Such deals have fallen significantly as competition from private equity has taken hold of the market

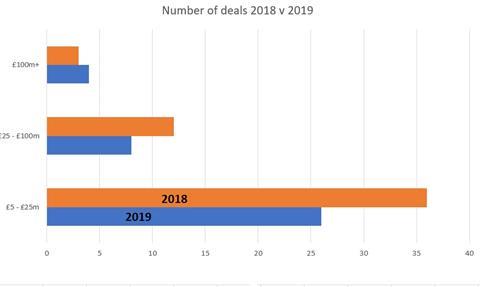

The number of ’sweet spot’ deals for buying brokers valued at between £5m and £25m decreased significantly last year, according to data pulled together from one of the UK’s leading M&A experts (see below).

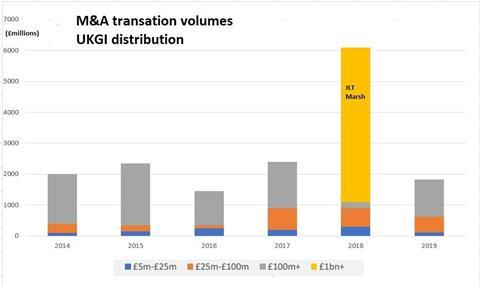

IMAS’s 2019 review of UK distribution deals in 2019 shows that the sweet spots for deals - generally between £5m and £25m - are down amid fierce competition fuelled by private equity.

The fierce competition is also inching up prices, with average deal pricing now x9 trading earnings (EBITDA).

IMAS founder Olly Laughton-Scott says there are fewer deals happening in the sweet spot because there are fewer brokers around, with so many having already been snapped up.

Laughton-Scott said private equity had different models that would find deals, despite the scarcity in the sweet spot.

”PE is very opportunity driven. They do not have religion. They will look at investment thesis,” he said.

”Essentially, different models have evolved to take advantage.

”If you look at Ethos, what they have done is to make a model to buy small acquisitions which are cheaper. I don’t think you can say PE is after one thing.

“If a part of the market is not being serviced, you create a vehicle to do that. PE is good at sensing the opportunity and putting money to play.”

Impact of covid

Laughton-Scott said Covid would definitely have an impact on deal making, certainly in the short to medium term.

”Deals need stability and if you look at the stock market what a business will be worth in a year’s time is pretty uncertain,” he said.

”Many firms, whilst they are doing okay, there are lots operational issues they have to sort out. They are focused on operational issues rather than deals.”

He also said Covid would have an impact on debt, and therefore deal making.

”A lot of the deals have been driven with significant amount of banking debt, especially the bigger ones, and the debt will get more expensive.

”A lot of debt providers have got major operational issues, they have existing clients who are suffering. They will see that the risk profile has increased, debt is more expensive and that will impact on pricing.”

No comments yet