Broking M&A is focusing on the extremities of the UKGI marketplace, with smaller firms being eyed up and the ‘consolidation of the consolidators’ potentially on the cards too, says co-founder

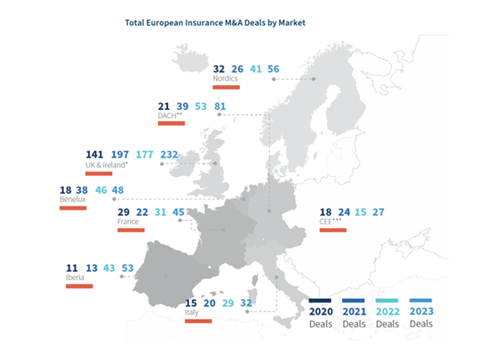

The UK and Ireland continue to be the leading force in the European insurance M&A market, with the 2023 FTI Consulting European Insurance M&A Barometer Report, published in March 2024, revealing a 31% increase in the number of deals completed in this jurisdiction.

The report found that there were around 232 deals announced in the UK and Irish markets over the course of 2023, up from 177 a year earlier. This accounts for more than 40% of the deals announced across the whole of Europe.

The study did, however, predict that M&A activity will have reached a peak during 2023, largely due to the “scarcity of targets” – particularly in the broking market, which continues to fuel deal volumes.

Such predictions have been made a number of times in recent years, yet none of them have come to fruition yet.

Indeed, Insurance DataLab co-founder Dan King thinks broking M&A is set to continue at a pace – even if the pool of potential targets may not be quite as large as it used to be.

He said: “The increased regulatory burden is making life tougher for broker leaders and with many approaching retirement age, quite a few are likely to be looking to exit.

“With the imminent prospect of a new government likely to increase the level of taxation, deal volumes may even rise before they start to come down again.”

Booming broker businesses

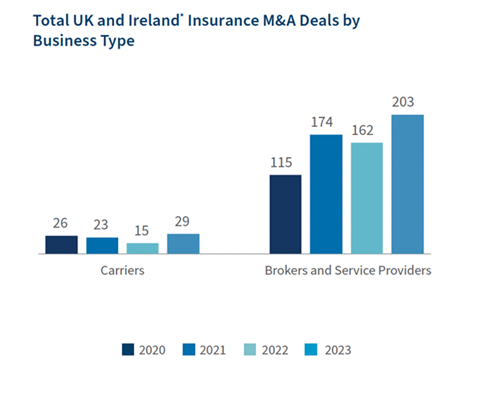

Insurance DataLab’s own analysis of the UKGI broking M&A market for 2023 echoed FTI Consulting’s findings that deal volumes continued to grow last year, with more than 130 deals completing across the course of 2023.

Brown and Brown was one of the most active firms – it completed more than 15 deals in 2023 following its acquisition of Global Risk Partners (GRP) in 2022.

Notable deals included the purchase of Vetsmedicover in August 2023, which marked the broker’s entrance into the pet insurance market, as well as London-based Kentro in October 2023 – an insurance group that manages more than £500m of gross written premium (GWP) across offices in the UK, US, Europe, Asia and Dubai.

Clear Group was another active acquirer last year as its deal flow hit double digits during 2023. Deals included the acquisition of Heath Crawford and Foster in September 2023, which added £18m of GWP to the group.

Last year also marked Clear Group’s first foray into the MGA market as it took a 50% stake in Thomond Underwriting in July 2023. The broker followed this up with a further two MGA deals before the end of the year as it continued to expand its underwriting footprint.

The big broking news of the year, however, was the announcement of the merger of Markerstudy and Ardonagh-owned Atlanta in a £1.2bn deal.

The two businesses are estimated to control more than £3bn of GWP, with the deal getting the greenlight by the Competition and Markets Authority (CMA) in March 2024.

The regulator initially launched an inquiry in January 2024 to look at whether the transaction would result in a “substantial lessening of competition within any market or markets in the UK for goods or services”. After a review, it agreed to approve the merger, however.

Read: Howden expands sport and entertainment arm with broker buy

Read: Seventeen Group announces double acquisition

Explore more M&A-related stories here, or discover more news content here

Despite this personal lines megadeal, smaller acquisitions have generally made up the bulk of M&A deals completed over the course of 2023.

King said this is a trend the industry can expect to see continuing throughout 2024.

“A lot of the mid-market brokers have already been acquired and we are now seeing a focus on the smaller end of the market,” he explained. “The consolidators are really focusing on bringing specialist businesses into their operations.

“If they can’t complete a deal that brings in a significant and sizeable level of GWP, [consolidators] are looking to secure expertise and specialist knowledge that can accelerate growth in a particular niche sector.”

Transaction trends

If these types of smaller acquisitions are to continue to dominate the UKGI market in 2024, then King noted that the industry could also expect to see a new form of M&A – something that has been touted as being on the horizon for a number of years now.

“The consolidation of the consolidators has been on the lips of industry commentators for a while now and 2024 could certainly be the year that this happens,” he said. “We’ve already seen an influx of overseas capital – such as with the Brown and Brown deal for GRP.

“I would not be surprised if one of these players finally makes the move to acquire one of their peers from the consolidator market.”

One of the biggest changes of the year, however, is a significant uptick in M&A activity in the insurer and carrier markets.

RSA’s acquisition of NIG in a £520m deal with Direct Line Group (DLG), which could rise to £550m depending on performance, was one of the biggest of the year. The deal was confirmed in September 2023.

At the time of the announcement, RSA said the transaction would see it become the UK’s third largest commercial lines insurer, with an estimated 7% of total market share – previously it was ranked as the sixth largest commercial lines insurer.

Speaking to Insurance Times just after the deal was announced, RSA chief executive Ken Norgrove described the acquisition as “a unique and transformational deal” for the insurer.

“[This acquisition] really turbo boosts our existing strategy for our broker proposition and our customer proposition in commercial,” he said.

“What we’re acquiring is DLG’s commercial lines brokerage business, 98% of which is the NIG brand and Farmweb brand – this is significantly transformational for us and complimentary to our own business.

“We’ve been very strong in the mid-market and specialty areas, but what this really does is bring us into play in the sub-10,000 space and cements our proposition in the SME [arena].”

RSA was also active in one of the other big deals of 2023, but this time on the other side of the equation, selling its home and pet insurance business to Admiral as it completed its exit from the UK personal lines market. This was confirmed in December 2023.

Since then, other deals have also been mooted, most notably Ageas’ pursuit of DLG – although this move has since been abandoned after DLG turned down an offer in excess of £3bn in March 2024.

Read: ‘Integration and transformation’ the drivers for RSA this year – Ken Norgrove

Read: Jason Storah – Aviva’s Probitas buy marks ‘win-win’ to accelerate ‘organic ambitions’

Explore more insurer-related content here, or discover more interviews here

King thinks it is likely that further deals involving insurers will materialise over the coming months.

“The UKGI market is a very crowded and competitive space for underwriters and one that we think is ripe for consolidation,” he commented.

“A number of insurers have revealed ambitions for selling their business or disposing of certain units, so it would not surprise me if 2024 was the year that some of these deals started to materialise.

“Market conditions have been incredibly tough of late and some of the big players could certainly look to take advantage by acquiring businesses that they think can be turned around as the market begins to pick up again.”

No comments yet