Rates online remain soft even as some capacity providers leave the market, but underwriters are becoming more selective

Pricing for specialist construction and engineering insurance – including contractors-all-risks (CAR) and erection-all-risks (EAR) – remains highly competitive. Plentiful capacity has meant rates remain favourable despite record losses on international accounts and the withdrawal of a growing number of Lloyd’s players in recent months as part of the market’s strategic review.

Last year’s costly natural catastrophe losses – including Hurricanes Harvey, Irma and Maria – along with several other major international claims, have eroded underwriting profitability and led to insurance price corrections on some accounts.

Examples include the collapse of a partially constructed bridge near Bogota, Colombia, in January, tunnel collapses at the Ituango Dam in Colombia in May and the failure of a hydropower dam in Laos in July.

“It is extremely challenging to steer a construction insurance portfolio in this market environment, given the long tail nature of the risk,” says Guido Benz, head of engineering and construction at Swiss Re Corporate Solutions. “It is almost like steering a boat across a lake where the boat still continues to drift after you’ve turned the power off. That’s the issue underwriters are facing with construction portfolios.”

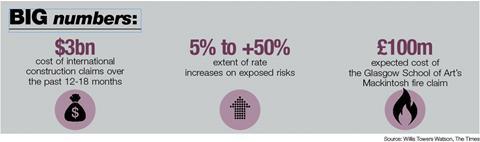

International cat-exposed accounts have seen pricing up by 5% to more than 50% in some cases, with the expectation that rates will remain relatively flat for non-catastrophe exposed books of business, according to Willis Towers Watson. It notes that there are record levels of capacity for all types of risk and that the market remains “extremely competitive”.

Costly fire losses

The UK market has, however, experienced notable claims of its own. The Mandarin Oriental Hotel fire in London and the Glasgow School of Art fire have added to the pain for construction underwriters. Both blazes occurred after costly refurbishments, with six figure losses forecast for the latter.

“There have been a large number of big project losses – particularly fires on refurb projects – and underwriters are looking much more closely at these,” says Martin Hiller, chairman of UK construction at Gallagher.

“I wouldn’t expect to see these losses driving rates up, but we will see a more cautious approach on the terms and conditions being provided,” he adds. “Contractors are likely to have imposed risk management warranties and retain more of the risk.

“There is also the need to discuss risk allocation between contractor and employer when there are high existing structure exposures in relation to the value of works.”

Faced with mounting claims and an increased focus on profitability within Lloyd’s, several syndicates have cut capacity. In October, CNA Hardy announced it would close its property treaty, marine hull and CAR/EAR portfolios, citing poor profitability even amid improving market conditions.

“Most of the underwriters in the construction insurance market are writing both a UK construction book and an international construction book,” says Hiller. “And there’s no doubt that the international losses have been significant.

“Generally, the sector has been struggling and that’s quite apparent with the number of Lloyds insurers that have now stopped writing construction business.”

“Although reinsurance cost will inevitably increase, it’s a market where there is still a lot of capacity and for the traditional good UK risks we’re not expecting a hike in premiums,” he adds. “Perhaps just a levelling off.”

Cladding concerns and PI

One exception within construction classes of business is professional indemnity, where capacity has tightened and pricing has increased substantially. The hard market has in part been driven by significant claims on waste-to-energy plants, much of it relating to unproven technology or issues with the quality of the input waste and disputes around it.

Grenfell is another significant issue. The disaster in June 2017 drew attention to the fire risk of defective cladding, prompting investigations into whether other cladding designs may need to be replaced.

“Professional indemnity is quite a distressed part of the market at the moment,” says Dave Cahill, senior partner, construction, JLT Specialty. “Non-US PI classes are the second worst-performing class of business in the whole Lloyd’s market at present. It’s a class which is in remediation and we are seeing a tremendously difficult market for the professional risk.”

“That’s because there have been a lot of claims recently for waste-to-energy projects with clients struggling to get them to perform in the way they are required to in the contract,” he says.

“That’s been followed on quite quickly by a massive amount of concern about cladding and the impact of the Grenfell disaster. It’s both the physical rectification costs of re-cladding certain properties but also the consequential loss itself that might occur.”

No comments yet