Four years after the introduction of GIPP, and with slowing premium growth finally allowing its impact to be assessed, Insurance Times investigates whether the rules spawned a worrying unintended consequence – and whether an Irish model might provide the remedy

After the initial fanfare surrounding the introduction of insurance’s general pricing practice regulations (GIPP), the dust settled and, with motor premiums being driven consistently higher by claims inflation, repair costs and other macroeconomic forces, many consumers were left entirely unaware of their existence at all.

Now, with premium growth flattening, and even reversing, Insurance Times revisits the impact of GIPP, investigating its successes, failures and its possible unintended consequences.

The primary aim of GIPP – which came into effect on 1 January 2022 – was to ensure that insurers could not charge a higher price for renewing customers than they would for new customers on the same policy, thus eliminating the so called “loyalty penalty”.

As previously reported by Insurance Times, shopping and switching behaviour among motorists is at all time low and many, like Consumer Intelligence chief executive Ian Hughes, believe that is due to the delayed impact of GIPP.

Hughes has previously argued that the positive effects of the new regulations had been obscured by premium inflation, driven partly by claims inflation, which had a similar psychological impact as the loyalty penalty.

“Insurers put a load of premium through, which bumped up people’s prices and made people feel like they felt when they lost their introductory discount – they went out to market and they were switching,” he explained.

“We are only seeing the GIPP effect now, because of what happened with claims inflation and what happened with premium inflation”.

Indeed, the rate at which consumers shop around currently stands at 69.4%, with switching at 34.7% – well below the seven-year pre-GIPP averages of 83.1% and 40.9% respectively, indicating that a force other than market-driven premium decreases is affecting such trends.

So, if the rules are indeed starting to have a serious impact on consumer behaviour, can they be viewed as a success?

Unintended consequences

According to Sarah Vaughan, director at insurance consultancy Angelica Solutions, there is evidence that despite GIPP rules, returning customers are still paying more for their policies than new customers.

Read: Recent home insurance GWP growth masking issues beneath the surface – Oxbow Partners

Read: Ozempic confusion putting travel insurance at risk for thousands

Explore more Data Matters content here, or discover other news analysis stories here

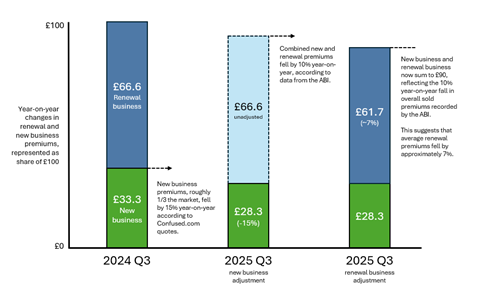

She highlighted that according to a Confused.com quoted price index – analogous to new business premiums – new business premiums fell by 15% between 2024 Q3 and 2025 Q3.

Over the same time period, the ABI reported that combined new and returning business premiums fell by just 10%. Assuming that new business accounts for approximately one third of the market, this means that renewal premiums fell by just 7% – less than half as much as new business.

Why then, are new customers paying less than returning customers, if GIPP rules were designed expressly to prevent this?

Vaughan suggested that the answer lies in one unintended consequence of GIPP – the forcing of insurers to find alternate methods of tempting new customers onto their books, while retaining their profits. Chief among these methods is creating new products with cheaper prices – discounts which come at the cost of service quality.

She explained that insurances prices “aren’t purely risk led, they’re also demand led”. Taking away the ability to price on such a key factor, tenure, can only have one possible consequence – lower profits.

“In theory that’s okay,” she continued. “Everyone had that ability taken away simultaneously and that makes it a level playing field for the underwriters. But actually, they’re not likely to just accept that lower level of profit.”

And the main route insurers have found to retaining that profit? Tempting cheaper products that contain sufficiently reduced coverage so that the insurer margins are preserved.

Vaughan added: “That’s my potential criticism of GIPP – some consumers are paying less, but are also getting less. So, are we storing up a problem of underinsurance, or a lack of understanding, which will manifest itself in problems at the claims stage?

“And if the [people] most financially vulnerable or stretched are the ones tempted by the cheaper products, they’re also going to be the ones most challenged when they realise that they’ve got a £1,000 excess, or the windscreen cover wasn’t included in their product.”

The Irish model

If consumers are being forced into inadequate cover by financial pressures, what can be done to address this risk?

“What I’m calling for is that we should do a proper analysis of the impact of GIPP that really looks at what a typical new business customer is paying compared to a renewal, and what are they getting for that,” suggested Vaughan.

“The reporting just says that an insurer has to report the average premium paid by tenure for a specific product, but that can easily hide the fact that they’ve got a suite of products that are half the price of the ones their renewing customers typically buy.”

One comparison Vaughan used was to low-traffic street initiatives in London. Those streets may see fewer vehicles, emissions and crashes, but the adjacent streets are often far, far busier and now shoulder more of collision and pollution risks.

A deeper analysis of GIPP is needed then, to ensure that like-for-like policy renewals aren’t simply the low traffic streets of the insurance world, forcing those most in need to cheaper, more exposing policies.

For a potential actionable solution, Vaughan pointed to similar anti-loyalty penalty rules introduced in Ireland around the same time that GIPP was in the UK.

She explained: “Ireland introduced a similar remedy, but there was a key difference – new business pricing is essentially unconstrained and the [anti-loyalty penalty aspect] just applies from first renewal onwards. So, the second renewal, third renewal, fourth renewal – they have to be the same as the first renewal.

“What that means is that insurers are free to try and market for new business effectively and they can still have acquisition offers. I do think that Irish model of saying, if you want a competitive market and you want to allow insurers to compete for new business, then let them.

“But if somebody’s been with you for 10 years, then they should be the paying the same price as if they’ve been with you for one year.”

He graduated in 2017 from the University of Manchester with a degree in Geology. He spent the first part of his career working in consulting and tech, spending time at Citibank as a data analyst, before working as an analytics engineer with clients in the retail, technology, manufacturing and financial services sectors.View full Profile

No comments yet