After the highs of 2017, motor rates are expected to continue falling this year and next. But there is some good news for the industry as efforts to curtail whiplash claims come into force

UK general motor insurers will continue to make a profit in 2018, but competitive and regulatory pressures are likely to mean they will once again be generating a loss in 2019.

Last year the sector reported its best result since 1994, with a net combined ratio of 96.8%. Factors driving this improved result were premium increases, fewer personal injury claims and reserve releases, buoyed by anticipated changes to the Ogden discount rate.

While the outlook remains good for 2018, the positive effect of Ogden is diminishing while competitive downward pressure on rates is returning, says EY manager Ben Wilson.

Exceptionally good year

“Last year turned out to be an exceptionally good year for insurers for several reasons, including Ogden, the reinsurance rates being reduced by the end of the year and some really positive trends on bodily injury in whiplash.”

“This year is also going to be quite good,” he said. “Premium is starting to reduce, but you still have some of the increases from last year that flow through the accounts, with premium increases taking a year to earn through.

“In 2019 all the premium rate cuts that we’ve seen this year will really hit the results, because they’ve been quite stark really,” he says. “And that’s more than the trends that you’re on the claims inflation side, so in 2019 you’re going to be back above 100% in the combined operating ratio.”

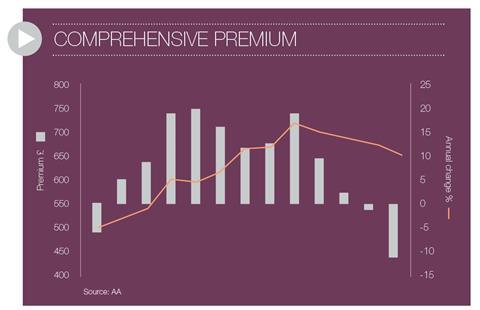

Motor insurance rates fell by 10.8% in the second quarter of 2018, according to the AA British Insurance Premium Index, with the average premium £79 cheaper than the same period last year.

Janet Connor, AA insurance director, attributed the fall in premium to claims culture reforms such as the Civil Liability Bill, adding that the “outlook for drivers is positive, especially if the promised new legislation is effective in stemming the tide of spurious whiplash injury claims.”

But even with the whiplash reforms and expected impact on cutting claims costs, it is anticipated that motor insurers will be running their businesses at a loss in 2019. The influx of capacity from reinsurers and MGAs is putting pressure on pricing.

“It’s good to see average premiums in the motor market reducing after the peaks we saw last year,” says Chris Jarratt, Coversure head of product development.

“The market got to the point where it was becoming publicly criticised for charging unaffordable rates, and it was clear that improvement was needed.

“In the broker market, careful and targeted underwriting is helping to sustain profitable growth, although competition against the direct market is still present.”

Civil Liability Bill continues progress

A proposal that would have given the FCA the power to force insurers to pass on up to £1.3bn in claims savings to policyholders was not adopted during the second reading of the Civil Liability Bill in the House of Lords. But carriers are expected to pass on any savings from lower claims costs and the higher discount rate.

Chris Jarratt, head of product development at Coversure, says this is a good thing.

“If the Civil Liability Bill is passed it will help to manage insurers’ claims costs. I would hope to see some consideration from insurers regarding pricing for motor insurance.”

Over the past decade personal injury claims have risen by 40%, despite vehicles becoming safer and a fall in the number of road traffic accidents, according to the ABI. It blames the claims inflation on spurious whiplash claims and how a “broken personal injury compensation system is being exploited by claimant lawyers”.

It notes the industry has a track record for passing on claims savings to consumers, having passed on £1.1bn in savings after the introduction of the Laspo [Legal Aid, Sentencing and Punishment of Offenders] Act in 2012.

“Soft tissue injury claims have been rising year-on-year since 2014 as cold calling claims firms have thrived, driving up the cost of insurance,” says ABI director general Huw Evans. “This Bill will ensure people in England and Wales receive fair compensation while reducing excess costs.

He added: “In a competitive market such cost benefits get passed through to customers, as they did after previous reforms in 2012 when average motor premiums fell by £50 over the next two years.”

No comments yet