vastly expanded pool of data.

He said a transaction can also be the easiest way to access innovation. “Some acquirers are looking at insurtech companies at a very early stage of development, while others prefer slightly more established targets with proven business models,” Edwards said.

Apps that aim to reunite consumers with lost property such as phones or tablets, have potential to reduce gadget and content insurance claims.

This is according to data and analytics firm GlobalData insurance analyst Yasha Kuruvilla, who said: “If people are able to easily find their lost items, the number of claims for lost devices will undoubtedly decrease.”

Apps include ReclaimHub, Missingx, Crowdfind, Troov and LOFO. These centralised global platforms allow users to post and search for lost items by geographic location. MissingX has contracts with airports and has matched more than 1.6 million items since its launch in 2001.

“Currently, only 15% of people have insurance for a one-off, high-value item such as a phone or laptop, while 28% of home insurance policies are contents only.

“But demand for contents-only insurance is expected to increase as rising house prices force more people to live in a rented home,” said Kuruvilla. “Insurers should work with companies such as Found to raise awareness about the benefits these apps can bring.”

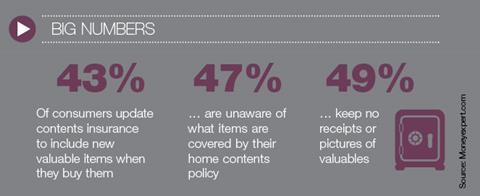

Nearly half of consumers are unaware of what items in their home are covered, research shows. Only 43% update their contents insurance to include new valuable items when they buy them, according to Moneyexpert.com.

No comments yet