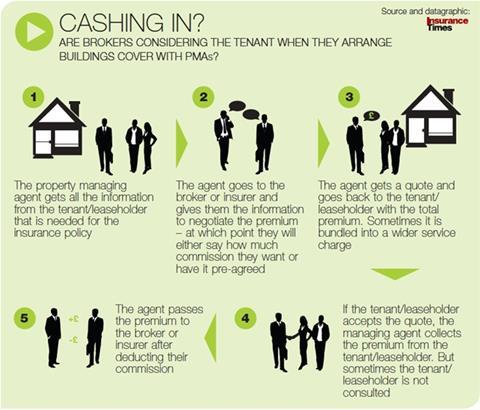

Five years on from the CMA’s report exposing huge commissions paid by brokers to property agents to win business, Insurance Times finds the practice is still very much alive and the sums being paid greater than ever

The long-running controversy on secret commissions offered by brokers to property negotiators is back in the limelight, and payments are now higher than ever.

Brokers were found to be paying landlords or managing agents commissions that distorted premiums by up to 40% to secure commercial buildings policies in a December 2014 Competitions and Markets Authority (CMA) market study.

And after comments from Sir Peter Bottomley, co-chairman of a parliamentary group looking into leasehold reform, last month signalled that the practice is still alive, one senior underwriter told Insurance Times some carriers are still today offering commission levels at 50%.

The added cost is passed onto leaseholders, often unbeknown to them, as the premium is bundled together with other costs into an annual service charge. The 2014 study found the practice encouraged property agents to take policies that were not in the best interests of leaseholders.

The CMA had subsequently recommended the FCA investigate whether the leaseholder market is being properly regulated, and enforce total transparency on the commissions property negotiators and brokers make from the policies. Almost five years on, though, and still the FCA remains quiet.

Insurance Times understood that some brokers sought to adjust their practices in the wake of that report. But since Sir Peter’s comments that “those receiving cowboy commissions by ripping off leaseholders in order to secure the landlords’ insurance business will be brought to account,” backing has flooded in for the Tory MP’s position that action must now be taken.

According to Neil Holloway, a former commercial buildings broker now specialising in recovering money on behalf of leaseholders, the commissions are as high as they’ve ever been.

Transparency

He told Insurance Times his brokerage Mulberry Insurance moved eight years ago from offering property agents commissions to a ‘trusted transparent’ policy, but then struggled to win business. In one instance he lost a client because he refused to match a £500,000 payment offered to the managing agent elsewhere.

“It became difficult to sell because 99% of people who buy this type of policy want to earn something out of it,” he said.

“There’s a secondary tier of managing agents that have built up their business on the back of insurance commissions.”

Holloway sold the business to Howden 14 months ago and set up his new specialist recovery company M2. The firm has already clawed back thousands of pounds for clients, including a banking group and a high street retail chain, that he says have fallen victim to the practice.

“There are some brokers and insurers that now don’t do real estate business because of the commission situation,” he added. “Most brokers are finding if they want to transact real estate with a landlord or managing agent, they are going to have to give a commission kick-back.”

“Horrific”

The senior underwriter who told Insurance Times of commissions reaching 50% had personal experience of seeing inflated premium prices, and said the practice was “really unfair on the person footing the bill.”

They added: “I was the underwriter for a block of flats and the actual cost of the insurance versus the amount being charged was horrific. This has not changed to date.

“The industry as a whole needs to be transparent on commission and remuneration. The sooner that a review begins into hidden commissions and fees the better.”

Holloway says the insurers should cap the commissions offered to brokers on these policies to limit the excessive amounts that the property agent can take.

The worry is the insurer that imposes caps may lose swathes of business, and this is why Holloway says regulatory action is needed – either to impose caps, enforce total transparency of the process, or both.

Insurer action

The matter is a delicate one among insurers. But Holloway said if they want to protect their brands from the accusation of ripping off leaseholders, they should take action before getting prompted by the regulator.

RSA UK chief executive Scott Egan told Insurance Times his company always considered customer outcomes, and would only work with brokers that also treat customers fairly.

“We’re not perfect, but in the end we will choose who we work with and who we partner with,” Egan said. “What I want to avoid is working with people in that distribution chain who I don’t think have a congruence with our customer values, which is to treat them fairly and recognise their demands and needs.”

Regulation

James Daley, managing director of consumer campaign group Fairer Finance said firms need guidance from trade bodies like the ABI and Biba on this matter, but that regulatory intervention would ultimately be required to stamp out the practice.

Daley said: “There are lots of potential solutions - from mandating greater transparency through to capping commissions - and these would all need to be considered through a full cost-benefit analysis. But as a first step, the CMA or FCA need to launch a piece of work to fully understand the problem.”

ABI director general Huw Evans has said he “always prefers the market to attempt to solve its own problems”, but five years on from the CMA study, it’s questionable whether the market can solve this one alone.

Egan has suggested the issue will form part of the FCA’s wider investigation into insurance distribution, but as testimony suggests the problem is getting worse the regulator may have to take a more targeted approach if there is to be any movement on this issue.

No comments yet